Yahoo Finance

Yahoo Finance Source Rock Royalties (CVE:SRR) Is Increasing Its Dividend To CA$0.0065

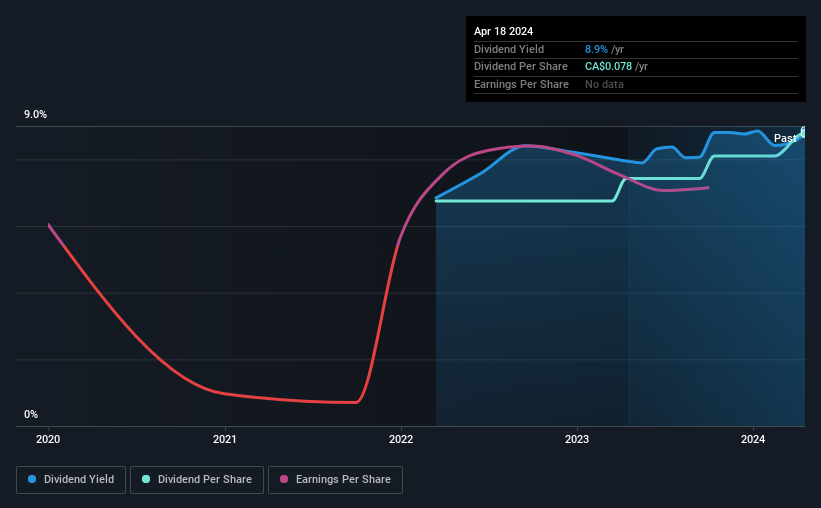

Source Rock Royalties Ltd. (CVE:SRR) has announced that it will be increasing its periodic dividend on the 15th of May to CA$0.0065, which will be 18% higher than last year's comparable payment amount of CA$0.0055. This makes the dividend yield 8.9%, which is above the industry average.

Check out our latest analysis for Source Rock Royalties

Source Rock Royalties Doesn't Earn Enough To Cover Its Payments

A big dividend yield for a few years doesn't mean much if it can't be sustained. Based on the last payment, earnings were actually smaller than the dividend, and the company was actually spending more cash than it was making. Paying out such a large dividend compared to earnings while also not generating free cash flows is a major warning sign for the sustainability of the dividend as these levels are certainly a bit high.

Earnings per share could rise by 21.8% over the next year if things go the same way as they have for the last few years. However, if the dividend continues along recent trends, it could start putting pressure on the balance sheet with the payout ratio reaching 172% over the next year.

Source Rock Royalties Is Still Building Its Track Record

Looking back, the dividend has been stable, but the company hasn't been paying a dividend for very long so we can't be confident that the dividend will remain stable through all economic environments. The annual payment during the last 2 years was CA$0.06 in 2022, and the most recent fiscal year payment was CA$0.078. This means that it has been growing its distributions at 14% per annum over that time. The dividend has been growing rapidly, however with such a short payment history we can't know for sure if payment can continue to grow over the long term, so caution may be warranted.

Source Rock Royalties Might Find It Hard To Grow Its Dividend

Investors could be attracted to the stock based on the quality of its payment history. Source Rock Royalties has impressed us by growing EPS at 22% per year over the past five years. Strong earnings is nice to see, but unless this can be sustained on minimal reinvestment of profits, we would question whether dividends will follow suit.

The Dividend Could Prove To Be Unreliable

In summary, while it's always good to see the dividend being raised, we don't think Source Rock Royalties' payments are rock solid. While we generally think the level of distributions are a bit high, we wouldn't rule it out as becoming a good dividend payer in the future as its earnings are growing healthily. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 5 warning signs for Source Rock Royalties (2 are a bit unpleasant!) that you should be aware of before investing. Is Source Rock Royalties not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.