Yahoo Finance

Yahoo Finance Is NiSource Inc. (NYSE:NI) A Risky Dividend Stock?

Is NiSource Inc. (NYSE:NI) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

A slim 2.7% yield is hard to get excited about, but the long payment history is respectable. At the right price, or with strong growth opportunities, NiSource could have potential. Some simple research can reduce the risk of buying NiSource for its dividend - read on to learn more.

Explore this interactive chart for our latest analysis on NiSource!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. In the last year, NiSource paid out 239% of its profit as dividends. Unless there are extenuating circumstances, from the perspective of an investor who hopes to own the company for many years, a payout ratio of above 100% is definitely a concern.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. Unfortunately, while NiSource pays a dividend, it also reported negative free cash flow last year. While there may be a good reason for this, it's not ideal from a dividend perspective.

Remember, you can always get a snapshot of NiSource's latest financial position, by checking our visualisation of its financial health.

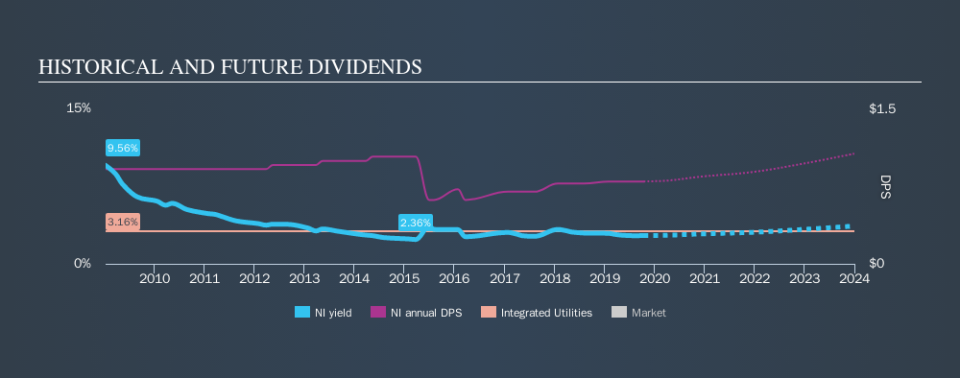

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. NiSource has been paying dividends for a long time, but for the purpose of this analysis, we only examine the past 10 years of payments. This dividend has been unstable, which we define as having fallen by at least 20% one or more times over this time. During the past ten-year period, the first annual payment was US$0.92 in 2009, compared to US$0.80 last year. This works out to be a decline of approximately 1.4% per year over that time. NiSource's dividend hasn't shrunk linearly at 1.4% per annum, but the CAGR is a useful estimate of the historical rate of change.

A shrinking dividend over a ten-year period is not ideal, and we'd be concerned about investing in a dividend stock that lacks a solid record of growing dividends per share.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. NiSource's EPS have fallen by approximately 14% per year. With this kind of significant decline, we always wonder what has changed in the business. Dividends are about stability, and NiSource's earnings per share, which support the dividend, have been anything but stable.

We'd also point out that NiSource issued a meaningful number of new shares in the past year. Regularly issuing new shares can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

Conclusion

To summarise, shareholders should always check that NiSource's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. We're a bit uncomfortable with NiSource paying out a high percentage of both its cashflow and earnings. Second, earnings per share have been in decline, and its dividend has been cut at least once in the past. In this analysis, NiSource doesn't shape up too well as a dividend stock. We'd find it hard to look past the flaws, and would not be inclined to think of it as a reliable dividend-payer.

Given that earnings are not growing, the dividend does not look nearly so attractive. Businesses can change though, and we think it would make sense to see what analysts are forecasting for the company.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.