Yahoo Finance

Yahoo Finance Silicon Laboratories (NASDAQ:SLAB) shareholders are still up 32% over 5 years despite pulling back 4.6% in the past week

When you buy and hold a stock for the long term, you definitely want it to provide a positive return. Furthermore, you'd generally like to see the share price rise faster than the market. But Silicon Laboratories Inc. (NASDAQ:SLAB) has fallen short of that second goal, with a share price rise of 32% over five years, which is below the market return. The last year has been disappointing, with the stock price down 11% in that time.

While the stock has fallen 4.6% this week, it's worth focusing on the longer term and seeing if the stocks historical returns have been driven by the underlying fundamentals.

View our latest analysis for Silicon Laboratories

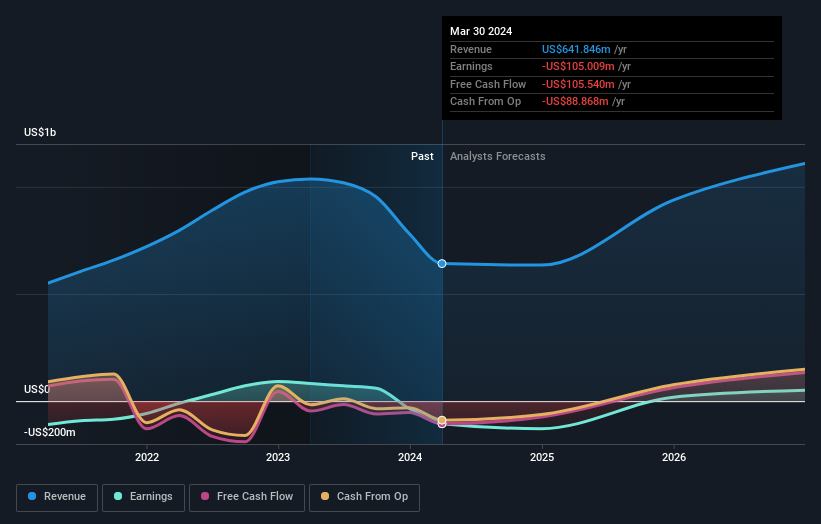

Silicon Laboratories wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one would hope for good top-line growth to make up for the lack of earnings.

In the last 5 years Silicon Laboratories saw its revenue grow at 5.9% per year. Put simply, that growth rate fails to impress. Like its revenue, its share price gained over the period. The increase of 6% per year probably reflects the modest revenue growth. If profitability is likely in the near term, then this might be one to add to your watchlist.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

Silicon Laboratories is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. If you are thinking of buying or selling Silicon Laboratories stock, you should check out this free report showing analyst consensus estimates for future profits.

A Different Perspective

Investors in Silicon Laboratories had a tough year, with a total loss of 11%, against a market gain of about 28%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Longer term investors wouldn't be so upset, since they would have made 6%, each year, over five years. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. If you would like to research Silicon Laboratories in more detail then you might want to take a look at whether insiders have been buying or selling shares in the company.

We will like Silicon Laboratories better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.