Yahoo Finance

Yahoo Finance One of the most frequently cited risks to stocks in 2023 is 'overstated'

This post was originally published on TKer.co

Stocks fell last week, with the S&P 500 declining 3.4%. The index is now up 9.9% from its October 12 closing low of 3,577.03 and down 17.9% from its January 3 closing high of 4,796.56.

Last week I published a roundup of Wall Street forecasters’ outlook for stocks in 2023.

In a nutshell, they were unusually bearish with more than half of them predicting the S&P 500 to close 2023 lower on the year.

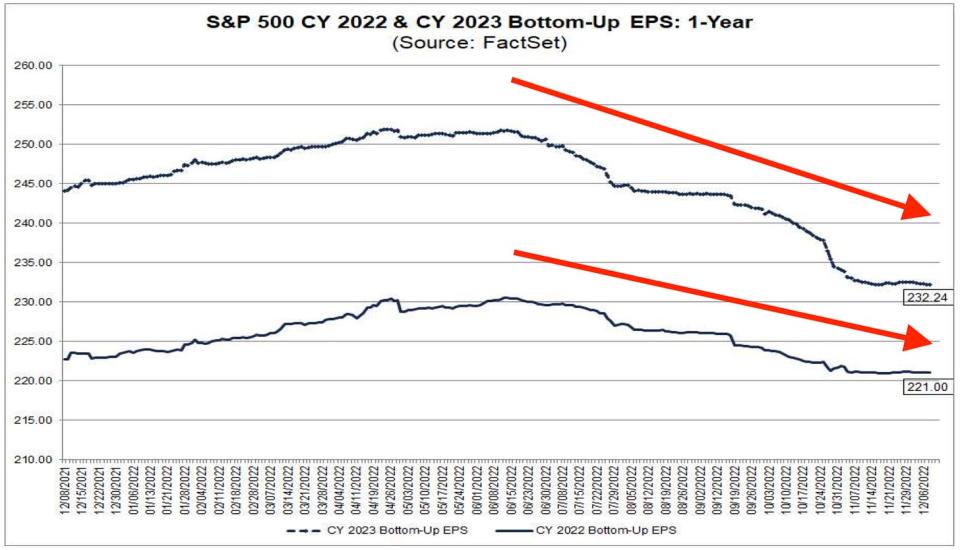

One commonly cited risk was the expectation that estimates for earnings would be revised down further from current levels. (Yahoo Finance’s Myles Udland had a good discussion about this on Friday.) According to FactSet, analysts expect S&P 500 earnings to climb to $232 per share in 2023. Even after months of downward revisions, this figure is higher than all the estimates provided by the equity strategists cited by TKer.

Because earnings are the most important driver of stocks in the long run, this is a bit alarming.

However, at least one top analyst argues these concerns are “overstated.”

There are at least two things to consider.

Knowing where earnings are going won’t help you

First, the next year’s earnings growth rate won’t tell you much about what stock prices will do in the near-term.

