Yahoo Finance

Yahoo Finance Penn West Petroleum Ltd.’s Stunning Turnaround in Just 3 Numbers

Penn West Petroleum Ltd. (TSX:PWT)(NYSE:PWE) completed a dramatic turnaround last year. Thanks to a significant asset sale as the clock ticked away towards a looming debt deadline, and a meaningful improvement in costs, the Canadian driller is back on solid ground. The company is in the position where it can deliver strong growth at current commodity prices, which should create value for its investors over the long term.

Here are three numbers that show just how dramatically the company has improved over the past year.

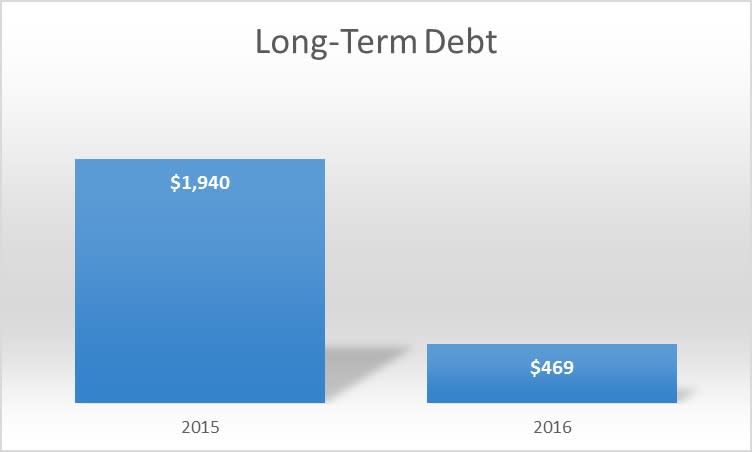

A 76% reduction in debt

The catalyst for Penn West Petroleum?s turnaround was the completion of several asset sales that not only repaid debt but simplified the company?s portfolio. Overall, the company closed $1.4 billion in asset sales last year. More importantly, despite the company?s financial troubles, it did not sell these assets at fire-sale prices. Instead, it received a premium to the value of the reserves, which were an estimated $1.1-1.2 billion.

By selling assets above that value, the company was able to deliver a remarkable 76% decrease in total debt by year-end:

Data source: Penn West Petroleum Ltd. Chart by author. In millions of Canadian dollars.

Meanwhile, the company?s leverage ratio has improved from nearly breaching its five times financial covenant to less than two times debt-to-funds from operations. Further, another benefit of jettisoning those assets is that the company has also reduced its asset retirement obligations from $397 million at the end of 2015 to $182 million at the end of last year.

Penn West has more balance sheet improvements on the way. The company recently completed an additional $65 million of asset sales and should close a final $10 million sale shortly. Those sales, combined with the expectation that it will generate free cash flow, should push its total debt down to $400 million by the end of the first quarter.

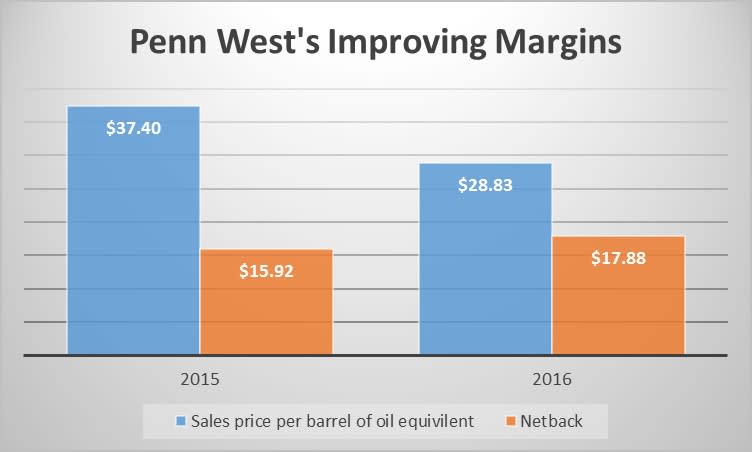

A 12% improvement in cash margins

One of Penn West?s other focuses last year was to improve its costs, which would enable it to make more money per barrel of production while also stretching its capital dollars. The company completed several initiatives to drive out costs, including selling some lower-margin assets. The net result was a 12% improvement in its netback despite a lower realized commodity price last year:

Data source: Penn West Petroleum Ltd. Chart by author.

Penn West expects margins to continue improving in 2017. The company?s aim is to boost its netback up to a range of $20-22 per BOE this year due to the expectation for higher oil prices than last year as well as benefiting from the lower operational costs of a more focused portfolio.

A 3% drop in the corporate decline rate

Oil production is a very capital-intense business. Drillers are in an endless cycle of reinvesting capital back into their asset base to both offset declining output from legacy wells and grow production. One thing Penn West has done over the past year is to reduce the amount of oil production it needs to replace each year by finding ways to shrink its decline rate.

These efforts are paying off, evidenced by the fact that the company?s corporate decline rate has improved from 22% at the end of 2015 to a current rate of 19%.

More of the company?s capex budget is going towards growth spending instead of maintenance. In fact, at the company?s current $180 million budget, the improving decline rate has freed up an incremental $15 million of capital it can now allocate to growth projects. For perspective, that?s enough money to enable Penn West to drill three wells in prospective zones as it tests its acreage. The company?s aim is to get its decline rate down to 15% in the future, which would free up another $20 million in growth capital.

Investor takeaway

Penn West Petroleum has come a long way over the past year. While the company?s ability to sell assets above the reserve value helped get the ball rolling, the initiatives to lower costs and the corporate decline rate have also helped in its turnaround efforts. The net result is a company that now has what it takes to thrive at lower oil prices.

You've probably never even heard of this up-and-coming e-commerce powerhouse headquartered in Eastern Ontario...

But, despite coming public just last year, it's already helping the likes of Budweiser... Tesla... Subway... and Red Bull move $9.9 BILLION (and counting) worth of goods online each year.

And now it's caught the eye of the legendary investor who got behind Amazon.com in 1997 -- just before it shot up over 23,000% and made investors like you and me rich beyond their wildest dreams.

Click here to discover why this investor says it's time to buy.

More reading

Fool contributor Matt DiLallo has no position in any stocks mentioned.

You've probably never even heard of this up-and-coming e-commerce powerhouse headquartered in Eastern Ontario...

But, despite coming public just last year, it's already helping the likes of Budweiser... Tesla... Subway... and Red Bull move $9.9 BILLION (and counting) worth of goods online each year.

And now it's caught the eye of the legendary investor who got behind Amazon.com in 1997 -- just before it shot up over 23,000% and made investors like you and me rich beyond their wildest dreams.

Click here to discover why this investor says it's time to buy.

Fool contributor Matt DiLallo has no position in any stocks mentioned.