Yahoo Finance

Yahoo Finance PBOC’s Bond-Trading Drumbeat Leaves Market Debating the How

(Bloomberg) -- Growing speculation the People’s Bank of China will add to its policy toolbox by buying and selling government bonds has market watchers debating how that’s likely to work in practice.

Most Read from Bloomberg

Real Estate Investors Are Wiped Out in Bets Fueled by Wall Street Loans

Billionaire-Friendly Modi Humbled by Indians Who Make $4 a Day

Much will depend on the PBOC’s reasons to buy or sell bonds: it may wish to use the tool to attempt to cool an overheated rally, or it may have a longer-term plan for better liquidity management in the financial system, according to strategists. Complicating matters for some China watchers is the central bank’s aging stockpile of bonds to sell, which potentially limits the parts of the yield curve it can target.

Ever since an old speech by President Xi Jinping mentioning PBOC bond trading as a potential tool came to the market’s attention two months ago, the central bank has made clear it doesn’t mean large bond purchases a la quantitative easing. If anything it suggested a sale of bonds was more likely, to prevent excessively low yields which it sees as endangering financial stability and weighing on the yuan.

A rally in Chinese bonds has pushed benchmark yields toward their lowest in more than two decades amid a wave of inflows into scarce fixed-income securities and pessimism over the country’s long-term growth potential. That has led to a series of warnings from the PBOC on the risks of a bond bubble, particularly in longer-dated debt.

“There is a good chance they sell first before the PBOC buys bonds, as controlling the interest rate on long-term bonds is a good excuse to kick off the program,” said Le Xia, chief Asia economist at BBVA. It “would be a phased action, starting with a small amount to launch the tool, then gradually increasing in size.”

Not Enough Bonds

To others though, a practical issue is that there may not be enough bonds for the PBOC to sell, or at least those with the maturities it wants to guide.

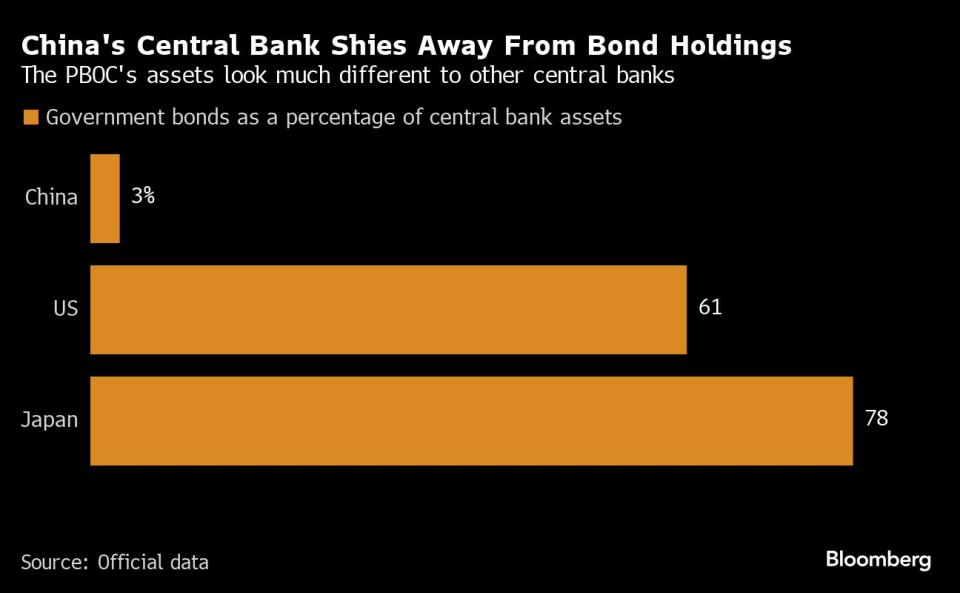

Unlike peers such as the Federal Reserve or Reserve Bank of Australia which accumulated sizable amounts of debt before subsequently reducing their balance sheets, the PBOC has only bought a few batches of special sovereign bonds more than a decade ago. Instead, it has tended to use banks as proxies to manage liquidity and adjust financial conditions, which can have shortcomings.

