Yahoo Finance

Yahoo Finance Top 3 Stocks Estimated To Be Below Their True Value In June 2024

As global markets continue to navigate through a mix of political turmoil in Europe and mixed economic signals from major economies, investors are keenly watching for opportunities that may be undervalued in such a fluctuating landscape. In this context, identifying stocks that are estimated to be below their true value could offer potential avenues for those looking to invest amidst current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows

Name | Current Price | Fair Value (Est) | Discount (Est) |

Kuaishou Technology (SEHK:1024) | HK$49.35 | HK$98.60 | 49.9% |

Noble (NYSE:NE) | US$44.55 | US$88.41 | 49.6% |

RaySearch Laboratories (OM:RAY B) | SEK140.00 | SEK279.05 | 49.8% |

Componenta (HLSE:CTH1V) | €3.05 | €6.07 | 49.8% |

Cloudia Research (BIT:AGAIN) | €2.90 | €5.79 | 49.9% |

Guerbet (ENXTPA:GBT) | €36.10 | €71.57 | 49.6% |

Interojo (KOSDAQ:A119610) | ₩24900.00 | ₩49536.65 | 49.7% |

Musti Group Oyj (HLSE:MUSTI) | €25.40 | €50.47 | 49.7% |

HeartCore Enterprises (NasdaqCM:HTCR) | US$0.7092 | US$1.40 | 49.5% |

Loungers (AIM:LGRS) | £2.68 | £5.33 | 49.7% |

Here's a peek at a few of the choices from the screener

UPM-Kymmene Oyj

Overview: UPM-Kymmene Oyj operates globally in the forest-based bioindustry, with a market capitalization of approximately €18.11 billion.

Operations: UPM-Kymmene Oyj's revenue is generated through various segments including UPM Energy (€0.68 billion), UPM Fibres (€3.22 billion), UPM Plywood (€0.40 billion), UPM Raflatac (€1.50 billion), UPM Specialty Papers (€1.48 billion), and UPM Communication Papers (€3.32 billion).

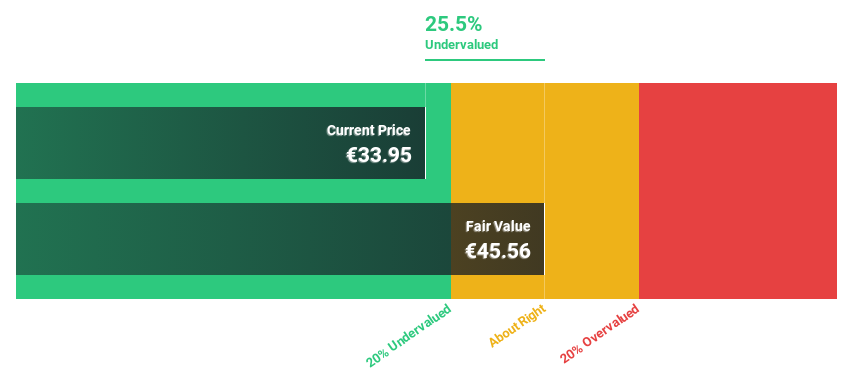

Estimated Discount To Fair Value: 25.5%

UPM-Kymmene Oyj, priced at €33.95, is considered undervalued with a fair value estimate of €45.56 based on discounted cash flow analysis. Despite slower revenue growth projections at 3.8% annually versus the Finnish market's 3.1%, UPM's earnings are expected to increase by 22.8% per year, outpacing the local market forecast of 14.8%. However, its current dividend coverage is weak, and profit margins have declined from last year’s 13.1% to 4.7%. Recent executive changes and a stable dividend policy may impact future performance dynamics.

AIA Group

Overview: AIA Group Limited, together with its subsidiaries, offers life insurance-based financial services and has a market capitalization of approximately HK$622.20 billion.

Operations: The company generates HK$19.76 billion from its life insurance operations.