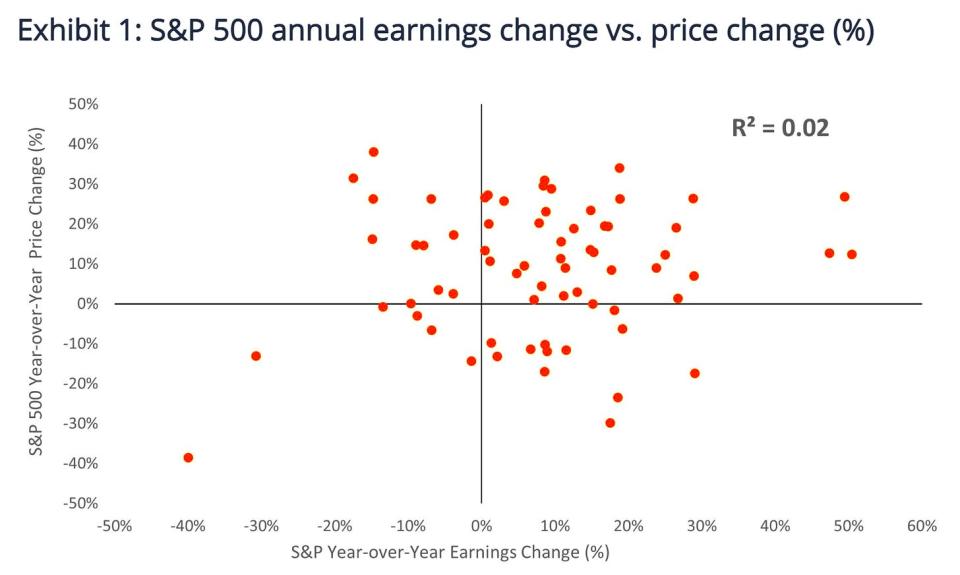

Aneet Chachra, portfolio manager at Janus Henderson, reviewed the history and found that the two variables effectively had no relationship.

“Unfortunately, correctly predicting future earnings is less useful than one would think,” Chachra found (via John Authers). “Over the long run, S&P 500 earnings and the index itself have unsurprisingly tracked each other, with both series growing at an 8% per annum average pace. But surprisingly, the correlation between year-over-year changes in annual earnings and the S&P 500 Index is almost zero!”

As you can see in Chachra’s chart, the scatterplot is pretty chaotic. With an R-squared of 0.02, there’s effectively no statistical linear relationship between one-year earnings growth and one-year stock market performance.

“‘Knowing’ next year’s earnings growth in advance provides remarkably little insight into what next year’s stock price return will be,” Chachra said.

This is in line with the fact that valuations in one year tell you little about what stock prices will do in the next year. And while we’re talking about the perils of predicting the short-term, the past year’s stock market returns don’t tell you much about the next year’s returns, either.

The market bottom might be in regardless

Second, earnings have historically bottomed after stocks bottomed. In other words, we can’t rule out the possibility that the October low in the S&P 500 is a typical precursor to some eventual short-term low in earnings we have yet to learn about.

Ari Wald, head of technical analysis at Oppenheimer, ran the numbers and published his findings in a November 26 research note. Emphasis added:

None of this is to suggest we can rule out the risk of stocks struggling in 2023. Rather, it’s just to caution against getting too confident about the prospect of stocks falling further, especially with prices down already.

Reviewing the macro crosscurrents 🔀

There were a few notable data points from last week to consider:

