Yahoo Finance

Yahoo Finance Recession worries recede

[Note: A version of this article was previously published on TKer.co]

Stocks made new record highs, with the S&P 500 reaching a closing high of 5,026.61 and an intraday high of 5,030.06 on Friday. For the week, the S&P gained 1.4%. The index is now up 5.4% year to date and up 40.5% from its October 12, 2022 closing low of 3,577.03.

Coming into 2024, Deutsche Bank and Societe Generale were among a handful of banks whose economists were calling for a recession in 2024.

Last week, they both pulled that call.

"When we first adopted a mild recession as our baseline forecast, a key element was that, with an economy far from the Fed's objectives, the history of central bank-induced disinflations showed the path to a soft landing was narrow if not unprecedented. We now think the economy will land on this narrow path and that a recession will be averted with limited cost in the labor market." - Deutsche Bank’s Matthew Luzzetti, Feb. 5"We no longer anticipate the mild recession for 2024 that we had expected for nearly a year. Gains in jobs and consumer spending may be moderating, but they are not signaling problems ahead." - Societe Generale’s Stephen Gallagher, Feb. 7

The banks’ revised views follow a slew of better-than-expected economic reports released since the beginning of the year. (Read more about them in TKer’s weekly review of macro crosscurrents here, here, here, here, and below.)

While the data in aggregate continues to confirm the economy is in pretty good shape, some of the data show it isn’t quite as hot as it used to be.

Debt delinquencies rise

One set of metrics that has been deteriorating over the past couple quarters is debt delinquency rates. (More on this here, here, here, here, here, and here.)

According to the New York Fed’s Q4 Household Debt and Credit (HHDC) report, the share of debt newly transitioning into delinquency continued to rise for most forms of borrowing.

"Annualized, approximately 8.5% of credit card balances and 7.7% of auto loan balances transitioned into delinquency," the New York Fed observed. "Early delinquency transition rates for mortgages increased by 0.2 percentage point yet remain low by historic standards."

When you consider all outstanding debt, the delinquency rates, while rising, continue to reflect a normalization back to prepandemic levels.

In other words, while the "flow" into new delinquency has been picking up, the "stock" of delinquencies remains below prepandemic levels.

"As of December, 3.1% of outstanding debt was in some stage of delinquency, up by 0.1 percentage point from the third quarter," New York Fed researchers wrote. "Still, overall delinquency rates remain 1.6 percentage points lower than the fourth quarter of 2019."

So while debt delinquency rates have deteriorated, absolute levels of debt delinquencies aren’t too bad.

"It's maybe not a flashing red signal but something that is indicative of a slight weakening in household balance sheets that is consistent with a slowdown in consumption," New York Fed researchers said on a call with reporters.

It’s also worth keeping in mind that cooler economic activity has been an aim of the Federal Reserve in its ongoing effort to bring down inflation. (More here and here.)

About ‘record high’ credit card debt

There continues to be a lot of attention on credit card balances. Here are some headlines from the past week reporting on the New York Fed’s data:

Americans' credit card debt hits record $1.13 trillion - ABC News

Americans owe a record $1.1 trillion in credit card debt, straining budgets - CBS News

Credit card debt hits a ‘staggering’ $1.13 trillion. - CNBC

Credit card debt smashed another record high at the end of 2023 - Fox Business

Credit card debt passes $1 trillion. Here’s a payoff playbook. - Washington Post

While these headlines are accurate and it is true that delinquency rates have been ticking up, there is much-needed context.

"All of these debts are nominal figures," New York Fed researchers explained. "As price changes, naturally most of our debt figures are going to tend to be all time high. … If we were to report these as a percent of personal income or adjusted for CPI, I don't think that you would see these kinds of all time highs."

