Yahoo Finance

Yahoo Finance Is Zosano Pharma (NASDAQ:ZSAN) Using Debt In A Risky Way?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Zosano Pharma Corporation (NASDAQ:ZSAN) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Zosano Pharma

What Is Zosano Pharma's Debt?

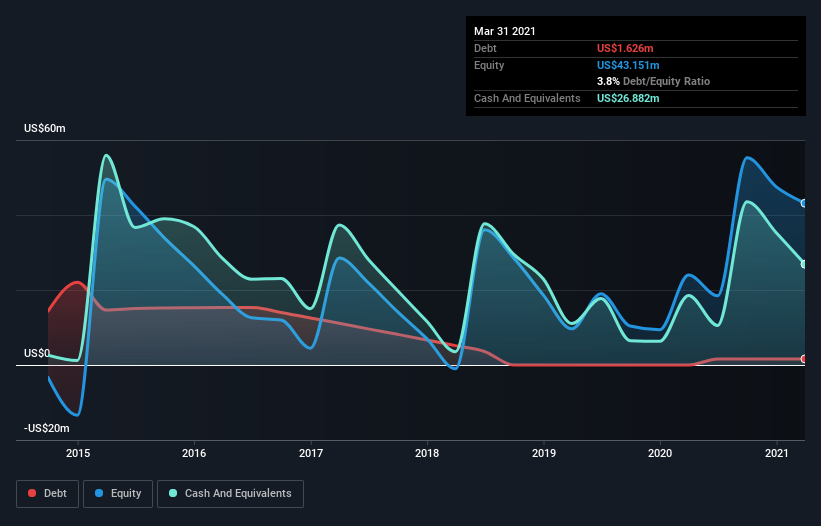

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Zosano Pharma had US$1.63m of debt, an increase on none, over one year. However, it does have US$26.9m in cash offsetting this, leading to net cash of US$25.3m.

How Strong Is Zosano Pharma's Balance Sheet?

We can see from the most recent balance sheet that Zosano Pharma had liabilities of US$14.4m falling due within a year, and liabilities of US$8.15m due beyond that. On the other hand, it had cash of US$26.9m and US$243.0k worth of receivables due within a year. So it can boast US$4.57m more liquid assets than total liabilities.

This surplus suggests that Zosano Pharma has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Zosano Pharma has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Zosano Pharma's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Since Zosano Pharma doesn't have significant operating revenue, shareholders must hope it'll ramp sales of its new medical tech as soon as possible.

So How Risky Is Zosano Pharma?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months Zosano Pharma lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$41m of cash and made a loss of US$33m. Given it only has net cash of US$25.3m, the company may need to raise more capital if it doesn't reach break-even soon. The good news for shareholders is that Zosano Pharma has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 5 warning signs for Zosano Pharma you should be aware of, and 3 of them make us uncomfortable.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.