Yahoo Finance

Yahoo Finance Middle East Crisis: Geopolitics Remains a Downside Risk for the Global Economic and Credit Outlook

Although a full-scale military confrontation between Iran and Israel is not Scope Ratings’ base case, the recent confrontation between Israel and Iran has heightened risks for the Middle East.

Beyond constructive efforts around de-escalation from regional stakeholders, the United States and the European Union, we can read some positives from the degree of moderation in Iran’s reprisal, to avoid a damaging spiralling conflict with Israel.

Iran’s drone and missile attack – telegraphed days beforehand – alongside the fact it was largely thwarted by the air defences of Israel and allies could let Tehran claim retribution for Israel’s alleged assassination of Iranian military commanders in Damascus at the same time as presenting an off-ramp for Israel. Nevertheless, retaliation from Israel appears possible if not probable. The question at this stage centres on what form any reprisal takes and how much restraint Israel exercises, including in Gaza.

A Wider Conflict or Direct Confrontation Would Disrupt Global Commodity Markets

Oil markets have already priced in protracted tension and elevated geopolitical risk, with Brent prices standing at around USD 90 a barrel (albeit slightly lower this week). However, any further intensification of conflict within the region – even if this falls short of any full-scale regional war – could have significant economic repercussions beyond the Middle East through higher commodity prices, disrupted shipping routes and risk-off in financial markets.

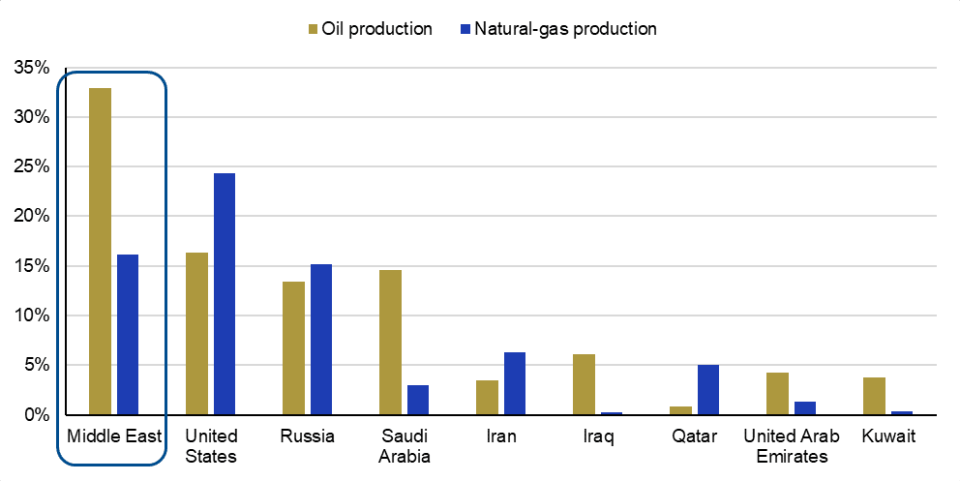

A wider Middle-East conflict could disrupt up to a third of global oil production and about 15% of natural gas production (Figure 1). Iranian oil production is comparatively modest, at around 3.5% of global production but its natural-gas production is more meaningful (at about 6%).

Internationally, the Strait of Hormuz is of strategic importance for crude-oil producers including Saudi Arabia (14.5% of global production), Iraq (6%), the United Arab Emirates (4%) and Kuwait (4%). The Strait is also crucial for Qatari gas exports (5%), especially to Europe since the international sanctions applied on imports from Russia.

Figure 1. Military confrontation foreseen disrupting Middle-East oil and gas production

Oil and natural-gas production, % world aggregates, 2022

A Further Commodity-price Shock Might Renew Inflationary Pressures, Raise Economic Uncertainty

As we highlighted in our Sovereign Outlook 2024, geopolitics and further supply-side crises represent a core risk to getting inflation to 2% price-stability goals. This is especially true during the current final mile for cutting above-target inflation as core and services inflation are already displaying signs of stickiness.

Any amplification of the Middle-East conflict could compel core central banks to postpone and/or temper future reductions in interest rates. Even if the ECB and other central banks begin lowering official rates later this year as expected, a new normal of a more unpredictable Middle East raises the spectre of a scenario resembling the 1970s with a higher steady state of rates. A baseline of higher rates for longer and risk of central-bank pivots if inflation surprises on the upside might correspond with a degree of further tightening of financial conditions globally.

Geopolitical Tensions to Remain a Core Credit Challenge

There are clear sovereign-credit risks to Israel from the current geopolitical stand-off. However, beyond Israel, higher military expenditure because of global geopolitical risks, counter-cyclical fiscal policies compensating for economic uncertainty and higher-for-longer interest rates represent broader risk factors for sovereign credit ratings.

We took these risks into consideration in a balanced view on sovereign ratings for 2024, but geopolitics remain a main concern and are likely to remain one for the credit outlook for 2025.

For a look at all of today’s economic events, check out our economic calendar.

Dennis Shen is Chair of the Macroeconomic Council at Scope Ratings GmbH. Thomas Gillet, a Director in sovereign ratings at Scope Ratings, contributed to writing this commentary.

This article was originally posted on FX Empire