Yahoo Finance

Yahoo Finance XPEL: A 100-Bagger's Journey to Further Upside

XPEL Inc. (NASDAQ:XPEL) is familiar company among many microcap investors. It has become a 100-bagger, with its share price skyrocketing from 85 cents in 2016 to a peak of nearly $104 per share in July 2021. With the current trading price around $54 per share, its shareholders have achieved a staggering compounded annual return of 68% over the past seven years.

Let's delve deeper to see whether XPEL presents a good opportunity for long-term investors currently.

Strong business growth and cash flow generation

XPEL is one of the leading suppliers of automotive paint protection film, window film and ceramic coatings. The company distributes its products through various channels, including its own installation centers, independent installers, new car dealerships and online. It has two main revenue streams are product and service. In 2023, its product revenue reached $311.4 million, accounting for 78.60% of the total. The service revenue, comprising its Design Access Platform software, installation labor, cutback credits and training, was nearly $85 million, representing 21.40% of total sales.

Of the two, service revenue experienced much higher growth rates of 56.80% and 29% in 2022 and 2023. In contrast, product revenue grew by approximately 18.80% and 20.60% over the past two years.

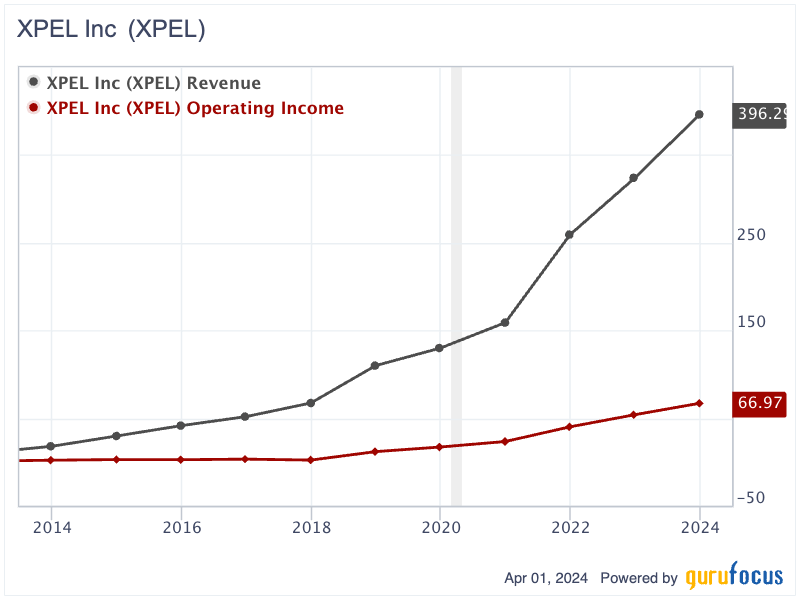

Over the broader timeline, XPEL has consistently grown its revenue each year for the past 10 years, increasing from $17.90 million in 2013 to $396.30 million in 2023, achieving a compounded annual growth rate of 36.30%. Similarly, its operating income has followed an upward trend, rising from $1.32 million in 2013 to $52.80 million in 2023.

The business growth over the past decade has been the result of the company's extensive international expansion, which began in 2014 with the establishment of an office in the U.K. In 2015, XPEL moved into the Canadian market by acquiring Parasol Canada. In 2016, it entered the European market by acquiring certain assets of Connectin Europe B.V. and established XPEL B.V. in the Netherlands. Over the subsequent two years, the company opened an office in Mexico and acquired Apogee Corp., establishing XPEL Asia in Taiwan.

