Yahoo Finance

Yahoo Finance Zuora's (NYSE:ZUO) Stock Price Has Reduced 52% In The Past Three Years

The truth is that if you invest for long enough, you're going to end up with some losing stocks. But long term Zuora, Inc. (NYSE:ZUO) shareholders have had a particularly rough ride in the last three year. Sadly for them, the share price is down 52% in that time. The good news is that the stock is up 6.4% in the last week.

View our latest analysis for Zuora

Zuora isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Shareholders of unprofitable companies usually expect strong revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

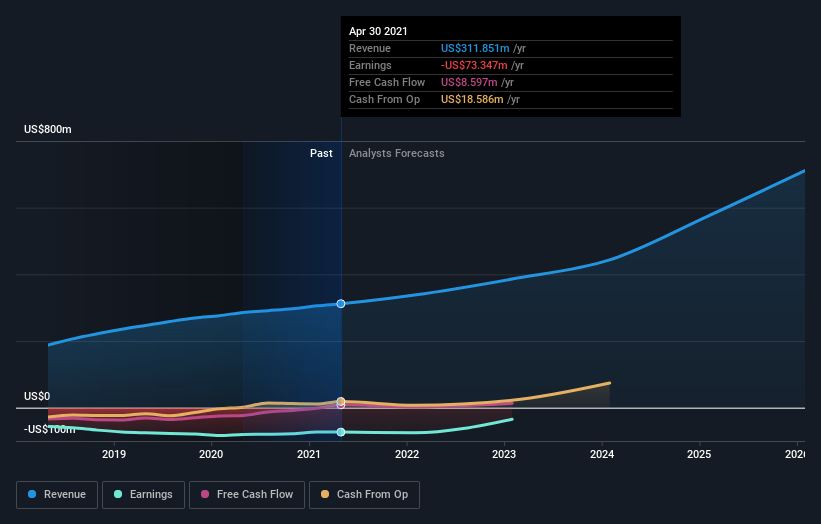

In the last three years, Zuora saw its revenue grow by 15% per year, compound. That's a pretty good rate of top-line growth. That contrasts with the weak share price, which has fallen 15% compounded, over three years. To be frank we're surprised to see revenue growth and share price growth diverge so strongly. It would be well worth taking a closer look at the company, to determine growth trends (and balance sheet strength).

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We're pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. It's always worth keeping an eye on CEO pay, but a more important question is whether the company will grow earnings throughout the years. This free report showing analyst forecasts should help you form a view on Zuora

A Different Perspective

Zuora shareholders are up 22% for the year. While you don't go broke making a profit, this return was actually lower than the average market return of about 45%. On the bright side, that's certainly better than the yearly loss of about 15% endured over the last three years, implying that the company is doing better recently. We hope the turnaround in fortunes continues. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for Zuora you should know about.

But note: Zuora may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.