Yahoo Finance

Yahoo Finance Roku (NASDAQ:ROKU investor three-year losses grow to 88% as the stock sheds US$552m this past week

It's not possible to invest over long periods without making some bad investments. But you have a problem if you face massive losses more than once in a while. So spare a thought for the long term shareholders of Roku, Inc. (NASDAQ:ROKU); the share price is down a whopping 88% in the last three years. That'd be enough to cause even the strongest minds some disquiet. Shareholders have had an even rougher run lately, with the share price down 18% in the last 90 days. While a drop like that is definitely a body blow, money isn't as important as health and happiness.

With the stock having lost 6.8% in the past week, it's worth taking a look at business performance and seeing if there's any red flags.

View our latest analysis for Roku

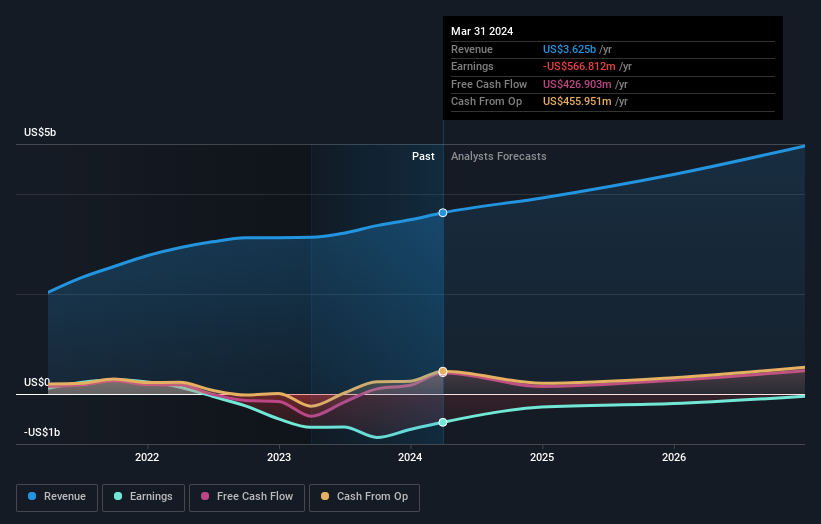

Because Roku made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. When a company doesn't make profits, we'd generally hope to see good revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

In the last three years, Roku saw its revenue grow by 15% per year, compound. That's a fairly respectable growth rate. So it seems unlikely the 23% share price drop (each year) is entirely about the revenue. It could be that the losses were much larger than expected. If you buy into companies that lose money then you always risk losing money yourself. Just don't lose the lesson.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. So it makes a lot of sense to check out what analysts think Roku will earn in the future (free profit forecasts).

A Different Perspective

Investors in Roku had a tough year, with a total loss of 19%, against a market gain of about 25%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 7% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Roku better, we need to consider many other factors. For instance, we've identified 2 warning signs for Roku that you should be aware of.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: most of them are flying under the radar).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com