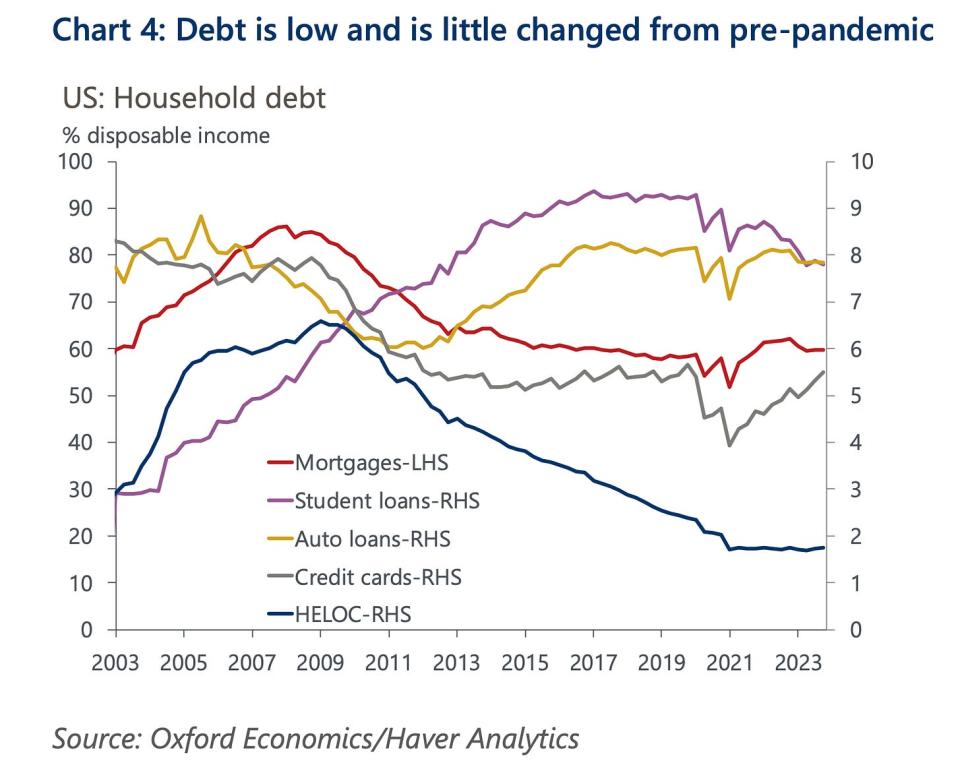

Indeed, as the chart below from Oxford Economics shows, credit card debt as a percent of disposable income (gray) is not abnormally high.

"Every category of consumer loan is now smaller relative to disposable incomes than before the pandemic," Oxford Economics’ Michael Pearce wrote on Thursday. "That is true even for credit card debt that, despite rising at a solid pace in recent years, remains below its Q4 2019 level as a share of incomes."

More timely data from Bank of America confirm that credit card activity also does not reflect a financially stretched consumer.

"Two metrics to measure consumers’ ability to borrow for everyday spending are the share of current spending they are financing on credit as opposed to debit cards and the degree to which they are spending close to their credit limits," Bank of America analysts wrote on Thursday. "On the first of these, Bank of America internal data suggests that the share of spending on credit cards, while rising since 2020, is no higher than it was in 2019. On the second, the average credit card utilization rate (credit card balances relative to credit limits) remains below 2019 levels.

The big picture

Metrics like debt delinquencies suggest things are relatively worse than they were during the hottest periods of the current economic expansion. It’s a normalization that’s to be expected in the Fed’s efforts to bring down inflation.