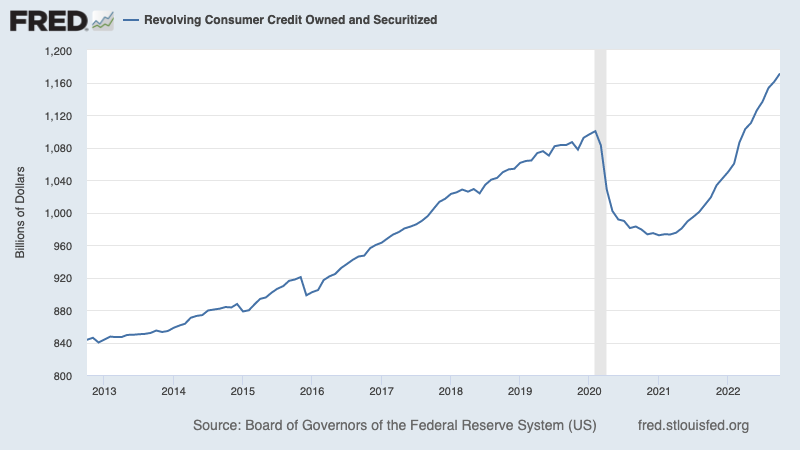

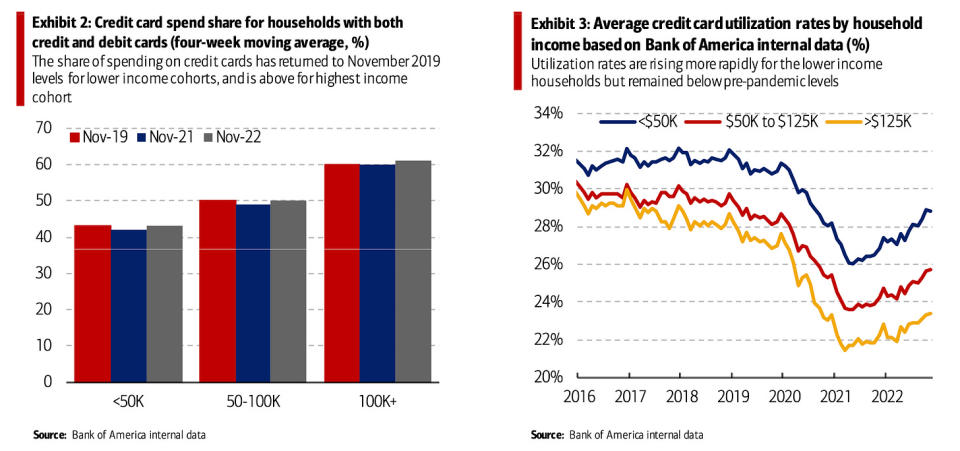

💳 Consumers are taking on more debt. According to Federal Reserve data, total revolving consumer credit outstanding increased to $1.17 trillion in October. Revolving credit consists mostly of credit card loans.

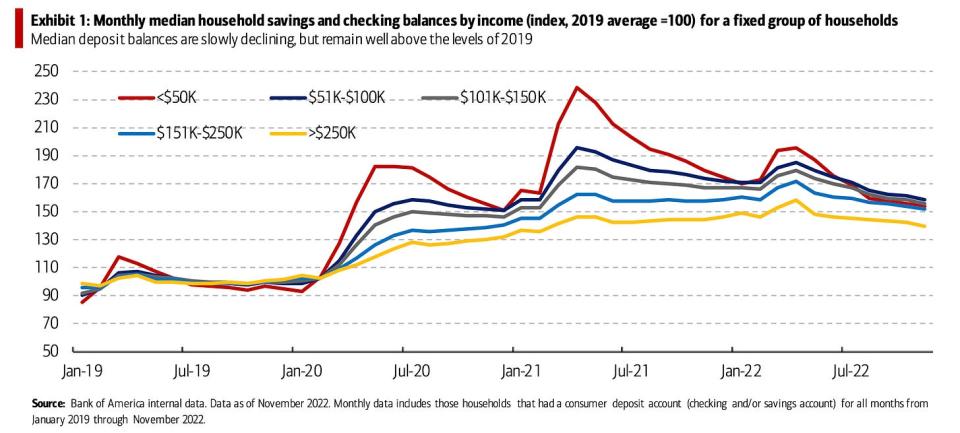

👍 But overall, consumers remain in good financial shape. According to Bank of America, household checking and savings account balances remain above pre-pandemic levels across income groups.

And while credit card usage has been increasing, consumers are far from maxing out their cards — as reflected by utilization rates below pre-pandemic levels.

