Yahoo Finance

Yahoo Finance Posthaste: Owning a home 'huge, if not impossible' stretch for many households in these Canadian cities

Good morning,

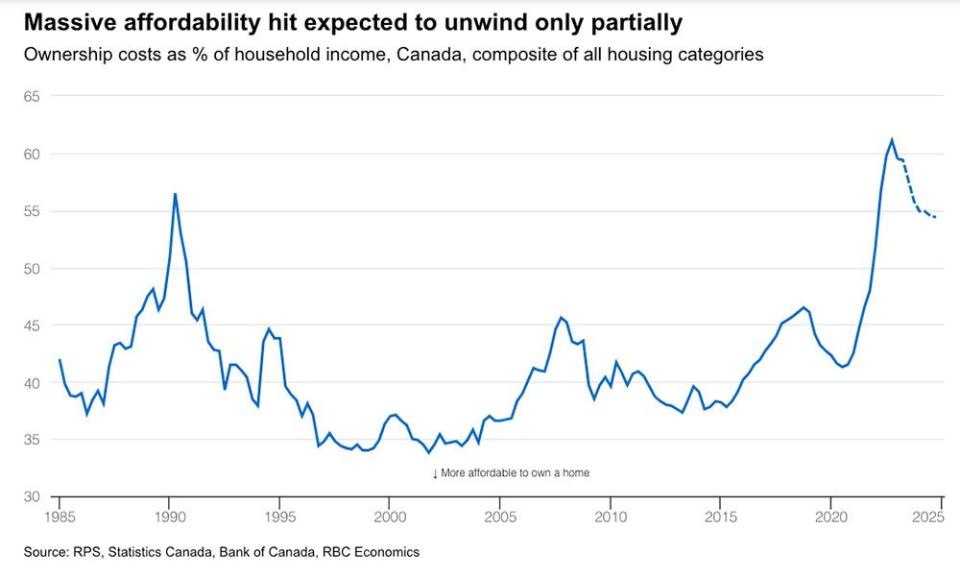

The good news is that owning a home in Canada became a little more affordable for the first time in almost three years.

RBC’s aggregate affordability measure, which tallies the share of median pre-tax income needed to cover home ownership costs, dropped nationally in the first quarter, down 1.6 percentage points to 59.5 per cent.

That means it takes about 60 per cent of a median income to cover the mortgage payments, taxes and utilities on a single-family home at the benchmark market price.

Last year affordability worsened as the Bank of Canada’s aggressive round of interest rate hikes kept the pressure on borrowers even as home prices dropped. The increase in mortgage rates added 4.3 percentage points to the measure (an increase is a decline in affordability) while falling home prices subtracted just 2.1 percentage points.

But when the Bank paused its hikes after its January meeting it gave homebuyers some “breathing room,” albeit temporarily, writes RBC assistant chief economist Robert Hogue in his report.

The policy shift stabilized mortgage rates and allowed the housing correction to lower ownership costs in the first quarter.

The bad news is challenges ahead could stall or even reverse these slight gains in affordability.

First the housing market has rebounded much faster than expected. RBC economists had thought it would take until the fall for prices to rise, but increased demand and low inventories have tightened conditions much faster than forecast.

In May, Toronto home prices rose for the third month in a row and the 3.2 per cent gain was the biggest since the market peaked in February 2022.

The Bank of Canada’s return to hiking also complicates matters. The Bank raised its rate to 4.75 per cent in June and is widely expected to increase it to 5 per cent this month. If the central bank stops there, as RBC believes, the rate increase should serve to dampen demand and home prices, keeping improvements in affordability on track, said Hogue.

But if the Bank continues to raise rates gains in affordability will become more challenging.

Meanwhile, many cities in Canada remains in “full-blown affordability crisis,” said Hogue.

“While welcome, the easing in ownership costs barely makes a dent in reversing the enormous loss of affordability since mid-2020,” he said.

“Big picture, owning a home is still a huge (if not impossible) stretch for middle-income households in Vancouver, Victoria and Toronto, and Montreal, Ottawa and Halifax to a lesser degree.”

In Vancouver, a middle-income household needs to devote a staggering 96.1 per cent of their pay to the costs of home ownership, even though affordability here improved by 2.7 percentage points in the first quarter.

“Owning a home has never been so unaffordable in Canada except in the previous quarter,” said Hogue.