But the absolute levels of most metrics suggest the economy continue to be generally good — further confirming we are experiencing a bullish "Goldilocks" soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

Reviewing the macro crosscurrents

There were a few notable data points and macroeconomic developments from last week to consider:

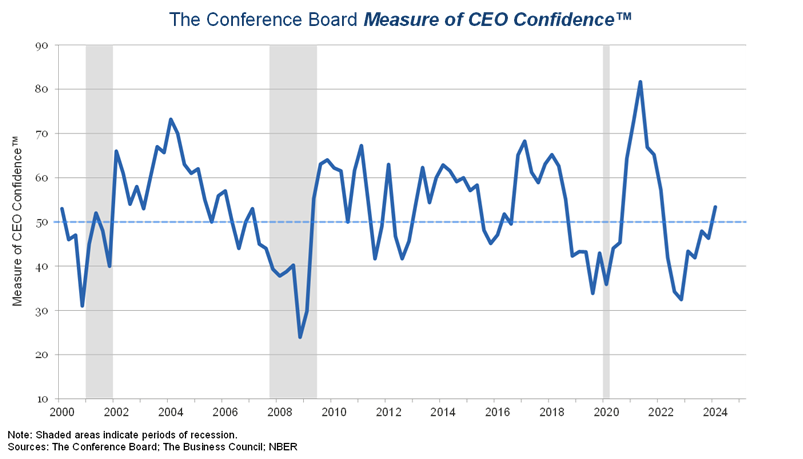

CEO’s are optimistic. The Conference Board’s CEO Confidence index in Q1 2024 signaled optimism for the first time since Q1 2022. CEOs’ assessment of current and future conditions both improved for general economic conditions and conditions in their own industries.

For more on improving sentiment, read: The economic vibes are healing

Services surveys look up. From S&P Global’s January U.S. Services PMI: "The U.S. service sector started the year in a sweet spot, with output and demand growth accelerating while price pressures cooled markedly. The key driver of faster growth was the financial services sector, where looser financial conditions tied to expectations of lower interest rates spurred greater activity in January. Households are also benefitting from loosened financial conditions, driving renewed growth in consumer-facing services. The buoyancy of the service sector has outweighed a further lackluster performance in manufacturing, and is driving overall output higher at a rate broadly consistent with GDP rising at a 2% pace…"

The ISM’s Services PMI rose in January, signaling accelerating growth, driven by gains in business activity, new orders, and employment.

However, the ISM’s prices index jumped significantly, stoking concerns that inflation could be heating up.

It’s worth remembering that soft data like the PMI surveys don’t necessarily reflect what’s actually going on in the economy.

For more on this, read: What businesses do > what businesses say

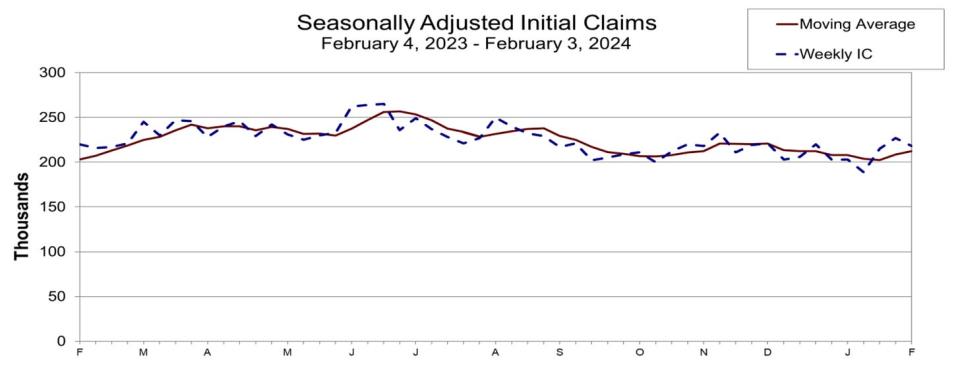

Unemployment claims fall. Initial claims for unemployment benefits fell to 218,000 during the week ending February 4, down from 224,000 the week prior. While this is above the September 2022 low of 182,000, it continues to trend at levels historically associated with economic growth.