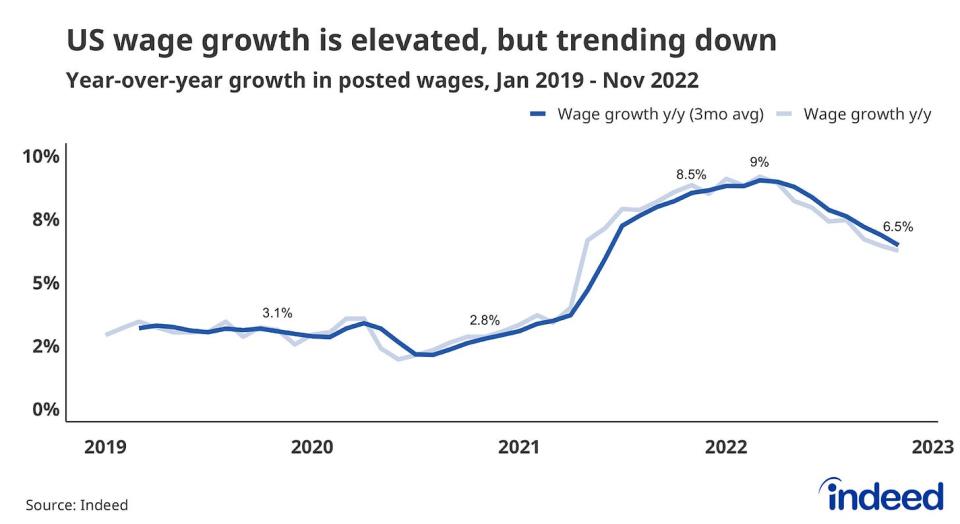

💸 Wages are growing, but growth is slowing. From Indeed Hiring Lab: “In November, posted wages grew a strong 6.5% year-over-year. But that seemingly impressive number represented a substantial deceleration from the peak of 9% growth recorded in March 2022. The drop has been broadly felt, with less than one-fifth of job categories seeing steady or increasing wage growth.“

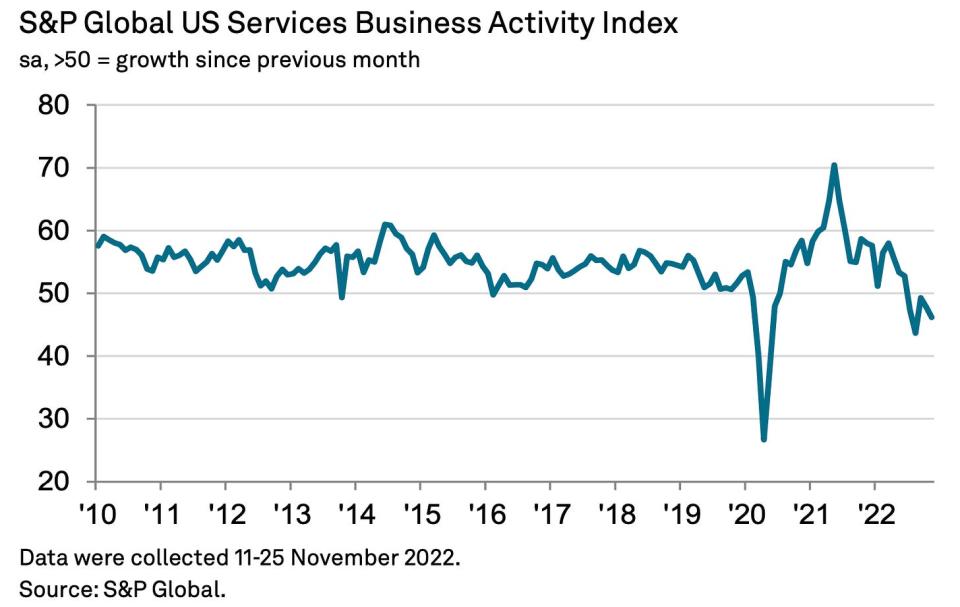

🤷🏻♂️ Service sector surveys paint a mixed picture. According to an ISM survey, services sector activity growth accelerated in November. From the report: “Based on comments from Business Survey Committee respondents, increased capacity and shorter lead times have resulted in a continued improvement in supply chain and logistics performance. A new fiscal period and the holiday season have contributed to stronger business activity and increased employment.“

However, a similar survey conducted by S&P Global suggested the opposite. From the report: “The survey data are providing a timely signal that the health of the US economy is deteriorating at a marked rate, with malaise spreading across the economy to encompass both manufacturing and services in November. The survey data are broadly consistent with the US economy contracting in the fourth quarter at an annualized rate of approximately 1%, with the decline gathering momentum as we head towards the end of the year.“

