Yahoo Finance

Yahoo Finance Strong week for Grab Holdings (NASDAQ:GRAB) shareholders doesn't alleviate pain of one-year loss

While not a mind-blowing move, it is good to see that the Grab Holdings Limited (NASDAQ:GRAB) share price has gained 29% in the last three months. But that's small comfort given the dismal price performance over the last year. Like an arid lake in a warming world, shareholder value has evaporated, with the share price down 53% in that time. So the bounce should be viewed in that context. It may be that the fall was an overreaction.

The recent uptick of 5.8% could be a positive sign of things to come, so let's take a look at historical fundamentals.

Check out our latest analysis for Grab Holdings

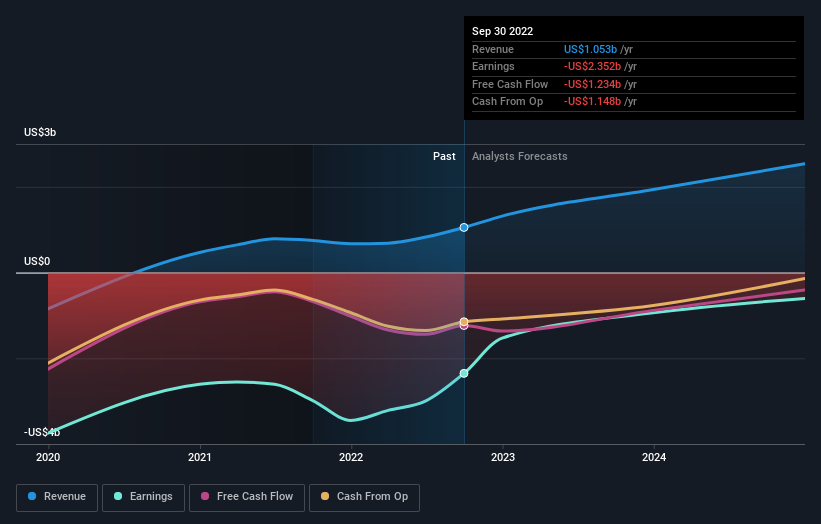

Because Grab Holdings made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually expect strong revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

In the last year Grab Holdings saw its revenue grow by 41%. That's definitely a respectable growth rate. Meanwhile, the share price tanked 53%, suggesting the market had much higher expectations. It is of course possible that the business will still deliver strong growth, it will just take longer than expected to do it. To our minds it isn't enough to just look at revenue, anyway. Always consider when profits will flow.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

Grab Holdings is a well known stock, with plenty of analyst coverage, suggesting some visibility into future growth. You can see what analysts are predicting for Grab Holdings in this interactive graph of future profit estimates.

A Different Perspective

We doubt Grab Holdings shareholders are happy with the loss of 53% over twelve months. That falls short of the market, which lost 23%. That's disappointing, but it's worth keeping in mind that the market-wide selling wouldn't have helped. Putting aside the last twelve months, it's good to see the share price has rebounded by 29%, in the last ninety days. Let's just hope this isn't the widely-feared 'dead cat bounce' (which would indicate further declines to come). I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For instance, we've identified 2 warning signs for Grab Holdings that you should be aware of.

But note: Grab Holdings may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here