Yahoo Finance

Yahoo Finance Retail Stocks to Buy for Long-Term Upside as the Tech Rally Slows

Technology stocks that have driven the market in 2023 face big tests this week as Microsoft, Meta, Amazon, and other titans all report their quarterly financial results. Tech stocks could come under near-term selling pressure no matter what happens because they already surged YTD even as earnings outlooks fade and the economy slows.

Tesla showed signs of weakness last week, which has sent one of the early 2023 winners tumbling. Still, the market remains almost eerily calm heading into a huge stretch of earnings reports that includes nearly all of the largest companies in the market—Apple is due out on May 4.

The Nasdaq and the S&P 500 have both moved roughly sideways over the last few months, while remaining solidly above their 50-day and 200-day moving averages. And perhaps the market makes it through this week without seeing too much movement.

But one would think that Wall Street should start to show more conviction in either direction in the early part of next month, with the Fed meeting on May 2-3 and the April CPI report due out on May 10.

Given this backdrop, investors might want to wait and see how tech performs in the coming weeks before they start buying stocks that are already up 30%, 40%, and even 50% YTD. Investors might instead decide now is time to be more conservative and buy proven, large-cap stocks from more stable and defensive areas of the market.

The two stocks we dig into today—Costco (COST) and Target (TGT)—are retail powerhouses trading at potentially attractive long-term entry points.

Costco Wholesale (COST)

Costco competes against the likes of Walmart (WMT), while remaining highly differentiated from most of the retail industry outside of club card competitors such as BJ’s Wholesale (BJ). Costco charges shoppers annual membership fees between $60 to $120 (at the moment) just to shop at its huge warehouse retail locations or online. Once customers are inside a Costco, they can buy pantry staples, fresh fruit, meat, and much more in bulk quantities, as well as clothing, patio furniture, TVs, diamond engagement rings, and nearly anything else you might imagine.

Costco’s membership fees help it maintain an extremely loyal customer base, while enabling it to keep costs low and margins high. Its U.S. and Canada renewal rate hit all-time highs of 93% last quarter. COST closed Q2 FY23 with 68 million paid households and 123 million cardholders, up 7% YoY, with its executive members accounting for 45% of paid members and 73% of worldwide sales.

Image Source: Zacks Investment Research

Costco could raise its annual fees sooner than later. COST has historically lifted its membership pricing every five to six years, with its last increase roughly six years ago in June 2017. Raising fees will help Costco better navigate inflation and boost its bottom line. Costco remains on very sturdy footing even if it doesn’t raise fees anytime soon. COST on April 19 raised its quarterly dividend by 13% to $1.02 a share. This came after it topped our Q2 FY23 earnings estimate in early March.

Costco posted 16% revenue growth in FY22 and 18% in FY21, which came on top of roughly 7.5% average sales growth in the five years prior. Costco also posted rather impressive bottom-line growth during this stretch. Zacks estimates calls for 7% revenue growth in FY23 and another 6% in FY24 to boost its earnings by 10% and 8%, respectively. Costco’s earnings revisions have held up rather well even as the wider S&P 500 outlook slips to help it land a Zacks Rank #3 (Hold).

Image Source: Zacks Investment Research

Costco shares have surged 370% in the past 10 years to blow away the market’s 160%, Walmart’s 95%, and the Zacks Retail sector’s 110%. COST has climbed 65% in the last three years to top the benchmark. But investors can scoop up Costco 15% below its peaks and 10% under its average Zacks price target.

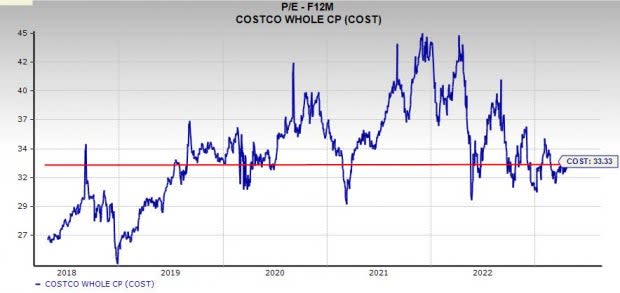

The nearby chart shows that COST recently climbed back above both its 50-day and 200-day moving averages. Costco also trades 25% below its highs and slightly under its five-year median at 33.3X forward earnings.

Target (TGT)

Target epitomized the boom-and-bust nature of the covid economy and stock market. The retailer was an early pandemic and post-covid rebound superstar. Target, like many others, then failed to adapt to changing consumer shopping patterns. Target shares got battered in 2022 on the back of inventory issues, slowing sales, rising costs, and more.

TGT simply had too much of the wrong stuff once consumers stopped splurging on furniture, appliances, TVs, and other big-ticket items. Target spent the past year working through its inventory issues, while investing in the future. TGT still managed to post 3% revenue growth in 2022, which came on top of 13% in 2021 and 20% and 2020.

Image Source: Zacks Investment Research

The inflationary crunch on shoppers hit Target harder than rival Walmart because TGT’s business is made up more heavily of discretionary items. Still, Zacks estimates call for Target to post roughly 2% sales growth in both FY23 and FY24. Its adjusted earnings outlook has slipped since its fourth quarter release but it has held up more recently to help it capture a Zacks Rank #3 (Hold).

Plus, TGT’s adjusted earnings are projected to surge 40% in FY23 and another 25% in FY24 to hit $10.55 per share (vs. $13.56 a share in 2021). Target’s most recent Zacks estimates are coming in above consensus. And Target remains a retail power built for the e-commerce and have-it-your-way consumer.

Image Source: Zacks Investment Research

Target stock has surged 130% in the past five years vs. the Zacks Retail sector’s 20% climb and the S&P 500’s 60%. Despite the outperformance, TGT trades roughly 40% below its 2021 peaks and 12% under its average Zacks price target. TGT has chopped around for nearly a year following its huge May 2022 selloff.

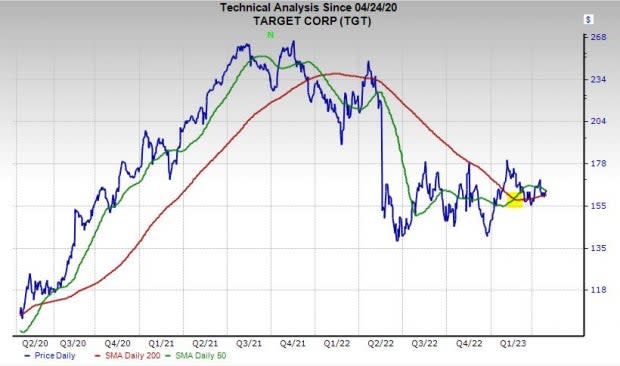

On the valuation front, Target trades just above its five-year median at 19.3X forward earnings, which also marks a 20% discount to the Zacks retail sector and 23% value vs. Walmart. Target is also on the cusp of breaking above its 50-day moving average again.

Target is a dividend aristocrat that's raised its payout for over 50 years running. In the end, long-term investors should try to remember that some of the best times to buy proven companies is when seemingly few others do.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

BJ's Wholesale Club Holdings, Inc. (BJ) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report