Yahoo Finance

Yahoo Finance Three Reasons to Retain BD (BDX) Stock in Your Portfolio Now

Becton, Dickinson and Company BDX, popularly known as BD, is well-poised for growth in the coming quarters, courtesy of its solid product portfolio. The optimism led by a solid second-quarter fiscal 2024 performance and a few strategic deals are expected to contribute further. However, macroeconomic concerns and stiff competition persist.

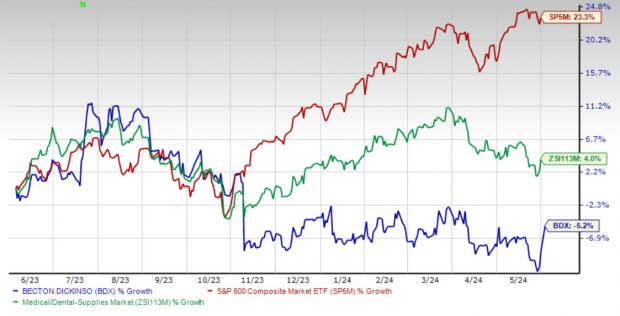

Over the past year, this Zacks Rank #3 (Hold) stock has lost 5.2% against the 4% rise of the industry and 23.3% growth of the S&P 500.

The renowned medical technology company has a market capitalization of $67.04 billion. It projects 8.8% growth for the next five years and expects to maintain its strong performance. BD’s earnings surpassed estimates in three of the trailing four quarters and broke even once, with the average surprise being 5.4%.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strong Q2 Results: BD’s solid second-quarter fiscal 2024 results buoy our optimism. The company registered solid top-line results, along with improvements in organic revenues and bottom-line performances. Robust performances by all segments and both geographic regions were also recorded. Strength in most of BD’s segment’s business units during the reported quarter was also seen.

Strategic Deals: BD has inked a few strategic agreements for its products over the past few months, raising our optimism. In February, it announced a strategic partnership with Camtech Health to advance cervical cancer screening by offering the first-ever option for women in Singapore to self-collect a sample privately in their homes.

In January, BD announced a strategic collaboration agreement with Techcyte to offer an artificial intelligence-based algorithm that guides cytologists and pathologists to efficiently and effectively identify evidence of cervical cancer and pre-cancer using whole-slide imaging.

Product Portfolio: We are upbeat about BD’s slew of product launches in recent times. Last month, the company received the FDA’s approval for the use of self-collected vaginal specimens for human papillomavirus testing when cervical specimens cannot otherwise be obtained.

In April, BD announced the global commercial release of the three- and four-laser additions to the BD FACSDiscover S8 Cell Sorter family, which complement the five-laser instrument launched last year.

Downsides

Macroeconomic Concerns: Global economic challenges, including rising inflation and volatile capital markets, among others, pose risks to the demand and pricing of BD’s products and services. These conditions can disrupt its supply chain, impact production, and increase its borrowing costs, affecting its business.

Stiff Competition: BD operates in an increasingly complex and challenging medical technology marketplace. Although technological advances and scientific discoveries have accelerated the pace of change in medical technology, the regulatory environment of medical products is becoming more complex and vigorous. Acquisitions and collaborations by and among companies seeking a competitive advantage also affect the competitive environment.

Estimate Trend

BD is witnessing a positive estimate revision trend for fiscal 2024. In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 0.8% north to $13.04.

The Zacks Consensus Estimate for the company’s third-quarter fiscal 2024 revenues is pegged at $5.07 billion, suggesting a 3.9% improvement from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, Boston Scientific Corporation BSX and Ecolab Inc. ECL.

DaVita, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 13.6%. DVA’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 29.4%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

DaVita’s shares have gained 48.4% compared with the industry’s 21.3% rise in the past year.

Boston Scientific, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 12.5%. BSX’s earnings surpassed estimates in each of the trailing four quarters, with the average being 7.5%.

Boston Scientific has gained 46.9% compared with the industry’s 1.9% rise in the past year.

Ecolab, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 14.3%. ECL’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 1.3%.

Ecolab’s shares have rallied 33.3% against the industry’s 9.7% decline in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

Ecolab Inc. (ECL) : Free Stock Analysis Report

Becton, Dickinson and Company (BDX) : Free Stock Analysis Report

DaVita Inc. (DVA) : Free Stock Analysis Report