Yahoo Finance

Yahoo Finance Royal Bank of Canada (TSE:RY) Is Increasing Its Dividend To CA$1.42

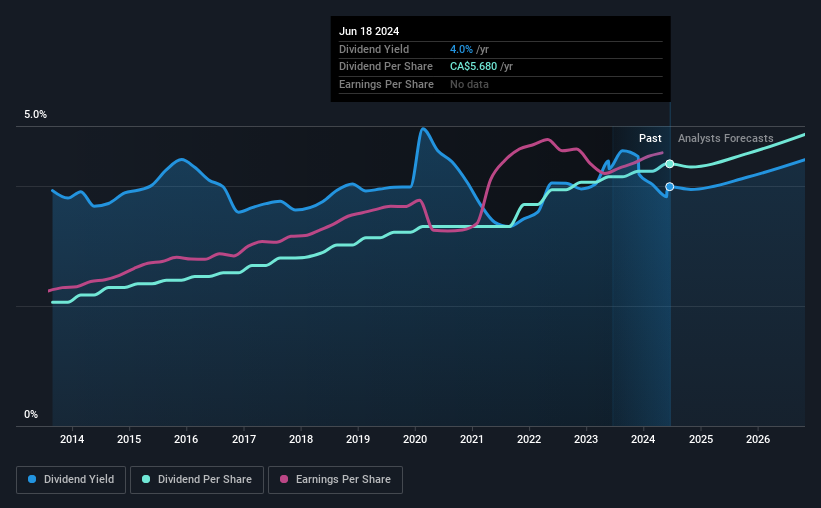

The board of Royal Bank of Canada (TSE:RY) has announced that it will be paying its dividend of CA$1.42 on the 23rd of August, an increased payment from last year's comparable dividend. This takes the annual payment to 4.0% of the current stock price, which is about average for the industry.

Check out our latest analysis for Royal Bank of Canada

Royal Bank of Canada's Dividend Forecasted To Be Well Covered By Earnings

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible.

Having distributed dividends for at least 10 years, Royal Bank of Canada has a long history of paying out a part of its earnings to shareholders. Based on Royal Bank of Canada's last earnings report, the payout ratio is at a decent 50%, meaning that the company is able to pay out its dividend with a bit of room to spare.

Over the next 3 years, EPS is forecast to expand by 3.1%. The future payout ratio could be 48% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

Royal Bank of Canada Has A Solid Track Record

The company has an extended history of paying stable dividends. The dividend has gone from an annual total of CA$2.68 in 2014 to the most recent total annual payment of CA$5.68. This works out to be a compound annual growth rate (CAGR) of approximately 7.8% a year over that time. The growth of the dividend has been pretty reliable, so we think this can offer investors some nice additional income in their portfolio.

The Dividend's Growth Prospects Are Limited

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Earnings per share has been crawling upwards at 4.6% per year. Royal Bank of Canada is struggling to find viable investments, so it is returning more to shareholders. This could mean the dividend doesn't have the growth potential we look for going into the future.

We Really Like Royal Bank of Canada's Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Companies that are growing earnings tend to be the best dividend stocks over the long term. See what the 11 analysts we track are forecasting for Royal Bank of Canada for free with public analyst estimates for the company. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com