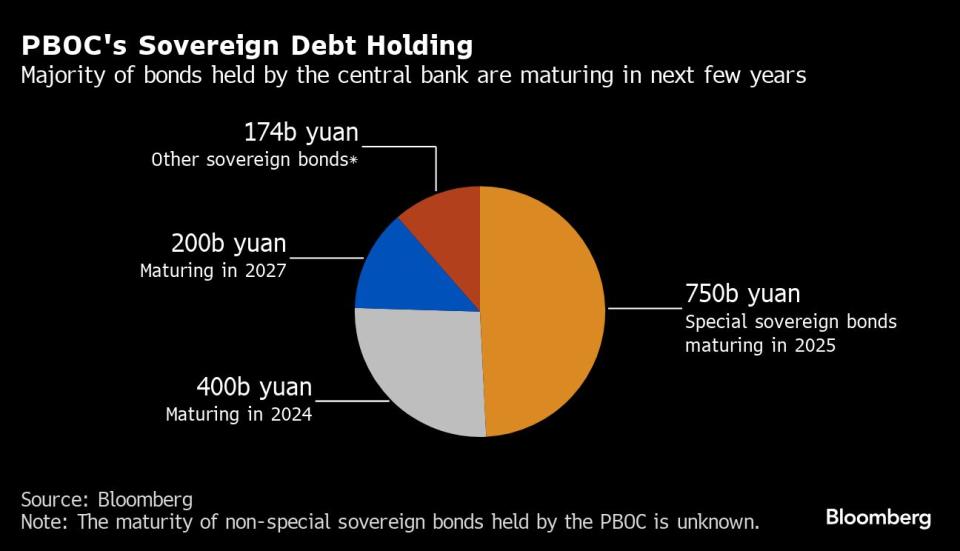

“A direct selling of long-term Chinese government bonds from the central bank appears to be less credible, given the remaining tenors of bonds held by the PBOC are mostly less than four years,” a team at Goldman Sachs Group Inc including Xinquan Chen wrote in a note Wednesday.

The central bank held about 1.5 trillion yuan ($207 billion) of government debt on its balance sheet as of April.

“Initially, the PBOC will have to find a way to acquire bonds, so that it can buy and sell in the market,” said Adam Wolfe, emerging markets economist at Absolute Strategy Research. That would likely involve buying bonds from market makers in the interbank market when aggregate liquidity is tight, so it can then sell them when conditions loosen, he said.

In a recent PBOC response to media including Bloomberg it said it may sell some low-risk bonds including government debt when needed, but provided no specific information on the source of those securities. The central bank didn’t immediately reply to a fax seeking comments for this story.

Of the bonds the PBOC currently holds, 400 billion yuan of notes maturing in August could potentially be “rolled into longer maturities and offer the central bank some ‘ammunition’ when it needs to sell,” said Janice Xue, strategist at Bank of America.

Some have speculated that the PBOC would look to initiate a bond-lending arrangement, like borrowing securities from primary dealers or big banks, though there is little precedent for such a move in the global central bank playbook.

Additional Tool

For many, the trading of sovereign bonds may be best viewed as an additional tool for the PBOC to manage liquidity in the market.

“In that case net purchases would be the new normal and net selling would be seasonal or tactical,” said Ding Shuang, chief economist of Greater China and North Asia at Standard Chartered Bank. “We expect PBOC holding of CGBs to rise over time.”

But should the PBOC’s goal be to cool the rally, a paradox is that it may not actually need to act, as a warning may be enough, according to ING and Credit Agricole.

“I don’t expect the PBOC to start bond selling in the near term, if verbal intervention is successful in slowing the fall in yields,” said Lynn Song, ING’s greater China chief economist. Urgency will abate should yields stay in a range deemed as matching fundamentals or pressure on the yuan eases as more global central banks shift to cutting rates.

“China’s long-end rates haven’t made new lows after the warning from the PBOC, though demand for bonds could still be quite strong,” said Xiaojia Zhi, an economist at Credit Agricole CIB in Hong Kong, who expects the central bank to take a gradual approach to avoid excessive volatility.

From a timing point of view, the central bank might also wait for guidance from top officials before taking action, according to BBVA’s Le Xia.

“The more appropriate window may be after the Third Plenary session,” a top-level meeting by the Communist Party’s Central Committee scheduled in July, he said.

--With assistance from Iris Ouyang.

Most Read from Bloomberg Businessweek

Sam Altman Was Bending the World to His Will Long Before OpenAI

David Sacks Tried the 2024 Alternatives. Now He’s All-In on Trump

Legacy Airlines Are Thriving With Ultracheap Fares, Crushing Budget Carriers

©2024 Bloomberg L.P.