Yahoo Finance

Yahoo Finance This week in Trumponomics: The V-shaped recovery is gone

The coronavirus recession began with the sharpest economic contraction on record—a 32.9% drop in second quarter GDP, on an annualized basis. The second-worst drop in GDP was a mere 10% decline, back in 1958.

That’s about as steep as a V-shaped recession can get. Two months ago, there was reasonable hope that the recovery might be as sharp as the decline, or close to it. But that was only possible if the first coronavirus outbreak, on the east and west coasts and a few other hotspots, was the end of it. Alas, the virus is spreading rather than receding, and killing the recovery along with thousands of Americans.

Economists knew this week’s GDP report for the second quarter was going to be bad. More surprising, and worrisome, is new data showing the labor market recovery is petering out. “The outlook for the labor market has darkened in recent weeks,” Moody’s Analytics wrote on July 30. Initial claims for unemployment insurance, which measure people newly out-of-work, are at extremely high levels, and rose again this week instead of falling. A separate metric measuring the ongoing number of unemployed rose as well.

It’s not surprising why these job numbers are going in the wrong direction. Coronavirus infection rates are rising in at least 25 states, making it impossible for the economy to get back to normal. More than 152,000 Americans have died of the virus, including, this week, restarauteur and former presidential candidate Herman Cain. Lockdowns remain patchy and inconsistent, and coronavirus testing is becoming more scarce and taking longer as caseloads surge.

President Trump seems paralyzed. He had nothing to say about this week’s dreadful GDP report, and it’s obvious he’s not going to implement a national testing strategy or use federal power to deliver a dramatic increase in tests, as many public health experts have been pleading for. What Trump did do this week is suggest postponing the November election, perhaps as a distraction from the horrible economic news. It won’t happen, but Trump sometimes drops such stink bombs to change the conversation, which he did for about 12 hours.

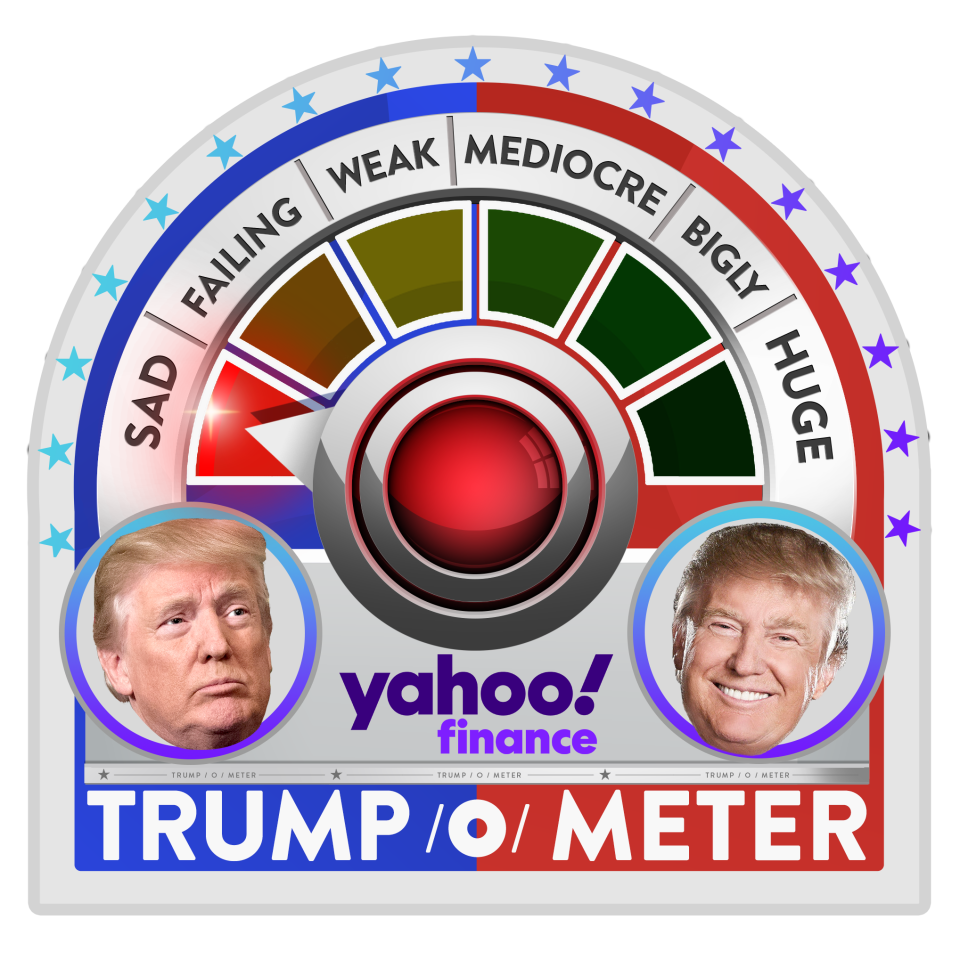

At the same time, Trump insists schools should fully reopen in a few weeks, as if everything’s fine, even though 1,000 Americans are dying every day from the virus. That’s the equivalent of three fully loaded jumbo jets crashing, every day. With China and most developed nations containing the virus much better than the United States, it’s becoming clear we could be mired in recession until a vaccine becomes widely available. This week’s Trump-o-meter reads SAD, the lowest official rating.

Forecasting firm Oxford Economics runs a state-by-state recovery tracker, which showed the economy bottoming out in early April and improving steadily through mid-June. That recovery has since stalled, however. “After a very rapid first phase of the recovery,” Oxford reported on July 30, “the economy has entered the second rehabilitation phase with much less momentum and a dire need for further fiscal support.” Every region except the Northeast declined in the latest weekly tracking data, with the South performing worst, followed by the Southwest and the mountain states. Even the Midwest is going backwards slightly as cases spread there.

Congress is negotiating yet another stimulus bill, likely to total $1.5 trillion or more, on top of $3.7 trillion authorized so far. There’s sharp disagreement between Republicans and Democrats over what should get further funding, but it seems likely there will be more stimulus checks for families, more enhanced unemployment aid and billions for states and cities by the time Congress is due to leave town on August 7.

That stimulus dwarfs anything from the last 80 years, yet at best it will prevent a bad downturn from getting worse. A robust recovery is not in sight. “Look at how money is being earned,” economist Joel Naroff of Naroff Economics wrote to clients this week. “It is by handouts. We have the largest welfare economy in U.S. history, but it was implemented to pay for current spending and keep us from a total collapse. Congress and the president must ask: How well is the economy capable of standing on its own?” Or maybe they shouldn’t, because the answer isn’t a happy one.

Rick Newman is the author of four books, including “Rebounders: How Winners Pivot from Setback to Success.” Follow him on Twitter: @rickjnewman. Confidential tip line: rickjnewman@yahoo.com. Encrypted communication available. Click here to get Rick’s stories by email.

Read more:

Get the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.