Yahoo Finance

Yahoo Finance Political Shockwaves Topple Latin America’s Carry Trade Darlings

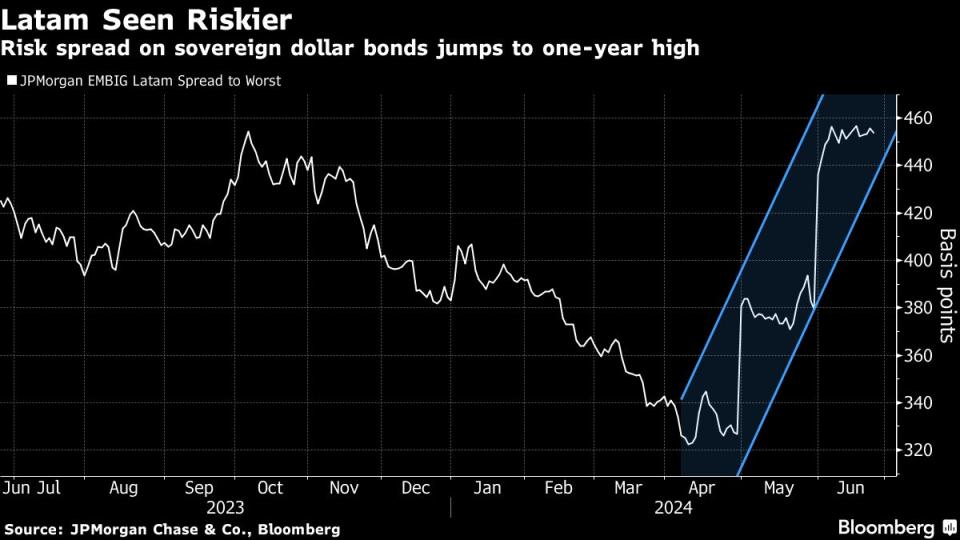

(Bloomberg) -- Latin America has flipped from emerging-market investors’ most-favored region to their least loved in just six weeks.

Most Read from Bloomberg

Biden's Defiance Has Democrats Fearing They'll Lose White House

Chinese Golf Carts Surging Into US Prompt Pleas for 100% Tariff

Volatility began to creep back into foreign exchange markets in mid-May, leading them to question favorites like the Mexican peso and Brazilian real. Now, those positions have all but fallen apart, with the region leading global losses.

The main issue is politics. Leaders have floated policy changes that investors worry will lead to overspending, scuppering the stability that drew many to the area. That’s added to underlying fears stemming from the US, where policymakers have delayed rate cuts, bolstering the appeal of the dollar.

As a result, the profitable carry trade — borrowing in the currency of a low-yielding country to buy a high yielder — has gone from minting double-digit returns to punishing players with steep losses.

“There’s no carry trade to exploit if the currency that you are long is too unstable,” said Thierry Wizman, director of global currencies and an interest-rate strategist at Macquarie Futures. “Carry traders were not presuming that there would be as much volatility as there would be.”

It’s a stark reversal for a region that had become a favored destination. In the two years before the trade fell apart, borrowing in Japanese yen, where rates were negative, and buying the peso and real resulted in returns of about 80% and 50%, respectively. That same strategy in the less liquid but high yielding Colombian peso was also lucrative, supplying a return of 63%, according to data compiled by Bloomberg.

It was largely made possible by a period of fiscal calm and low volatility. Now, though, several of those same countries are embarking on policy shifts that have riled markets — Mexico is considering changing the way judges are selected, Colombia is flouting its fiscal rule and Peru has been dogged by a reemergence of political turmoil, said Benito Berber, chief Latin America economist at Natixis.

Those risks are outweighing the appeal of the carry trade, even as policymakers in those countries leave interest rates high and the outlook on the Fed’s next moves starts to become clearer, he said.

“Risks in Latin America have some staying power for the next 6 months,” Berber said.

Super Peso

No country exemplifies the rapid shift more than Mexico. There, a landslide victory by Claudia Sheinbaum in the June 2 presidential election stoked concern her Morena Party allies will use their majority in congress to push through measures that undermine checks on power.

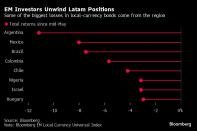

The Mexican peso suffered an 8% drop in the two weeks that followed, a historic rout for a currency whose unrelenting rally had earned it the moniker, “super peso.” Hedge funds slashed their bets on the peso in one of the biggest retreats on record, cutting their net long position in the third-biggest reduction since the Commodity Futures Trading Commission began compiling records in 2006. Meanwhile, local government bonds lost 1.6%, the worst performance in emerging markets, according to data compiled by Bloomberg.

“Mexico, being a success story of the post-pandemic world, had room for vulnerability and it came in the form of an undesirable political result,” said Juan Perez, director of trading at Monex USA. It “puts in peril the idea of checks and balances. The proposals for judicial reform are items that make it seem like there’s more in danger than just economic normalcy and trade assurance.”

That same trade involving the Japanese yen and Mexican peso — that used to be so lucrative — is the worst in emerging markets this month, according to data compiled by Bloomberg.

In Brazil, investor concerns have revolved around the government’s commitment to the fiscal framework and speculation it would miss its budget targets, a move that could potentially undermine its debt sustainability. The Brazilian real was among the worst-performing currencies in the world Friday after the primary budget balance showed a bigger deficit than expected, adding to fiscal concerns. Holders of the country’s local-currency bonds have lost more than 7% in the past six weeks, while carry traders also lost 7%.

Colombia’s peso is off more than 6% this month as traders weigh the impact of increased spending in that country, which will pressure fiscal accounts.

Risks Ahead

There are more risks ahead. Latin America is highly vulnerable to the impact of the US presidential election, due to proximity and deep economic and trade ties.

Jared Lou, portfolio manager for emerging-market debt at William Blair Investment Management in New York, sees value in many of the region’s markets over the medium term. But policy changes following the vote in November could cause more problems in the short term, he said.

“Currencies could continue to be vulnerable depending on how the US election unfolds.”

In Argentina, local bonds have shed more than 11% amid investor worries over President Javier Milei’s ability to get a handle on the country’s monetary policy. In recent weeks, officials have struggled to rebuild its war chest of foreign reserves—a critical step to eventually lift currency and capital controls.

Adding to woes is an artificially strong Argentine peso in official markets. The government devalues it at a 2% per month pace in a move known as the crawling peg, a policy money managers see as unsustainable because it puts the peso behind the rate of inflation.

Some investors see hope for the region. Claudia Calich, head of emerging-market debt at M&G Investments in London, doesn’t see a clear substitute in portfolios.

“If you reduce Latin America, where do you go really?” she said.

--With assistance from Kevin Simauchi.

(Updates with Brazil real move in 14th paragraph.)

Most Read from Bloomberg Businessweek

Japan’s Tiny Kei-Trucks Have a Cult Following in the US, and Some States Are Pushing Back

The FBI’s Star Cooperator May Have Been Running New Scams All Along

RTO Mandates Are Killing the Euphoric Work-Life Balance Some Moms Found

How Glossier Turned a Viral Moment for ‘You’ Perfume Into a Lasting Business

©2024 Bloomberg L.P.