For more on the labor market, read: The hot but cooling labor market in 16 charts

Is the labor market heating up again? January data from LinkUp suggest the demand for labor may be picking up again. From LinkUp: "Job listings jumped up across the board in January, with a 2.6% increase in active listings and a 14% bump in created listings over last month. This bump corresponds with the whopper BLS report of 353,000 new jobs in January. Higher demand touches most of the economy, as listings are up in 75% of U.S. states, across 87% of industries, and for 90% of occupations."

For more on job openings, read: Were there really twice as many job openings as unemployed people?

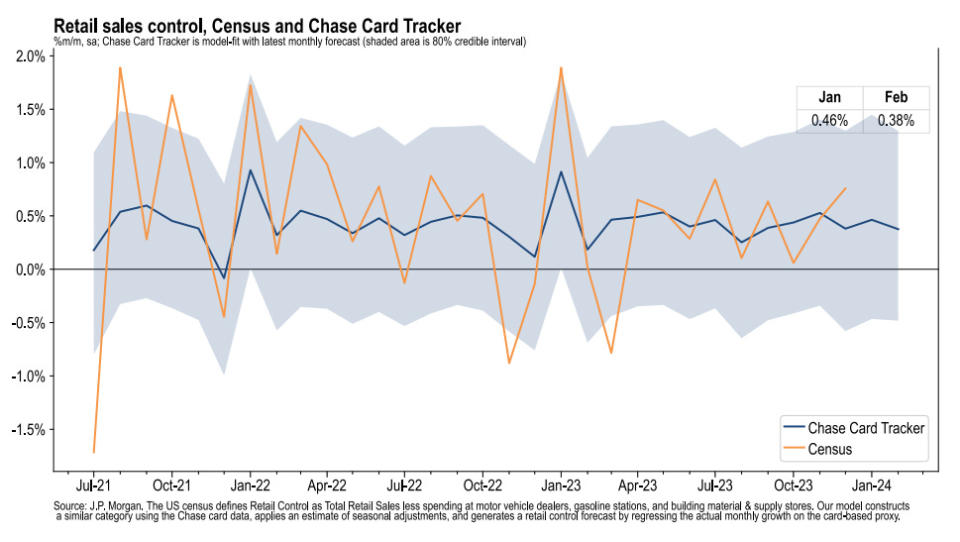

Card spending data is mixed. From JPMorgan Chase: "As of 01 Feb 2024, our Chase Consumer Card spending data (unadjusted) was 2.1% above the same day last year. Based on the Chase Consumer Card data through 01 Feb 2024, our estimate of the US Census January control measure of retail sales m/m is 0.46%."

