Yahoo Finance

Yahoo Finance Here's Why We're Wary Of Buying freenet's (ETR:FNTN) For Its Upcoming Dividend

freenet AG (ETR:FNTN) is about to trade ex-dividend in the next three days. Typically, the ex-dividend date is one business day before the record date which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. In other words, investors can purchase freenet's shares before the 9th of May in order to be eligible for the dividend, which will be paid on the 14th of May.

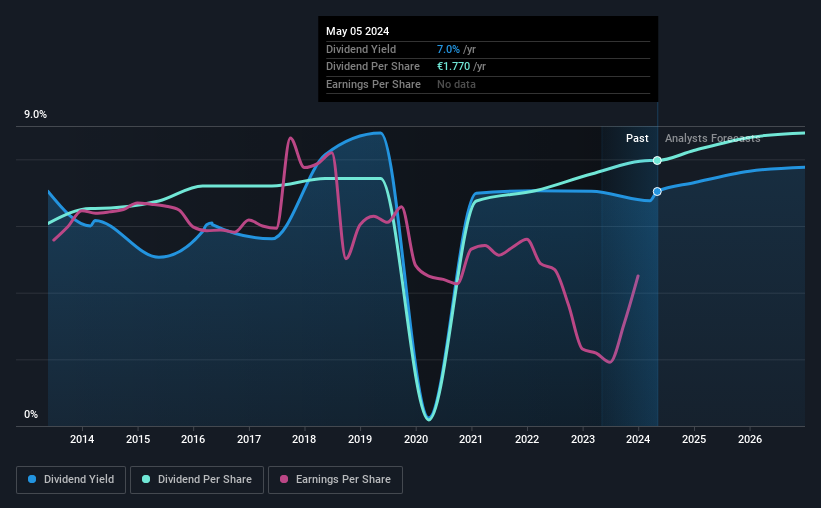

The company's upcoming dividend is €1.77 a share, following on from the last 12 months, when the company distributed a total of €1.77 per share to shareholders. Based on the last year's worth of payments, freenet stock has a trailing yield of around 7.0% on the current share price of €25.16. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to investigate whether freenet can afford its dividend, and if the dividend could grow.

View our latest analysis for freenet

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. freenet paid out 136% of profit in the past year, which we think is typically not sustainable unless there are mitigating characteristics such as unusually strong cash flow or a large cash balance. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Over the last year it paid out 58% of its free cash flow as dividends, within the usual range for most companies.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and freenet fortunately did generate enough cash to fund its dividend. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. freenet's earnings per share have fallen at approximately 5.7% a year over the previous five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the last 10 years, freenet has lifted its dividend by approximately 2.7% a year on average. That's intriguing, but the combination of growing dividends despite declining earnings can typically only be achieved by paying out a larger percentage of profits. freenet is already paying out a high percentage of its income, so without earnings growth, we're doubtful of whether this dividend will grow much in the future.

To Sum It Up

Has freenet got what it takes to maintain its dividend payments? It's never fun to see a company's earnings per share in retreat. Worse, freenet's paying out a majority of its earnings and more than half its free cash flow. Positive cash flows are good news but it's not a good combination. Bottom line: freenet has some unfortunate characteristics that we think could lead to sub-optimal outcomes for dividend investors.

Although, if you're still interested in freenet and want to know more, you'll find it very useful to know what risks this stock faces. For example, we've found 1 warning sign for freenet that we recommend you consider before investing in the business.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.