Yahoo Finance

Yahoo Finance Posthaste: Why the Bank of Canada pause won't save the housing market this time

Good morning,

Canada’s housing correction is back.

Home sales fell 4.1 per cent in August, we learned late last week — the second monthly decline in a row and the fastest drop since the Bank of Canada started raising interest rates in 2022, says Desjardins.

This spring when the central bank first paused rate increases the housing market sprang back to life with a vigour that surprised economists.

Two more rate hikes in June and July put a damper on that rally, but this month the Bank paused again. Can we expect to see another bounce in the housing market?

Don’t count on it, says BMO senior economist Robert Kavcic, because this time “the headwinds are stiffer than they were the last time the Bank of Canada stepped aside.”

“The Bank of Canada’s September 6th pause will help market psychology, and we wouldn’t fully write off this market given underlying demographic demand, but there are a few reasons why this pause might not provide the same burst it did in the spring,” he wrote in note.

For one thing, sellers are coming back to the market, something that was missing in the spring.

In March new listings were the lowest since 2003, because “homeowners didn’t want to, or have to, sell into a down market,” said Kavcic.

Now new listings are surging back to historic norms, up 5.5 per cent in August from last year, and there’s a record number of homes under construction that will make their way onto the market, he said.

Pressure to sell will also mount as more mortgages come up for renewal. In its financial system review earlier this year, the Bank of Canada highlighted concerns about the ability of households to service their debt when mortgages are renewed at much higher rates, with some facing payment increases of up to 40 per cent.

And this time there is no mortgage rate relief on the horizon, said Kavcic.

In the spring, the market expected a recession and was pricing in rate cuts in the second half of 2023. As bond yields dropped, shorter-term fixed-mortgage rates fell below 5 per cent.

Now yields are high and the Bank’s hawkish hold in September is keeping the market from rallying, leaving the lowest available mortgage rate today about 100 basis points higher than the lowest in the spring, he said.

Then there is the economy.

The job market has weakened in recent months with the unemployment rate up 0.6 percentage points from last year’s lows and job vacancies down 230,000 from a year ago.

“This is not yet a ‘soft’ job market by any means, and wage growth is still sturdy, but there might be a little fraying around the edges,” said Kavcic.

Oxford Economics believes the housing correction will extend into 2024 as the economy falls into recession.

“Mounting job losses and increased income insecurity will combine with higher mortgage rates to weaken demand for housing and likely lead to a greater number of stressed home sales,” said Oxford economist Tony Stillo.

The average home price (seasonally adjusted) fell 2.3 per cent in August from the month before, and has now fallen 5.2 per cent over the past three months, erasing much of the spring rebound, he said.

Oxford expects home prices will fall another 5 to 10 per cent by the middle of next year, taking the overall decline from the market’s 2022 peak to between 20 and 25 per cent.

RBC economists also expect cooling to last through the fall as higher interest rates, affordability challenges and a “looming recession” throw up obstacles.

“Any material acceleration in the recovery will have to wait until interest rates come down in 2024,” said RBC assistant chief economist Robert Hogue.

__________________________________________________

Was this newsletter forwarded to you? Sign up here to get it delivered to your inbox.

_____________________________________________________________________

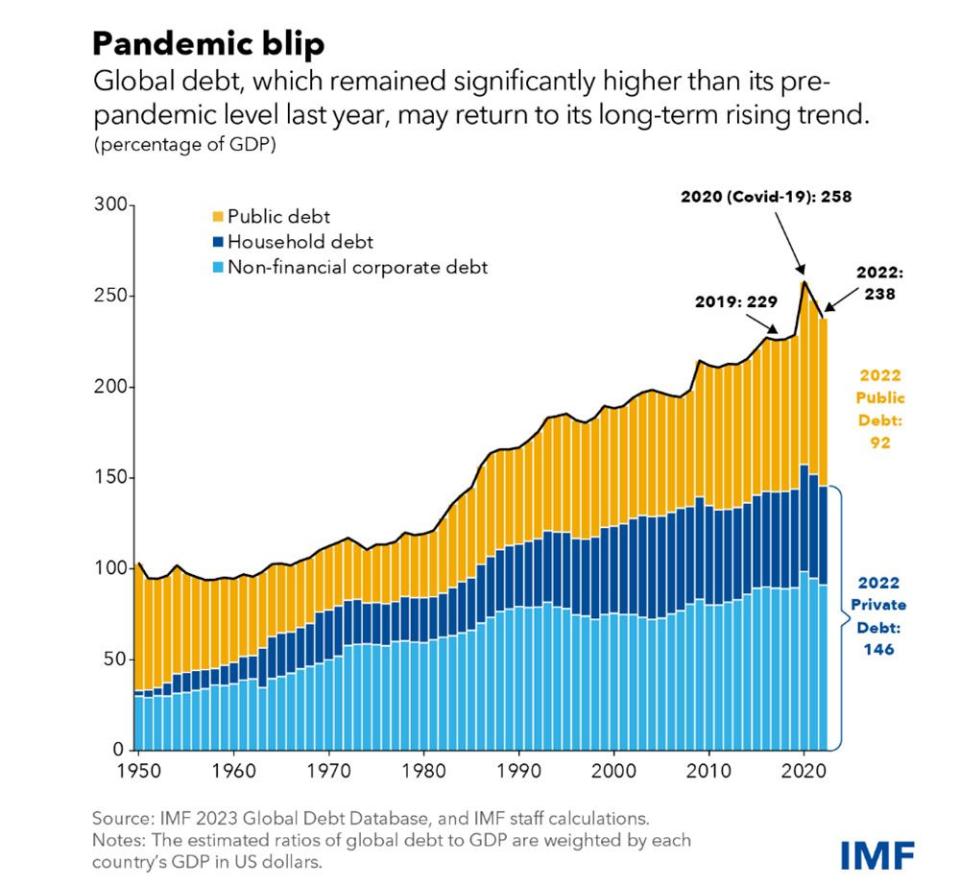

Global debt fell back from its pandemic peak for the second year in a row, but the rising trend remains, warns the International Monetary Fund.

Total debt was 238 per cent of global gross domestic product in 2022, according to the IMF’s latest Global Debt Monitor, nine percentage points higher than before the pandemic in 2019. In U.S. dollars the debt amounts to $235 trillion, or $200 billion above its level in 2021.

Public debt, especially, remains “stubbornly high,” said the IMF, dropping by just 8 percentage points of GDP over the past two years, erasing only about half of the pandemic spike.

Big week for central banks. Wednesday is the main event when the United States Federal Reserve delivers its decision. On Thursday, the United Kingdom, Scandinavia and Switzerland weigh in, and on Friday it’s the Bank of Japan.

World Petroleum Congress begins in Calgary and runs until Sept. 21

Natural Resources Minister Jonathan Wilkinson will announce clean energy investments today in Calgary

Get all today’s top breaking stories as they happen with the Financial Post’s live news blog, highlighting the business headlines you need to know at a glance.

_______________________________________________________

Power trip: Energy transition opens investing opportunities in small-to-mid-sized Canadian companies

Employers and staff are calling a ‘truce’ on the return-to-office war

One reason your will needs to be regularly updated is that your life changes, as does the life of the person who agreed to be your estate’s executor. Lawyer Ed Olkovich walks us through what happens if the named executor dies or is otherwise unable to perform their duties and how the courts decide what to do next. Find out more

____________________________________________________

Today’s Posthaste was written by Pamela Heaven, @pamheaven, with additional reporting from The Canadian Press, Thomson Reuters and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com, or hit reply to send us a note.