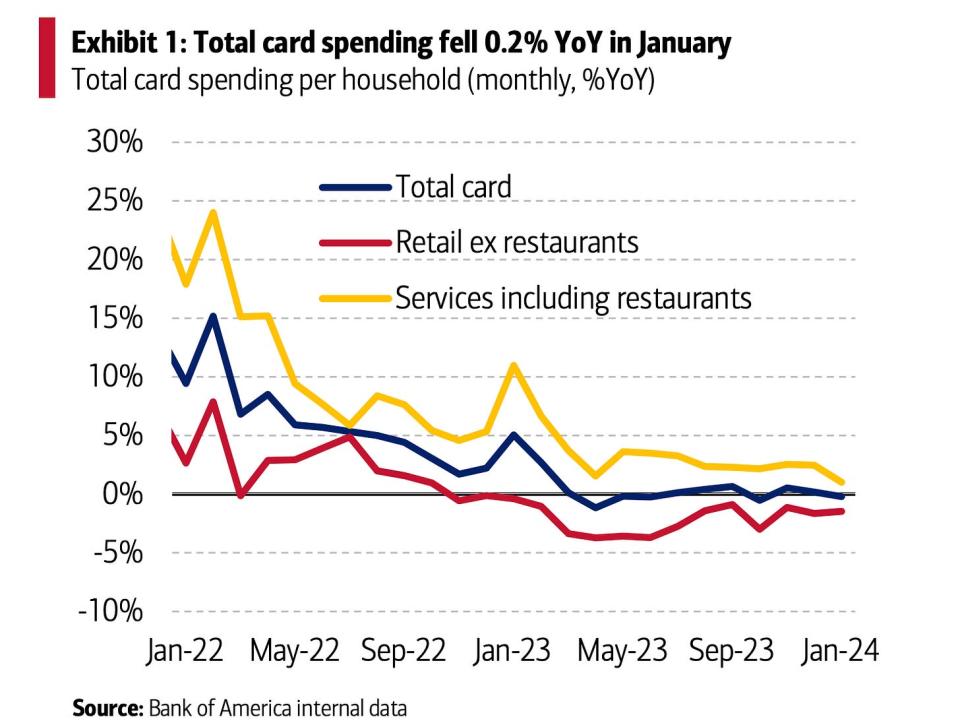

From BofA: "Consumer spending softened in January with total card spending per household falling by 0.2% year-over-year (YoY), after a 0.2% YoY rise in December, according to Bank of America internal data. On a seasonally adjusted (SA) basis, per household spending dropped 0.3%."

For more on consumer finances, read: People have money

Supply chain pressures less loose. The New York Fed’s Global Supply Chain Pressure Index — a composite of various supply chain indicators — ticked higher in January but remains below levels seen even before the pandemic. That's way down from its December 2021 supply chain crisis high.

For more on the supply chain, read: We can stop calling it a supply chain crisis

Used car prices are cooling. From Manheim: "Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) were unchanged in January compared to December. The Manheim Used Vehicle Value Index (MUVVI) remained at 204.0 but down 9.2% from a year ago. The index experienced the same 0.0% monthly change from December 2021 to January 2022."

Gas prices stay cool. From AAA: "Sticking to the slow lane since last week, the national average for a gallon of gas dipped slightly for a few days before rising a fraction of a cent higher to $3.15. However, seasonal demand trends, higher costs for oil, and routine refinery maintenance will likely push pump prices slowly higher soon."

For more on energy prices, read: The other side of the oil price story

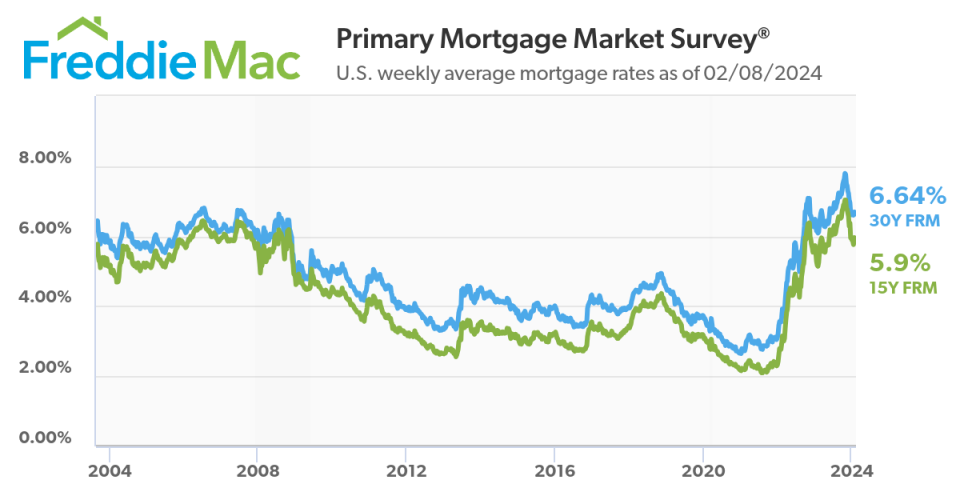

Mortgage rates tick up. According to Freddie Mac, the average 30-year fixed-rate mortgage declined to 6.64% from 6.63% the week prior. From Freddie Mac: "Mortgage rates remain stagnant, hovering in the mid-six percent range over the past several weeks. The economy and labor market remain strong with wage growth outpacing inflation, which is keeping consumer spending robust. Meanwhile, affordability in the housing market is an ongoing issue due to continued high home prices, elevated mortgage rates and low supply of homes on the market, particularly for first-time and low-income homebuyers."

