Yahoo Finance

Yahoo Finance The U.S. Silica Holdings (NYSE:SLCA) Share Price Is Down 82% So Some Shareholders Are Rather Upset

As an investor, mistakes are inevitable. But really bad investments should be rare. So spare a thought for the long term shareholders of U.S. Silica Holdings, Inc. (NYSE:SLCA); the share price is down a whopping 82% in the last three years. That would be a disturbing experience. And more recent buyers are having a tough time too, with a drop of 56% in the last year. The falls have accelerated recently, with the share price down 35% in the last three months.

While a drop like that is definitely a body blow, money isn't as important as health and happiness.

See our latest analysis for U.S. Silica Holdings

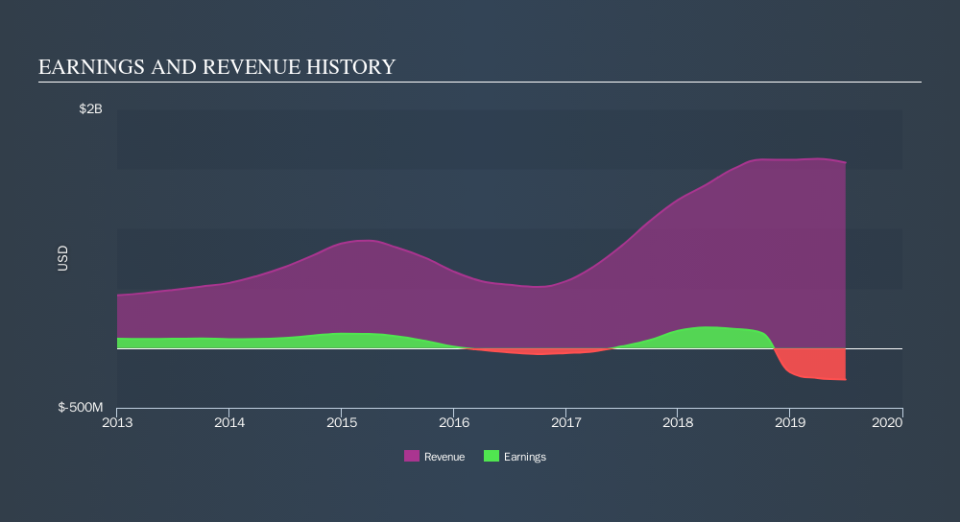

U.S. Silica Holdings isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally expect to see good revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

Over three years, U.S. Silica Holdings grew revenue at 39% per year. That is faster than most pre-profit companies. So why has the share priced crashed 44% per year, in the same time? The share price makes us wonder if there is an issue with profitability. Ultimately, revenue growth doesn't amount to much if the business can't scale well. If the company is low on cash, it may have to raise capital soon.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

We consider it positive that insiders have made significant purchases in the last year. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. If you are thinking of buying or selling U.S. Silica Holdings stock, you should check out this free report showing analyst profit forecasts.

A Different Perspective

While the broader market gained around 1.7% in the last year, U.S. Silica Holdings shareholders lost 55% (even including dividends) . Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 28% over the last half decade. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. It is all well and good that insiders have been buying shares, but we suggest you check here to see what price insiders were buying at.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.