Yahoo Finance

Yahoo Finance Three Reasons to Retain Merit Medical (MMSI) Stock for Now

Merit Medical Systems, Inc. MMSI is well-poised for growth in the coming quarters, courtesy of its strong product portfolio. The optimism led by solid first-quarter 2024 performance and its continued spend on research and development (R&D) are expected to contribute further. However, headwinds due to higher consolidation in the healthcare industry and forex volatility persist.

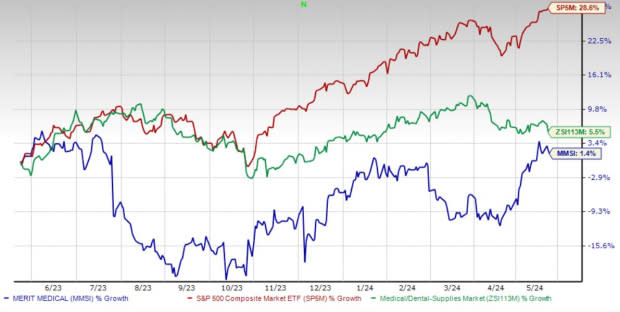

Over the past year, this Zacks Rank #3 (Hold) stock has gained 1.4% compared with a 5.5% rise of the industry and 28.6% growth of the S&P 500.

The renowned medical device provider has a market capitalization of $4.78 billion. The company projects 10.8% growth for the next five years and expects to maintain its strong performance. It has delivered an earnings surprise of 9.3% for the past four quarters, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strong Q1 Results: Merit Medical’s robust first-quarter 2024 results buoy optimism. The company witnessed a year-over-year uptick in the top and bottom lines. The company also saw revenue growth in both its segments and across the majority of the product categories within its Cardiovascular unit. Robust performances in the United States and outside were also registered. The expansion of both margins was also recorded.

Strong Product Portfolio: Merit Medical has continued to gain significant momentum on the back of new products, raising our optimism. This month, the company announced the U.S. commercial release of the basixSKY Inflation Device.

The same month, Merit Medical received the FDA’s 510(k) clearance for its Siege Vascular Plug. The company also announced the launch of its Bearing nsPVA Express Prefilled Syringe in the United States and Australia.

Continued Spend on R&D: Merit Medical’s R&D operations have been central to its historical growth and are believed to be critical to its continued growth. In recent years, the company’s focus on innovation has led to the introduction of several new products, improvements to its existing products, and expansion of its product lines, as well as enhancements and new equipment in its R&D facilities. This raises our optimism.

Downsides

Higher Consolidation in the Healthcare Industry: Healthcare costs have risen significantly over the past decade. Thus, to provide healthcare solutions at a cheaper rate and eradicate competition, large-cap MedTech behemoths have started consolidating with mid-cap and small-cap companies. This enables the availability of healthcare products at cheap prices in the market. Per management, such trends compel Merit Medical’s customers to ask for price concessions on its products, which act against the ongoing business strategies. This may also exert a solid downward pressure on the prices of Merit Medical’s products and reduce the customer base.

Forex Volatility: Merit Medical’s operations outside the United States have made it increasingly subject to market risk relating to foreign currency, which could have a negative impact on its margins and financial results. If the rate of exchange between foreign currencies declines against the U.S. dollar, Merit Medical may not be able to increase the prices charged from its customers for products whose prices are denominated in those respective foreign currencies.

Estimate Trend

Merit Medical is witnessing a positive estimate revision trend for 2024. In the past 90 days, the Zacks Consensus Estimate for its earnings per share has moved a penny north to $3.33.

The Zacks Consensus Estimate for the company’s second-quarter 2024 revenues is pegged at $335.1 million, suggesting a 4.7% rise from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, Boston Scientific Corporation BSX and Ecolab Inc. ECL.

DaVita, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 13.6%. DVA’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 29.4%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

DaVita’s shares have gained 40.4% compared with the industry’s 24.5% rise in the past year.

Boston Scientific, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 12.5%. BSX’s earnings surpassed estimates in each of the trailing four quarters, with the average being 7.5%.

Boston Scientific has gained 46.9% compared with the industry’s 1.4% rise in the past year.

Ecolab, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 14.3%. ECL’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 1.3%.

Ecolab’s shares have rallied 40.1% against the industry’s 7.2% decline in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

Ecolab Inc. (ECL) : Free Stock Analysis Report

DaVita Inc. (DVA) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report