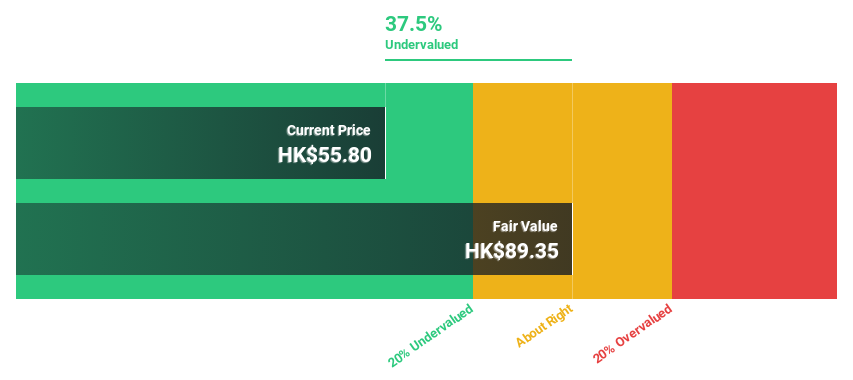

Estimated Discount To Fair Value: 37.5%

AIA Group, trading at HK$55.8 against a fair value of HK$89.35, is seen as undervalued based on discounted cash flow, with potential for a 69.1% price increase per analysts' consensus. Its earnings are expected to grow by 17.1% annually, surpassing Hong Kong's market growth rate of 11.6%. Recent strategic share repurchases aimed at enhancing shareholder value underscore its proactive management approach amidst robust revenue growth projections of 26.4% annually, significantly outpacing the local market forecast of 7.8%.

Our growth report here indicates AIA Group may be poised for an improving outlook.

Get an in-depth perspective on AIA Group's balance sheet by reading our health report here.

Dino Polska

Overview: Dino Polska S.A. operates a network of mid-sized grocery supermarkets in Poland, with a market capitalization of approximately PLN 39.88 billion.

Operations: The primary revenue source for the company comes from its retail network, generating PLN 26.79 billion in sales.

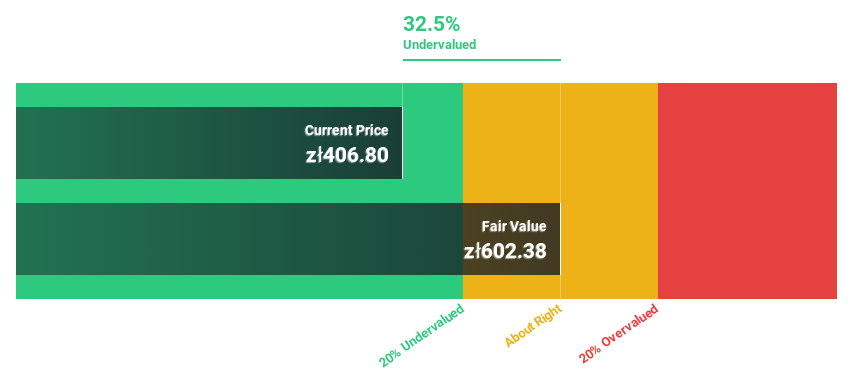

Estimated Discount To Fair Value: 32.5%

Dino Polska S.A., with a current trading price of PLN 406.8, is perceived as undervalued, positioned 32.5% below its calculated fair value of PLN 602.38. This valuation comes amidst a backdrop of strong financial performance, including a year-over-year net income increase and significant store expansions, reflecting an aggressive growth strategy. The company's earnings are anticipated to rise by 18.72% annually, outpacing the Polish market's forecasted growth. Despite robust revenue and profit growth rates exceeding market averages, Dino's stock remains attractively priced based on cash flow analyses.

Make It Happen

Navigate through the entire inventory of 953 Undervalued Stocks Based On Cash Flows here.

Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include HLSE:UPM SEHK:1299 and WSE:DNP.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com