Yahoo Finance

Yahoo Finance Why Should Investors Hold Cross Country Healthcare (CCRN) Now?

Cross Country Healthcare, Inc.’s CCRN growth is driven mainly by the number of healthcare professionals at work, increasing customer base and continued efforts to add shareholder value. Headwinds like labor shortages and softening markets are likely to affect the company.

The company has an impressive earning surprise history, beating the Zacks Consensus Estimate of earnings in all four trailing quarters, with an average surprise of 14.4%.

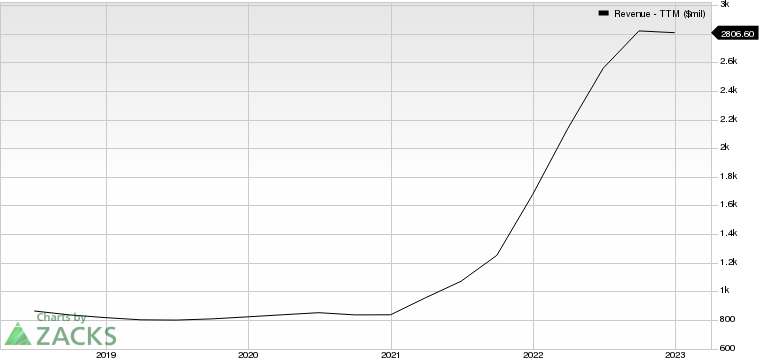

Cross Country Healthcare, Inc. Revenue (TTM)

Cross Country Healthcare, Inc. revenue-ttm | Cross Country Healthcare, Inc. Quote

Factors in Favour

Cross Country Healthcare has been putting efforts to increase technological capabilities in candidate engagement and customer-facing front. The company has been investing in recruitment and candidate nurturing tools, market analytics, mobile applications and self-serve capabilities, programmatic advertising, social media, and other technology. These investments are expected to enhance the recruitment capabilities of CCRN and take advantage of labor demand in various fields. Asset purchase agreements entered in 2022 include those with Mint Medical Physician Staffing, LP and Lotus Medical Staffing LLC, and HireUp Leadership, Inc.

Cross Country Healthcare has also collaborated with universities like Strayer University and Capella University to provide flexible degree programs to employees with affordable fees.

Cross Country Healthcare’s board of directors authorized a new stock repurchase program for $100 million of its shares. Of this authorized repurchase, 1.4 million shares for an aggregate price of $35.3 million have already been repurchased. In 2021 and 2020, the company did not repurchase any of its outstanding shares. In the fourth quarter of 2022, the company entered a Rule 10b5-1 Repurchase Plan to allow for share repurchases during its blackout periods.

Some Risks

Cross Country Healthcare’s current ratio at the end of the December quarter was 2.49, lower than 2.54 reported a year ago. A decline in the current ratio is not desirable as it indicates that the company may have problems meeting its short-term obligations.

In the last six months, CCRN plunged 29.8% against its industry’s 7.4% growth.

Zacks Rank and Stocks to Consider

CCRN currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader Zacks Business Services sector are Omnicom Group OMC, ICF International ICFI and Gartner, Inc. IT.

For first-quarter 2023, OMC’s earnings are anticipated to see a 41% increase from the year-ago reported figure to $1.96. The company’s earnings are expected to grow 3.6% on a year-over-year basis in 2023.

The Zacks Consensus Estimate for the company’s first-quarter 2023 earnings is pegged at $1.96, which has been revised slightly upward in the past 60 days. The consensus estimate for the full year is pegged at $7.18 per share. This has been revised upward 11.3% in the past 60 days. OMC currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

For first-quarter 2023, ICFI’s earnings are expected to increase 16% from the year-ago reported figure to $1.52. The company’s earnings are likely to grow 9.2% on a year-over-year basis in 2023.

The Zacks Consensus Estimate for the company’s first-quarter 2023 earnings is pegged at $1.52, which has been revised upward 2% in the past 60 days. The consensus estimate for the full year is pegged at $6.3 per share. This has been revised upward 7.3% in the past 60 days. The company currently sports a Zacks Rank of 1.

The Zacks Consensus Estimate for IT’s first-quarter 2023 earnings is pegged at $2.58, indicating 10.7% growth from the year-ago reported figure. This has been slightly revised upward in the past 60 days. The consensus estimate for the full year is pegged at $9.49 per share, which has been revised slightly upward in the past 60 days. The company currently carries a Zacks Rank #2 (Buy).

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicom Group Inc. (OMC) : Free Stock Analysis Report

Gartner, Inc. (IT) : Free Stock Analysis Report

Cross Country Healthcare, Inc. (CCRN) : Free Stock Analysis Report

ICF International, Inc. (ICFI) : Free Stock Analysis Report