Yahoo Finance

Yahoo Finance U.S. Bancorp (USB) Rides on Solid Deposit Base, High Costs Ail

U.S. Bancorp’s USB robust loan pipeline, investment portfolio repositioning efforts and stable deposits are likely to enhance net interest income (NII). Diverse revenue streams and rising fee income are expected to support top-line growth. However, an escalating expense base remains a concern.

U.S. Bancorp has experienced strong growth in total loans and deposits in the past few years. This growth is mainly driven by efforts to strengthen relationships with existing customers, acquire new ones and increase market share. Total deposits also increased on a year-over-year basis, reflecting improvements in total savings deposits, time deposits and noninterest-bearing deposits. Management anticipates strong loan pipelines in the commercial and credit card space to drive growth in the upcoming period.

USB’s organic growth and diversified revenue streams are its key strengths. Revenues witnessed a compound annual growth rate (CAGR) of 10.4% over the last four years (ended 2023), primarily driven by higher NII. Although NII decreased during the first quarter of 2024, investment portfolio repositioning, improved loan demand and lower deposit migration are likely to bolster the metric going forward. Additionally, USB’s efforts to enhance its range of products, services and capabilities will support fee income growth. Hence, the company is well-positioned to improve its revenue trend backed by growth in fee income and NII.

U.S. Bancorp has a strong balance sheet. As of Mar 31, 2024, the company had a long-term debt of $52.69 billion, while cash and due from banks was $76.99 billion during the same period. This reflected a strong liquidity position. Given the company’s strong liquid profile and favorable debt-to-equity ratio, its capital distribution activities seem sustainable.

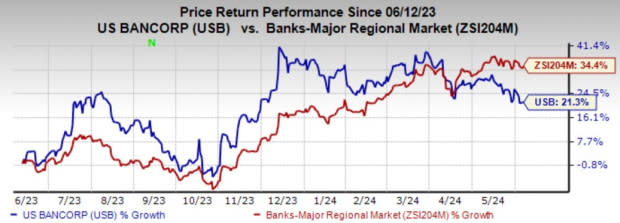

USB currently carries a Zacks Rank #3 (Hold). Shares of the company have gained 21.3% over the past year compared with the industry’s growth of 34.4%

.

Image Source: Zacks Investment Research

However, increased expenses from merger and integration charges, compensation and benefits, occupancy and equipment, and technology and communications remain a concern for the company. The company's non-interest expenses witnessed a 10% CAGR from 2019 to 2023. Although net interest expenses declined in the first quarter, the increase in technology-led initiatives will continue to elevate U.S. Bancorp’s cost base, potentially impeding the bottom-line growth.

U.S. Bancorp’s trailing 12-month return on equity (ROE) undercuts its growth potential. The company’s ROE of 13.93% compares unfavorably with that of the S&P 500’s 16.63%, highlighting that it is less efficient in using shareholders’ funds.

Stocks to Consider

Some better-ranked stocks from the finance space are UMB Financial Corporation UMBF and Bank of America Corporation BAC.

UMBF’s 2024 earnings estimates have risen 14.4% over the past 60 days. Shares of UMBF have gained 6.2% over the past six months. Currently, UMBF sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

BAC’s 2024 earnings estimates have risen marginally over the past seven days. Shares of BAC have gained 28.9% over the past six months. At present, BAC carries a Zacks Rank #2 (Buy).

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC) : Free Stock Analysis Report

U.S. Bancorp (USB) : Free Stock Analysis Report

UMB Financial Corporation (UMBF) : Free Stock Analysis Report