For more on mortgages and home prices, read: Why home prices and rents are creating all sorts of confusion about inflation

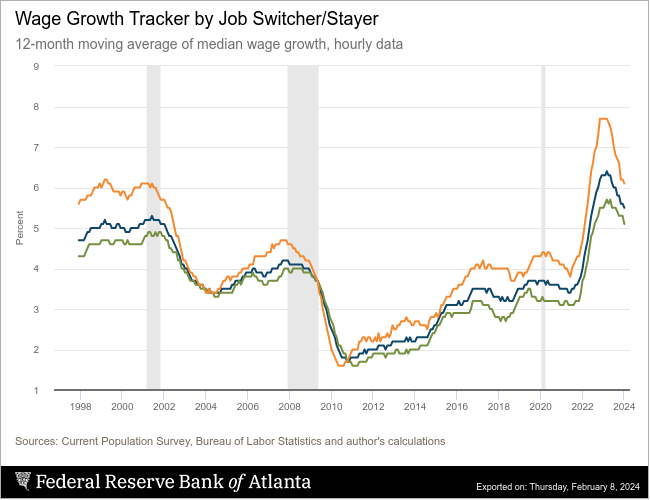

Job switchers lose pay advantage. According to the Atlanta Fed’s wage growth tracker, the gap wage growth between those who switch jobs and those who stay at their jobs continues to close. Job switchers saw 6.1% wage growth in the 12 months ending in December, whereas job stayers saw 5.1% growth during the period.

For more on why the Fed is concerned about high wage growth, read: The complicated mess of the markets and economy, explained

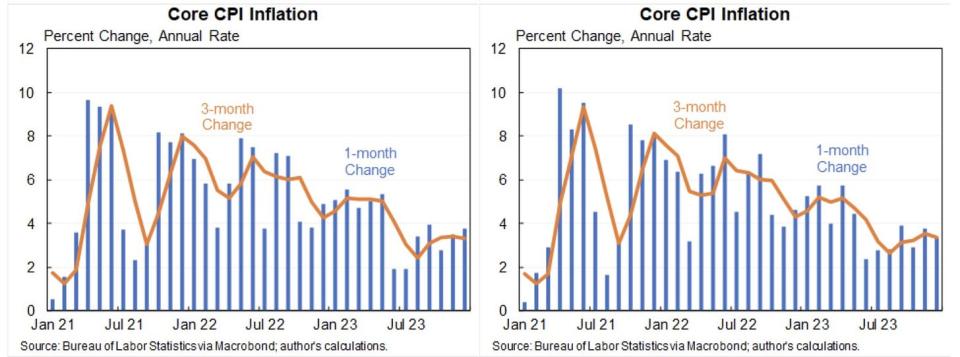

Insignificant revisions to inflation data. Every year, the BLS adjusts consumer price index (CPI) data to address seasonal factors. Long story short, this year’s revisions were insignificant, and the annualized three-month, six-month, and 12-month changes in core CPI were unchanged.

For more on inflation, read: Inflation: Is the worst behind us?

People are sorta returning to the office. From Kastle Systems: "For the second week in a row, office occupancy reached a record high since the start of the pandemic. Office occupancy rose more than a full point to 53% last week, according to Kastle’s 10-city Back to Work Barometer. Multiple cities reached post-pandemic record highs as well, including Washington, D.C. at 50.8%, Chicago at 56.4%, Philadelphia at 43.4%, and Dallas at 59.4%."

