Yahoo Finance

Yahoo Finance Here’s My Top Value Stock to Buy Right Now

Written by Brian Paradza, CFA at The Motley Fool Canada

Investors who wish to deploy new capital and buy cheaply valued stocks for retirement portfolios should check out Parex Resources (TSX:PXT) stock. It’s one of my top Canadian value stocks to buy right now. Its dividend yield is juicy for passive income, its cash flow generation machines are well oiled in the Colombian oilfields, and its aggressive share repurchase program could potentially unlock high upside over the next few years – if oil prices cooperate.

The company is a $2.4 billion oil and gas mining stock with production assets located in Colombia. Growing production, higher free cash flow, and investor-friendly capital budgeting policies make PXT stock an attractive value play, especially following its momentary drop in January 2024 – due to temporary causes.

Why did Parex Resources stock fall in January

Parex Resources’ stock price declined almost 16% on January 16 following the company’s release of its 2023 production numbers and financial guidance for 2024. Fourth quarter production of 57,329 barrels of oil equivalent per day (boe/d) increased by 6% year over year, but it unfortunately missed management’s guidance for 60,000 boe/d provided on November 7 last year. Disappointed traders punished the stock.

Management blamed “slower onstream timing because of extended testing and operational setbacks, as well as higher than expected water cut on a single high-rate well” for the target miss. Production hiccups do happen. The causes are temporary, and may not matter for a long-term oriented investor with a 5-to-10 year holding period.

Growing profitability, higher equity value, and growing dividends

Parex Resources is a low-cost oil producer that may remain highly profitable and cash flow positive for a long time. Data from its latest financial guidance indicates that operating netbacks for 2024 could exceed US$29 per boe and reach US$33 per boe if Brent Crude prices range between US$75 and US$85 per barrel for 2024.

The Brent Crude price hovered above US$83 at the time of writing.

Productivity growth and sustained profitability allowed the company to grow its balance sheet and increase shareholders’ equity from $1.7 billion at the end of 2018 to $2.5 billion by September last year, and triple its regular quarterly dividend from $0.13 per share in 2021 to $0.38 per share currently.

Another five years of good oil prices may richly reward PXT investors.

Buy the dip on Parex Resources stock

Parex Resources is cheaply priced today given a price-to-earnings multiple of 3.2, which is far lower than the average industry PE multiple of 8.5. The stock’s 6.5% dividend yield could double one’s investment in 11 years (the Rule of 72 predicts). The small-cap energy stock could gift investors through growing capital gains as well aggressive share repurchases.

Management targets executing for an average production growth rate of 5% per annum through 2026. The company has been hitting new annual productivity records, raising its dividends, and aggressively repurchasing its shares over the past four years. But the market cheaply values PXT relative to Canadian peers, even as the company’s positioned to fetch premium prices for its production in 2024.

What premium prices? Parex Resources sells its growing production at much higher prices than Canadian firms. It prices its daily production at London’s Brent Crude Oil Index, where prices are usually higher than on North American oil indices, including the West Texas Intermediate (WTI) index. High energy prices in Europe could persist for longer – pushed up by persistent political instability in areas around key trade routes, providing a tailwind for PXT’s profitability growth.

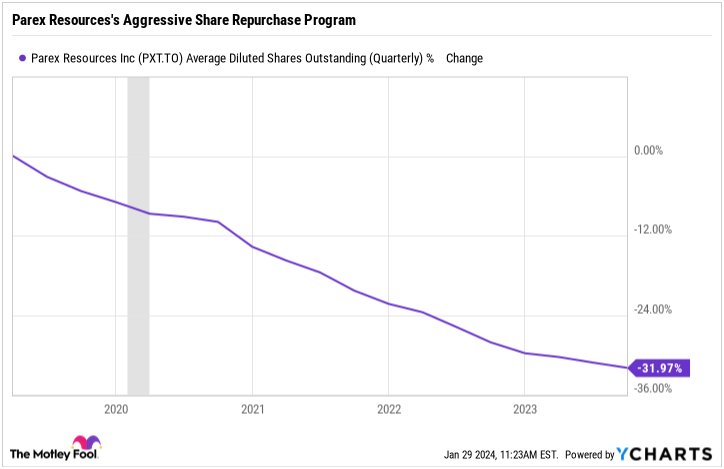

Most noteworthy, the company is aggressively repurchasing its shares. It reduced its outstanding shares by 32% over the past five years, and recently received regulatory authorization to repurchase up to 9.8% of its total shares outstanding this year.

Fewer shares mean fewer claims on its assets, future earnings, and cash flow. This, the remaining shares should be more valuable over time.

Risks to watch

Gyrations in global oil prices are almost guaranteed. Lower oil prices could eat into Parex Resources’ lucrative earnings margins and slow down its share repurchases. However, upside risks may include lucrative resource discoveries as the company explores oil on three high-risk high-reward assets in 2024. The downside risks include the stock market’s sustained huge discounts on the Colombian oil producer – limiting the capital gains on the investment.

That said, the dividend is well covered given a low earnings payout rate of 19%.

The post Here’s My Top Value Stock to Buy Right Now appeared first on The Motley Fool Canada.

Should You Invest $1,000 In Parex Resources Inc?

Before you consider Parex Resources Inc, you'll want to hear this.

Our market-beating analyst team just revealed what they believe are the 10 best starter stocks for investors to buy in 2024... and Parex Resources Inc wasn't on the list.

The online investing service they've run for a decade, Motley Fool Stock Advisor Canada, is beating the TSX by 32 percentage points. And right now, they think there are 10 stocks that are better buys.

Get Our 10 Starter Stocks Today * Returns as of 12/22/23

More reading

Can You Guess the 10 Most Popular Canadian Stocks? (If You Own Them, You Might Be Losing Out.)

How to Build a Bulletproof Monthly Passive-Income Portfolio in 2024 With Just $25,000

Fool contributor Brian Paradza has no position in any of the stocks mentioned. The Motley Fool recommends Parex Resources. The Motley Fool has a disclosure policy.

2024