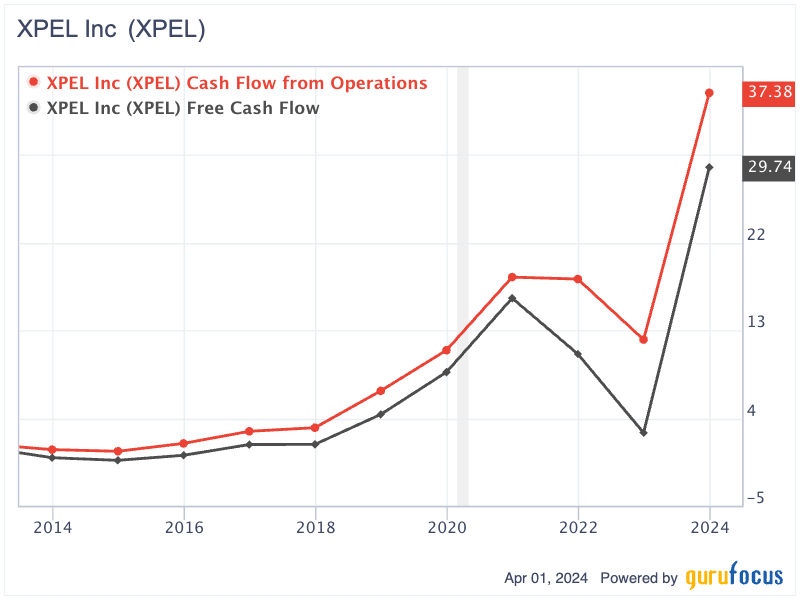

Although XPEL's operating cash flow and free cash flow have experienced huge volatility, they have been on the rise over the past decade. Its operating cash flow has skyrocketed from $0.77 million in 2013 to $37.38 million in 2023, while the free cash flow soared from -$6,000 to $29.74 million over the same period. In the past five years, XPEL has managed to grow its free cash flow by nearly 46.70% per year.

Impressive ROIC

The company has not only grown its revenue and operating income, generating increasing cash flow, but also delivered a high return on invested capital, which measures the rate of return on capital that company has invested. Over the last decade, XPEL's ROIC has been double digits for nine out of 10 years, oscillating between 16.50% and 61%. The only exception was in 2017, when its ROIC dipped to a low of 6.77%, which was attributed to a rise in operating costs. This increase included a one-time adjustment for consolidating three existing warehouses into a single facility and higher intercompany shipping expenses for inventory transfers between warehouses. In 2023, XPEL's ROIC rebounded to 28.53%.

Long-term growth investors always favor high ROIC businesses, and the long-term share price return would eventually be approximately equal to the ROIC of the underlying businesses.

As the late Charlie Munger one advised:

Over the long term, it's hard for a stock to earn a much better return that the business which underlies it earns. If the business earns six percent on capital over forty years and you hold it for that forty years, you're not going to make much different than a six percent return even if you originally buy it at a huge discount. Conversely, if a business earns eighteen percent on capital over twenty or thirty years, even if you pay an expensive looking price, you'll end up with one hell of a result.

Conservatively leveraged balance sheet

XPEL has quite strong, conservatively leveraged balance sheet. As of December 2023, it reported nearly $180 million in shareholders' equity and $11.60 million in cash. The majority of the company's obligations consist of lease liabilities totaling $16.70 million. The company recorded an outstanding balance of $19 million in its revolving credit facility and merely $379,000 in notes payable. Consequently, the debt-to-equity ratio is quite low at only 0.20. With its current cash flow generating capability, XPEL could settle its debt and lease obligations comfortably.

Potential upside

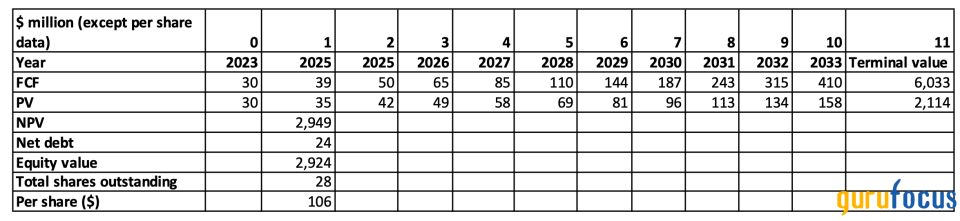

To value the stock, I used a discounted cash flow analysis. If XPEL can grow its free cash flow at a rate of 30% per year for the next 10 years, then the terminal growth rate would decrease to 3% per year afterwards. Using a 10% discount rate, I estimate its value to be nearly $2.95 billion. After adjusting for the current net debt of nearly $24 million, and with 28 million shares outstanding, the per-share intrinsic value of XPEL could be around $106, which is nearly 100% higher than its current trading price.

Source: Author's calculation

Key takeaway

XPEL has demonstrated its ability to not only consistently grow its revenue and cash flow, but also deliver high returns on invested capital, a key indicator for sustainable and profitable businesses. Moreover, the company possesses a strong balance sheet, with conservative leverage and significant shareholder equity. My discounted free cash flow analysis estimates XPEL could be worth $106 per share, suggesting a potential 100% upside from the current trading price. As a result, the stock can be considered a compelling opportunity for long-term investors.

This article first appeared on GuruFocus.