In Toronto, a two percentage point decline in the measure shaved off less than a tenth of the increase over the past two years, and at 79 per cent the city is “still deep in crisis territory.”

RBC expects affordability to continue to improve but slowly. Based on its forecasts, it predicts the measure will fall 5 percentage points nationally over the coming year, a small fraction of the record 20-point increase since the middle of 2020.

__________________________________________________

Was this newsletter forwarded to you? Sign up here to get it delivered to your inbox.

_____________________________________________________________________

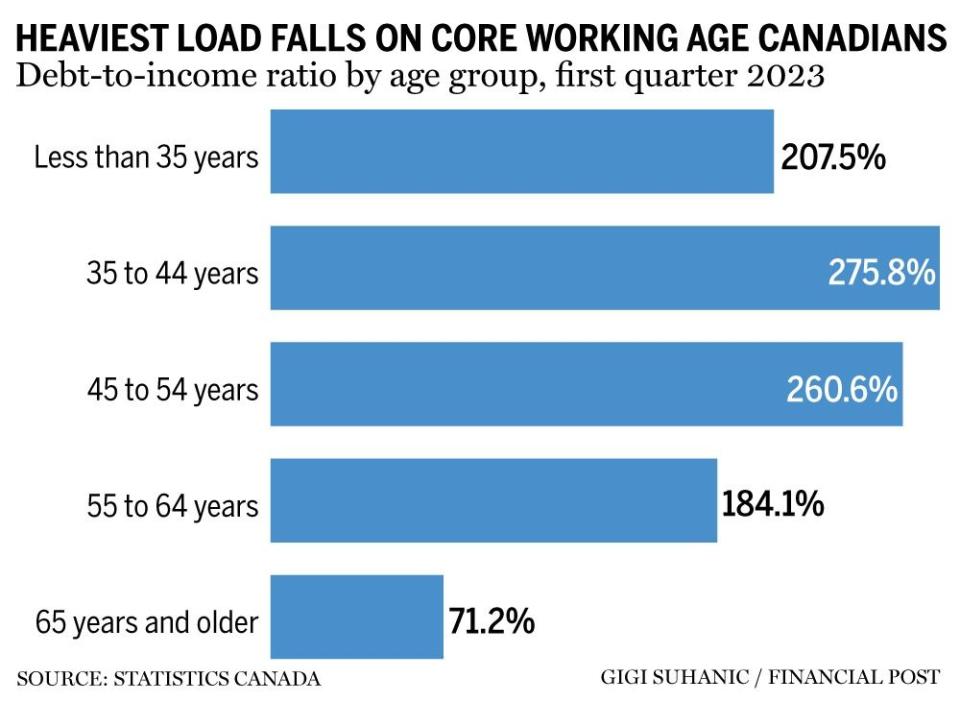

Some rather alarming news from Statistics Canada yesterday. Debt-to-income ratios for younger and working-age Canadians hit a record high in the first quarter.

Working-age households suffered unprecedented increases, reaching 275.8 per cent for households aged 35 to 44 years, up 16.6 percentage points from a year earlier, and 260.6 per cent for households aged 45 to 54 years, up 20.5 percentage points.

Only senior households (65 and older) had a debt-to income ratio lower than the start of the pandemic in the first quarter of 2020.

High interest rates and inflation are hitting the younger age groups harder because these households carry higher balances on credit cards and mortgages, said Statistics Canada.

“Persistently high interest rates and inflation are likely to continue to strain households’ ability to make ends meet without going further into debt, especially vulnerable groups, such as those with the lowest income, the least wealth and those of younger age groups.”

Federal Open Market Committee release minutes for June interest rate hold

Today’s Data: U.S. factory orders

_______________________________________________________

B.C. ports strike could inflict damage that takes months to correct, warns Canada’s biggest railway

Calgary real estate sets another sales record as tight conditions persist

Employers are racing to catch up as workers experiment with AI without knowing the risks

Researching a stock involves more than just looking at a company’s simple revenue and profit numbers, though even that can be difficult when there are adjusted earnings. Veteran investor Peter Hodson looks at that and four other figures that often cause misunderstandings. Read them here

Case for ending the Bank of Canada's interest rate hikes now

Calgary real estate sets another sales record as tight conditions persist

____________________________________________________

Today’s Posthaste was written by Pamela Heaven, @pamheaven, with additional reporting from The Canadian Press, Thomson Reuters and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com, or hit reply to send us a note.