Yahoo Finance

Yahoo Finance Why Westport Fuel Systems Inc.'s Stock Has Plunged 30.1% So Far in 2018

What happened

Shares of natural gas transportation technology company Westport Fuel Systems Inc. (NASDAQ: WPRT) have fallen 30.1% in 2018, according to data from S&P Global Market Intelligence, as investors waver on whether the company is a long-term winner. So far, the bad has outweighed the good for Westport in 2018.

So what

The most consequential drop of the year came after first-quarter results were released. Revenue rose 13% to $67.7 million, but net loss from continuing operations improved only 1% to $12.7 million. Management has been cutting costs and selling its compressor business for $14.8 million to focus the business and reduce operating expenses. But shrinking operations and selling assets isn't a long-term growth strategy.

Image source: Getty Images.

Westport can cut costs short-term, but the real challenge is growing the business beyond the niche market it is today, which will take more investment. And if cost cuts don't lead to profitability now, it's unclear when the company could turn around.

Management expects to report positive adjusted EBITDA in the second quarter, which would be a good sign for the company overall. But after years of false starts for natural gas fuels, it's worth being cautious about management's projections.

Now what

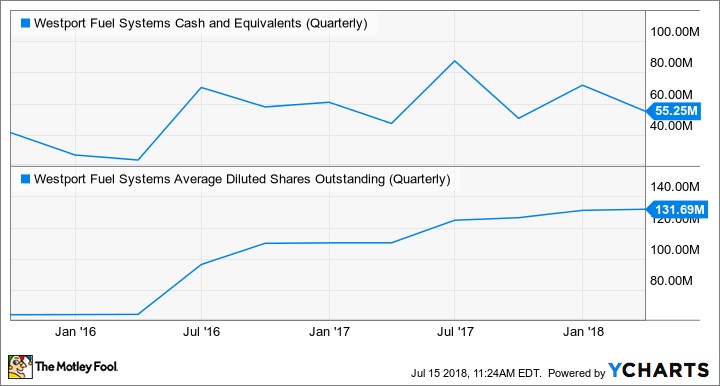

2018 will probably be volatile as investors weigh whether Westport's financial turnaround is happening fast enough. One thing to keep an eye on is the company's cash burn and cash level at the end of each quarter. Management has used dilutive share sales to maintain an acceptable cash level, which may be necessary later this year if cash generation doesn't improve.

WPRT Cash and Equivalents (Quarterly) data by YCharts

I'll take a wait-and-see approach to Westport's potential recovery, especially with a long history of disappointment for investors. Natural gas has a lot of potential to lower costs and clean up operations in long-haul trucking, but until we know it's going to be a profitable business, I'll remain skeptical that Westport will be a buy.

More From The Motley Fool

Travis Hoium has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.