Yahoo Finance

Yahoo Finance Will Rate Hikes Impact Allstate's (ALL) New Business in Q1?

The Allstate Corporation ALL is scheduled to release first-quarter 2024 results on May 1, after the closing bell.

Factors to Note

The company’s focus on keeping up with elevated loss cost trends is commendable, given it has been pursuing rate hikes consistently to earn profits in its Auto and Homeowners business. We expect the first-quarter’s performance to benefit from improvement in underwriting margins in Auto and Homeowners. Moreover, moderating the personal auto loss environment is likely to have provided some respite to Allstate.

The auto insurance business is expected to have been aided by expanding earned premiums and reduced adverse non-catastrophe prior-year reserve re-estimates in the first quarter. Meanwhile, the homeowners’ insurance business is likely to have received a boost from improved average gross premium per policy in the Allstate and National General brands. Customer 360 product is expected to have generated higher volumes for National General in the first quarter. However, the continued incidence of catastrophe losses is expected to have acted as a partial offset for the business’ quarterly performance. We expect the Property & Liability combined ratio to improve 1,150 bps year over year in the first quarter.

However, rate hikes might have impacted new business growth in the first quarter. This would result in a decline in policies in force, given the company’s reduced advertising spend. Given moderating but still elevated loss cost trends, the company might have found it challenging to increase advertising expenses in the first quarter. Lower retention coupled with decreased policy in force might limit the Property and Liability segment’s growth.

However, persistent rate increases in the coming quarters are expected to help ALL spend more on advertising, thereby increasing policies in force by 2024-end. Improved profitability coupled with rising policies in force should drive shareholder value. ALL’s aim to expand market share in Property and Liability also bodes well.

Net investment income is anticipated to have received an impetus from higher fixed income yields and increased duration of bonds. We expect the metric to have increased 2.7% in the first quarter.

The Protection Services segment is expected to have been aided by the strength of Allstate Protection Plans and Allstate Dealer Services coupled with expanding international operations. We expect the unit’s revenues to rise 20% year over year to $804 million in the first quarter. However, the upside is likely to have been partly offset by a higher share of lower-margin business and higher severity of claims.

Additionally, improved premiums and contract charges, as well as higher revenues derived from group health products, are likely to have contributed to the performance of the Allstate Health and Benefits segment in the to-be-reported quarter. However, the upside is likely to have been partly offset by a decline in individual health and employer voluntary benefits and, escalating expenses linked with system investments. Our estimate for the unit’s revenues is $594.7 million, up 1.7% year over year.

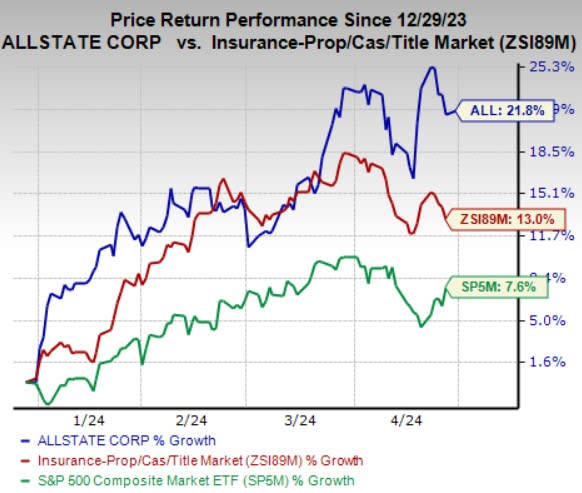

YTD Price Performance

Shares of ALL gained 21.8% in the year-to-date period compared with the 13% growth of the industry and a 7.6% increase in the S&P 500 Index.

Image Source: Zacks Investment Research

Q1 Earnings Preview

The Zacks Consensus Estimate for first-quarter earnings per share of $3.88 suggests an approximately four-fold increase from the prior-year loss of $1.30. The consensus mark jumped 10 cents over the past 30 days. ALL beat the consensus estimate for earnings in three of the trailing four quarters and missed once, with the average surprise being negative 43.9%. The consensus estimate for first-quarter revenues of $15.3 billion indicates an 11% increase from the year-ago reported figure.

Our proven model does not conclusively predict an earnings beat for Allstate this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. However, that’s not the case here, as you see below.

Earnings ESP: Allstate has an Earnings ESP of 0.00%. The Most Accurate Estimate is pegged at $3.88, in line with the Zacks Consensus Estimate. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

Zacks Rank: ALL currently carries a Zacks Rank of 2.

Stocks to Consider

Here are some other companies from the Property and Casualty insurance space, which according to our model, have the right combination of elements to beat on earnings this time around:

Arch Capital Group Ltd. ACGL currently has an Earnings ESP of +0.16% and a Zacks Rank of 3, at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for ACGL’s first-quarter 2024 earnings is pegged at $2.06 per share, indicating an improvement of 19.1% from the prior-year quarter’s reported number.

Arch Capital’s earnings beat estimates in each of the trailing four quarters, the average surprise being 27.3%.

AXIS Capital Holdings Limited AXS has an Earnings ESP of +1.56% and a Zacks Rank of 3, at present. The Zacks Consensus Estimate for AXS’s first-quarter 2024 earnings is pegged at $2.68 per share, suggesting 15% growth from the year-ago quarter’s reported figure.

AXIS Capital’s earnings beat estimates in each of the trailing four quarters, the average surprise being 102.6%.

RenaissanceRe Holdings Ltd. RNR has an Earnings ESP of +0.41% and a Zacks Rank of 3, at present. The Zacks Consensus Estimate for RNR’s first-quarter 2024 earnings is pegged at $9.86 per share, which implies a 20.8% rise from the year-ago quarter’s reported figure.

RNR’s earnings beat estimates in each of the trailing four quarters, the average surprise being 24.8%.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

RenaissanceRe Holdings Ltd. (RNR) : Free Stock Analysis Report

The Allstate Corporation (ALL) : Free Stock Analysis Report

Axis Capital Holdings Limited (AXS) : Free Stock Analysis Report

Arch Capital Group Ltd. (ACGL) : Free Stock Analysis Report