Yahoo Finance

Yahoo Finance Posthaste: Pain of Canadians' mortgage payment shock is not over — not by a long shot

There’s been a lot of hope in the air lately that the Bank of Canada is getting close to cutting interest rates.

When the central bank held rates at 5 per cent at its meeting earlier this month, governor Tiff Macklem said a June cut was “within the realm of possibilities,” and inflation data shortly after appeared to support that.

After all it has been a long, tough haul for indebted homeowners since the bank began hiking its benchmark rate early in 2022.

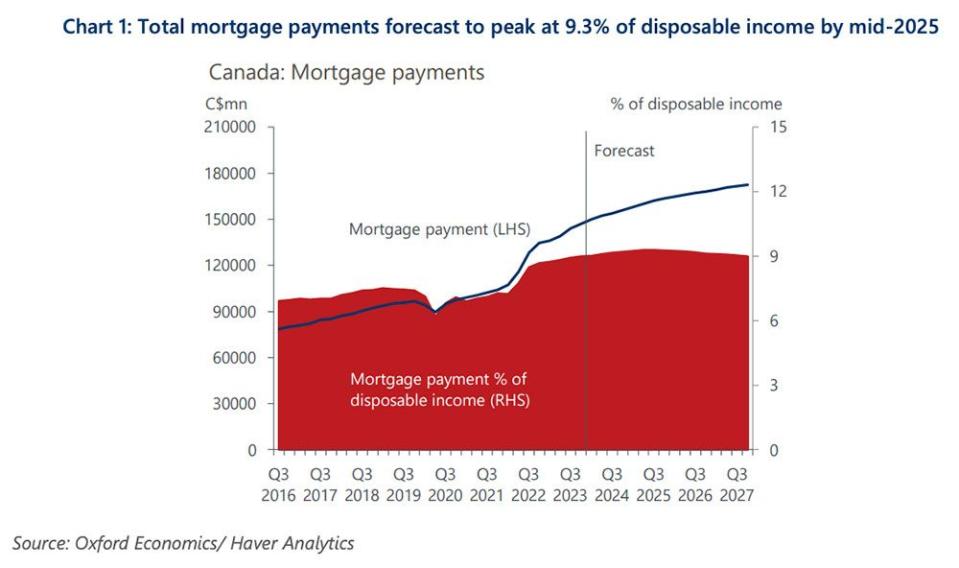

Five-year mortgage rates have surged from lows of 3.2 per cent in 2021 to 6.4 per cent in the fourth quarter of 2023, more than doubling mortgage payments, according to a new study by Oxford Economics.

“This has weighed on consumers’ pockets, but our calculations suggest that the mortgage payment shock is not over yet, said Oxford economists Callee Davis and Tony Stillo.

Even with interest rates expected to ease in the second half of this year, Oxford forecasts that mortgage payments will increase by another 6 per cent to $156 billion by the end of 2024. By the end of 2027, these payments will have risen 18 per cent to $173 billion.

These are big numbers and will take mortgage payment’s share of disposable income to a peak of 9.3 per cent by mid-2025 before it begins to ease, the highest on records going back to 1990, says Oxford.

The hardest hit will be low to medium-income households, which have little spare income, excess pandemic savings or ability to take on more debt.

According to Oxford, these households hold about 45 per cent of the mortgage debt in this country, with higher-income households accounting for 55 per cent.

Higher income households, with more disposable income, are obviously better equipped to deal with rising mortgage payments. For less wealthy Canadians, however, these payments are expected to gobble up 10 per cent of disposable income by mid-2025, compared to 8.8 per cent for higher incomes.

With little to no buffer, lower-income households could be forced to cut discretionary spending, become delinquent on their mortgages or sell their homes, said the economists.

And since these households accounted for 50 per cent of consumption in Canada last year, the pullback will hit the economy, they said.

Oxford’s outlier forecast is that aggregate real consumer spending will slow to 0.5 per cent this year, down from 1.7 per cent growth in 2023, bringing on a mild recession.

“Weaker consumption, which accounts for more than half of GDP, is a key driver of our recession forecast, but we could also see a period of deleveraging in coming years,” said Oxford.