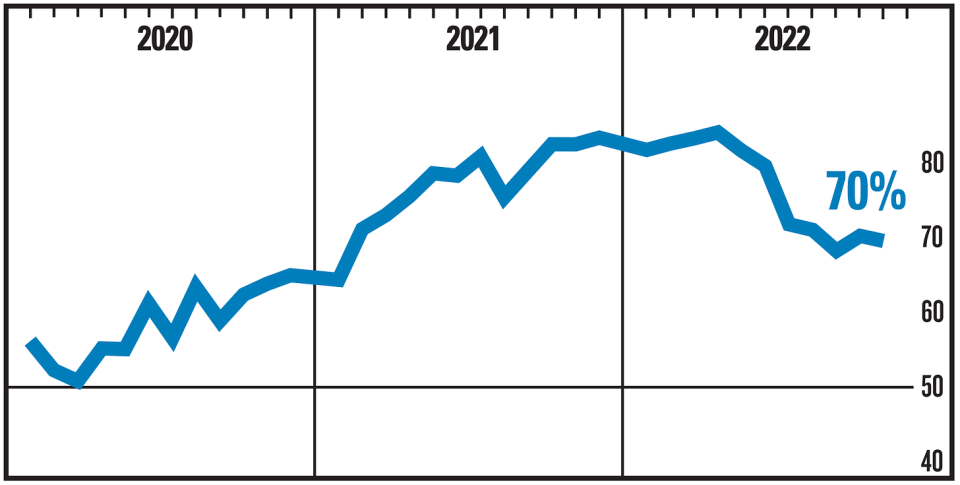

📉 Service price inflation is easing. The ISM and S&P Global services surveys both confirmed that price inflation for services cooled in November. From the ISM: “The Prices Index was down 0.7 percentage point in November, to 70 percent.“ From S&P Global: “A striking development is the extent to which companies are increasingly reporting a shift towards discounting in order to help stimulate sales, which augurs well for inflation to continue to retrench in the coming months, potentially quite significantly.“

📉 Wholesale price inflation is easing. According to the Bureau of Labor Statistics, the producer price index (PPI) in November was up 7.4% from a year ago. Excluding food, energy, and trade, core prices were up 4.9%. On a month-over-month basis, PPI was up 0.3% while core PPI accelerated to 0.3%.

⛽️ Gas prices are down. This year’s spike in gasoline prices has disappeared.

👍 Expectations about inflation improve. From the University of Michigan’s December Survey of Consumers: “Year-ahead inflation expectations improved considerably but remained relatively high, falling from 4.9% to 4.6% in December, the lowest reading in 15 months but still well above 2 years ago. Declines in short-run inflation expectations were visible across the distribution of age, income, education, as well as political party identification. At 3.0%, long run inflation expectations has stayed within the narrow (albeit elevated) 2.9-3.1% range for 16 of the last 17 months.“

⛓️ Supply chains tightened, but are much better than they were a year ago. The New York Fed’s Global Supply Chain Pressure Index1 — a composite of various supply chain indicators — deteriorated slightly in November. From the report: "The largest contributing factor to the rise in supply chain pressures was Chinese delivery times, though improvements were shown in U.S. delivery times and Taiwanese purchases."

Putting it all together 🤔

Inflation is cooling from peak levels. Nevertheless, inflation remains hot and must cool by a lot more before anyone is comfortable with price levels. So we should expect the Federal Reserve to continue to tighten monetary policy, which means tighter financial conditions (e.g. higher interest rates and tighter lending standards). All of this means the market beatings will continue and the risk the economy sinks into a recession will intensify.

But it’s important to remember that while recession risks are rising, consumers are coming from a very strong financial position. Unemployed people are getting jobs. Those with jobs are getting raises. And many still have excess savings to tap into. Indeed, strong spending data confirms this financial resilience. So it’s too early to sound the alarm from a consumption perspective.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

As always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a terrible year so far, the long-run outlook for stocks remains positive.

This post was originally published on TKer.co

Sam Ro is the founder of TKer.co. Follow him on Twitter at @SamRo

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance

Download the Yahoo Finance app for Apple or Android

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube