Yahoo Finance

Yahoo Finance US homeownership rate still below pre-recession peak: LendingTree

Despite record-low mortgage rates, the U.S. homeownership rate is still lower than it was before the housing crash of 2008, and mortgage spending is at an all-time low.

In fact, several metrics show that borrowers and lenders are still hesitant to take action after the Great Recession, according to a new study by LendingTree, a Charlotte, N.C.-based online lending marketplace.

“There are a lot of folks who are ‘once bitten twice shy’,” said LendingTree Chief Economist Tendayi Kapfidze, who noted that part of the difference is because permissive lending created an unhealthy run-up in the homeownership rate before the crisis.

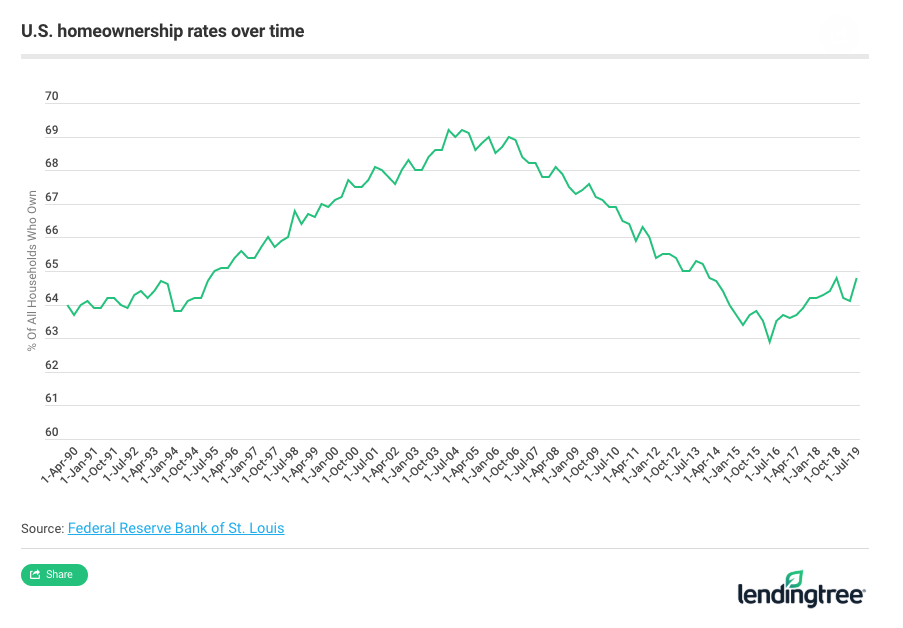

The homeownership rate, 64.8%, is still 4 percentage points shy of pre-recession highs, according to LendingTree. Another metric of housing health, the rate at which people move, was at an all time low of only 9.78% in 2019, compared to 11.9% in 2008, according to U.S. Census data.

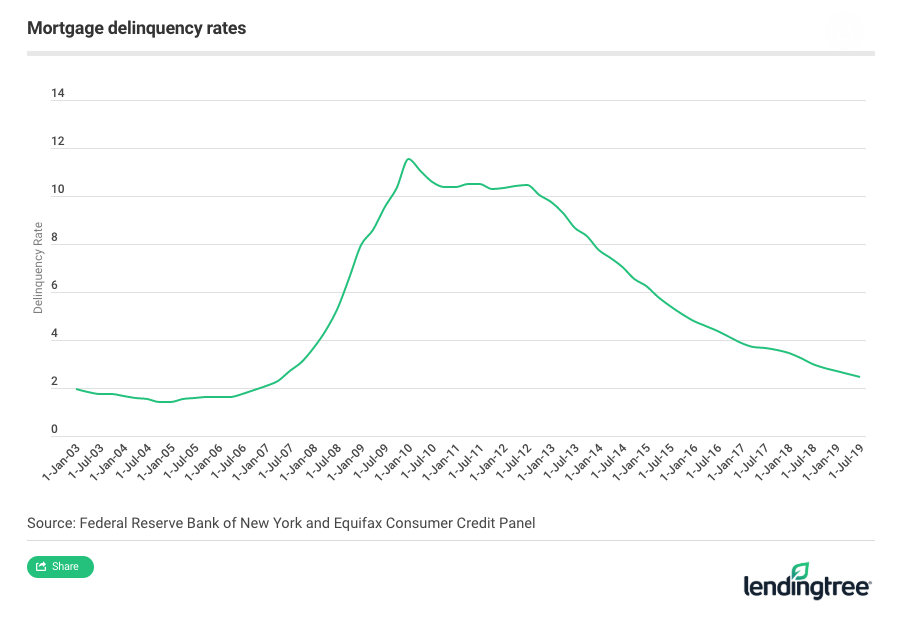

Home purchases are down because homeowners are watching their budgets and taking on less debt, statistics show. Only 2.45% of mortgage holders were delinquent in 2019, the lowest level in a decade — mortgage delinquency rate was as high as 11.5% in 2010, according to LendingTree. And despite skyrocketing home values, surpassing its pre-crisis peak of $14.4 trillion to reach $18.7 trillion in 2019, homeowners are taking on less debt against their home, said Kapfidze.

“Because home prices have appreciated, people could be accessing equity more easily, but they aren’t,” said Kapfidze.

Mortgage spending is at an all-time low in the U.S. economy, partially because debt-to-income standards for lending are higher, said Kapfidze. Americans spent only 4.1% of disposable household income on their mortgage payments in 2019, the lowest percentage since the Federal Reserve began tracking the data in 1980.

Mortgage lending standards are tighter than they were pre-crisis. In 2019, fewer than one in 10 mortgages went to subprime borrowers, compared to one in five pre-crisis. Meanwhile, 61% of mortgages now go to borrowers with a credit score over 760, compared to only 28% before the crisis, according to LendingTree.

“Lending standards are much tighter. You need pretty good credit now, and there are not a lot of exotic products that increase affordability,” said Kapfidze.

-

Sarah Paynter is a reporter at Yahoo Finance. Follow her on Twitter @sarahapaynter

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.

More from Sarah:

Home prices could rise in 2020, say experts