Sign up here to get Posthaste delivered straight to your inbox.

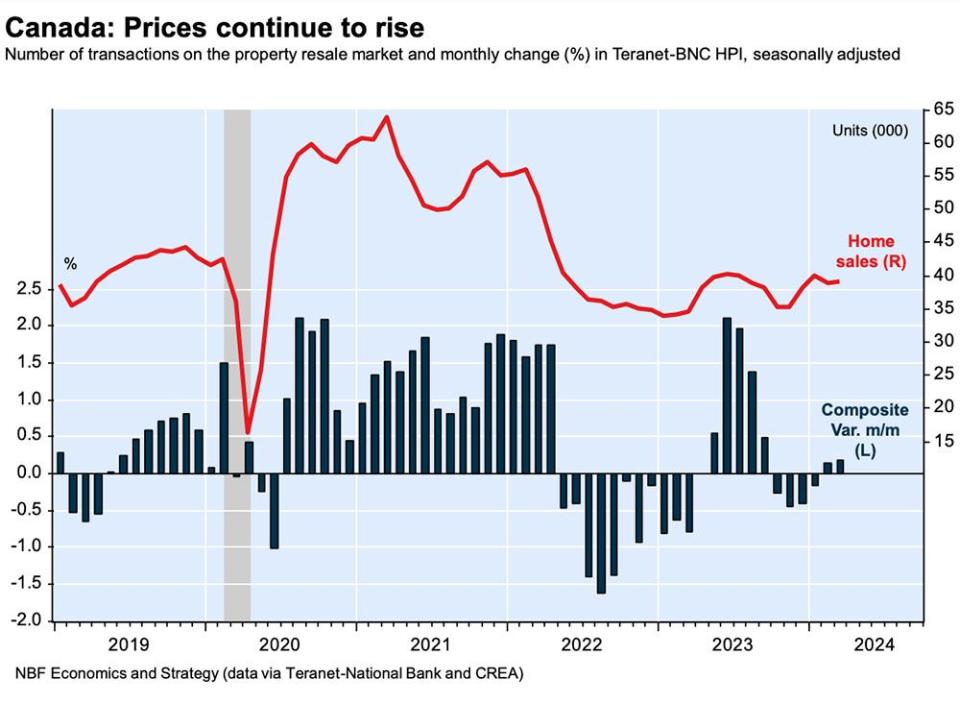

Home prices on the Teranet-National Bank Composite Index continued their march higher last month, gaining 0.2 per cent on February. The housing market has been on an upswing since November, according to the index, lifted by surging demographic growth, slightly better fixed mortgage rates and anticipation of Bank of Canada interest rate cuts, said National Bank of Canada economist Darren King.

National is “cautiously” optimistic that a significant recovery could be coming down the pipe that includes stronger price growth.

But there are plenty of uncertainties too, including “further deterioration in the labour market for young people,” said King.

Today’s Data: United States existing home sales, initial jobless claims

Earnings: Comerica Inc, Netflix Inc, Blackstone Inc, PPG Industries

Why big banks and pension giants are likely breathing easier after the Liberal budget

Lack of investment is a ‘big part’ of Canada’s productivity slowdown — and it could get worse

David Rosenberg: Time for Macklem to turn before it’s too late

April is generally a good month for investors, with the S&P/TSX composite index and the S&P 500 finishing up 74 per cent and 84 per cent of the time, respectively. But portfolio manager Martin Pelletier points out the last time there was such a concentration in the top 10 per cent of U.S. stocks was in 1929, and we all know what happened after that. Find out more at FP Investing

Are you worried about having enough for retirement? Do you need to adjust your portfolio? Are you wondering how to make ends meet? Drop us a line at aholloway@postmedia.com with your contact info and the general gist of your problem and we’ll try to find some experts to help you out while writing a Family Finance story about it (we’ll keep your name out of it, of course). If you have a simpler question, the crack team at FP Answers led by Julie Cazzin or one of our columnists can give it a shot.

McLister on Mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Read them here

Today’s Posthaste was written by Pamela Heaven with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.