For more on office occupancy, read: This stat about offices reminds us things are far from normal

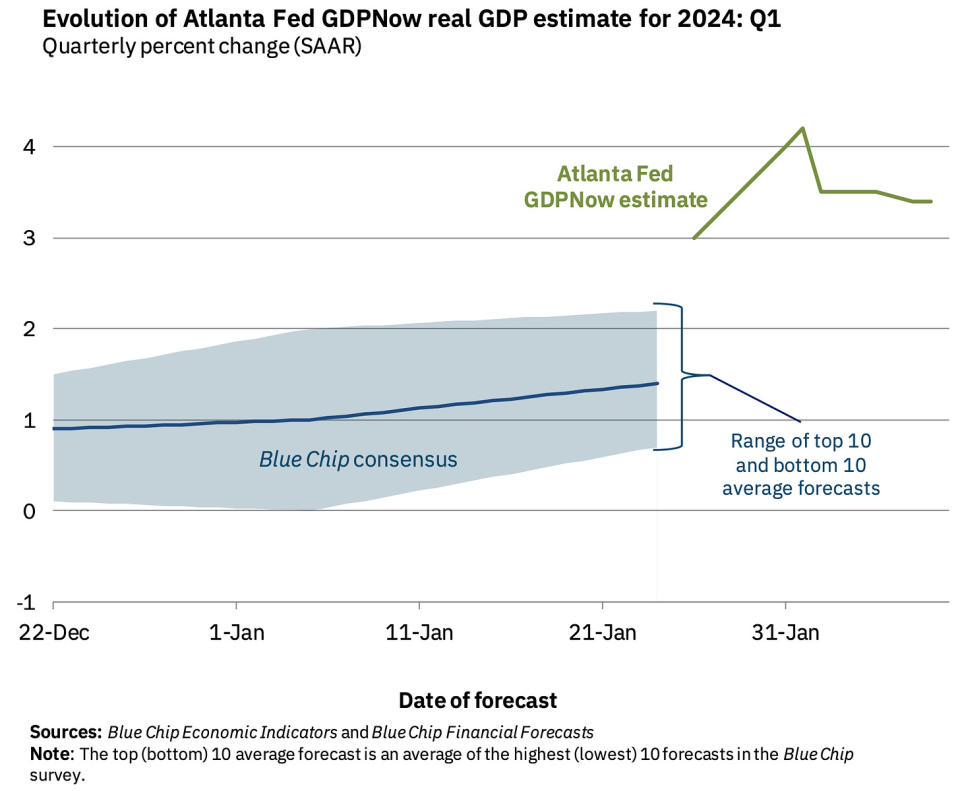

Near-term GDP growth estimates look good. The Atlanta Fed’s GDPNow model sees real GDP growth climbing at a 3.4% rate in Q1.

For more on economic growth, read: Economic growth: Slowdown, recession, or something else?

Putting it all together

We continue to get evidence that we are experiencing a bullish "Goldilocks" soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

This comes as the Federal Reserve continues to employ very tight monetary policy in its ongoing effort to get inflation under control. While it’s true that the Fed has taken a less hawkish tone in 2023 and 2024 than in 2022, and that most economists agree that the final interest rate hike of the cycle has either already happened, inflation still has to stay cool for a little while before the central bank is comfortable with price stability.

So we should expect the central bank to keep monetary policy tight, which means we should be prepared for relatively tight financial conditions (e.g., higher interest rates, tighter lending standards, and lower stock valuations) to linger. All this means monetary policy will be unfriendly to markets for the time being, and the risk the economy slips into a recession will be relatively elevated.

At the same time, we also know that stocks are discounting mechanisms — meaning that prices will have bottomed before the Fed signals a major dovish turn in monetary policy.

Also, it’s important to remember that while recession risks may be elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs, and those with jobs are getting raises.

Similarly, business finances are healthy as many corporations locked in low interest rates on their debt in recent years. Even as the threat of higher debt servicing costs looms, elevated profit margins give corporations room to absorb higher costs.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

And as always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a pretty rough couple of years, the long-run outlook for stocks remains positive.

[Note: A version of this article was previously published on TKer.co]