Yahoo Finance

Yahoo Finance US Pensions Poised to Stock Up on Corporate Debt After Big Gains

(Bloomberg) -- US company pensions are poised to shift billions of dollars into corporate credit, after months of stock-market gains and higher bond yields have left them awash with cash, analysts and advisers said.

Most Read from Bloomberg

Saudis Warned G-7 Over Russia Seizures With Debt Sale Threat

Archegos’ Bill Hwang Convicted of Fraud, Market Manipulation

S&P 500 Tops 5,600 Mark in Longest Rally This Year: Markets Wrap

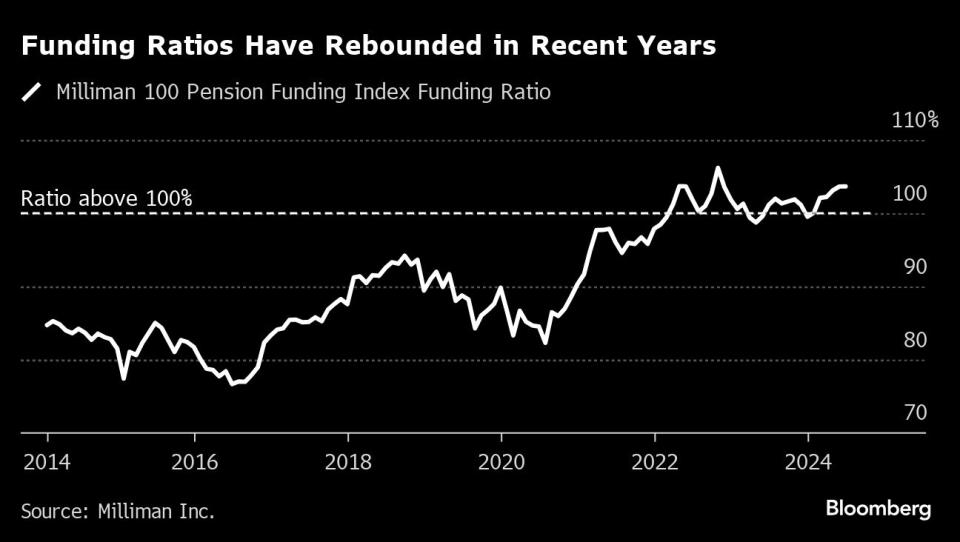

Corporate pension plans had 103.7% of the funding they need to meet obligations as of June, the highest level since 2022, according to the Milliman 100 Pension Funding Index. That metric has dropped below 100% only four times since March 2022. Big gains in US stocks have helped, with the S&P 500 up about 18% this year on a total return basis.

Such flushness typically leads retirement-fund managers to move resources away from higher-risk assets, like equities, and into bonds. Credit strategists are already seeing some movement at the margins, with pension funds seeking out investment-grade corporate bonds and other products that allow them to lock in current high yields to help fund their long-term obligations.

“I would certainly expect more corporate bond buying from pension funds if these levels are upheld,” said James Martin, US credit strategist at UBS.

Demand from company pension funds, which control more than $3 trillion, is at least one reason why valuations for US corporate bonds are so high now — even after the Federal Reserve has in the last two years lifted rates at the fastest pace since the 1980s. As of Tuesday average investment-grade spreads, or risk premiums, were just 90 basis points, or 0.9 percentage point, according to Bloomberg index data. That’s well below the 10-year average of 123 basis points.

Pension managers typically need to see funding levels above 100% for a few quarters before shifting allocations, Martin said. Levels at the largest corporate pensions have been above 100% since January, according to the Milliman index.

Fixed income products account for about 54% of defined-benefit portfolios, said Mike Moran, senior pension strategist at Goldman Sachs Asset Management. It’s the highest level he’s seen in his 25 years working with pensions, and he expects it to grow further.

The historical rule of thumb was that once a pension reaches an 80% funding level, its manager would start shifting out of stocks and into bonds. But pension managers are often cautious about making sudden changes to their portfolios.

The 2008 crash put many funds on life support. A long period of rock-bottom interest rates hurt their ability to catch up with portfolios that, by nature, are heavily weighted in fixed-income products.

Some pension managers were squarely focused on meeting immediate obligations for retirees until a federal program came to their aid a few years ago. Signed into law in 2021, the American Rescue Plan Act provided funds for the US government’s Pension Benefit Guaranty Corporation to distribute an estimated $97 billion into 250 distressed multi-employer pension plans. Not all of the money is distributed yet, but the aid has shifted focus back to long-term investments for many plans.

“Put yourself in the shoes of a pension-fund manager,” said Daniel Sorid, Citi’s investment-grade credit strategist. “Yesterday you were close to insolvency, but then once the federal government cuts a check, you’re more or less fully funded and all of a sudden your asset allocation needs to shift.”

Sorid has not seen a meaningful change in pension fund assets yet, but he expects managers to start buying more corporate bonds soon. The PBGC is reviewing $13 billion worth of additional funding requests that could be paid out by August, and roughly $2 billion of that should flow into investment-grade debt, Sorid wrote in a recent report.

“Even if it doesn’t fully materialize, it always hangs out there as this potential new demand source and helps to support the market,” he said.

Time to De-risk

To Goldman’s Moran, this period is reminiscent of robust funding levels before the financial crisis in 2008 or even before the dot-com bubble burst in 2000. In his view, there is no better time for pension managers to de-risk.

He has already seen evidence that they are more interested in steadier debt products that align better with their liabilities, like investment-grade corporate bonds and zero coupon Treasuries known as STRIPS, which are sold at a discount to face value and don’t make payments until they mature.

“This is a period of strength, a position of strength, for plan sponsors, and history shows us that the position of strength can sometimes be fleeting,” Moran said. “So it’s important for plans to take actions.”

Most Read from Bloomberg Businessweek

At SpaceX, Elon Musk’s Own Brand of Cancel Culture Is Thriving

Ukraine Is Fighting Russia With Toy Drones and Duct-Taped Bombs

©2024 Bloomberg L.P.