Yahoo Finance

Yahoo Finance Is Memex (CVE:OEE) Weighed On By Its Debt Load?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Memex Inc. (CVE:OEE) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Memex

What Is Memex's Net Debt?

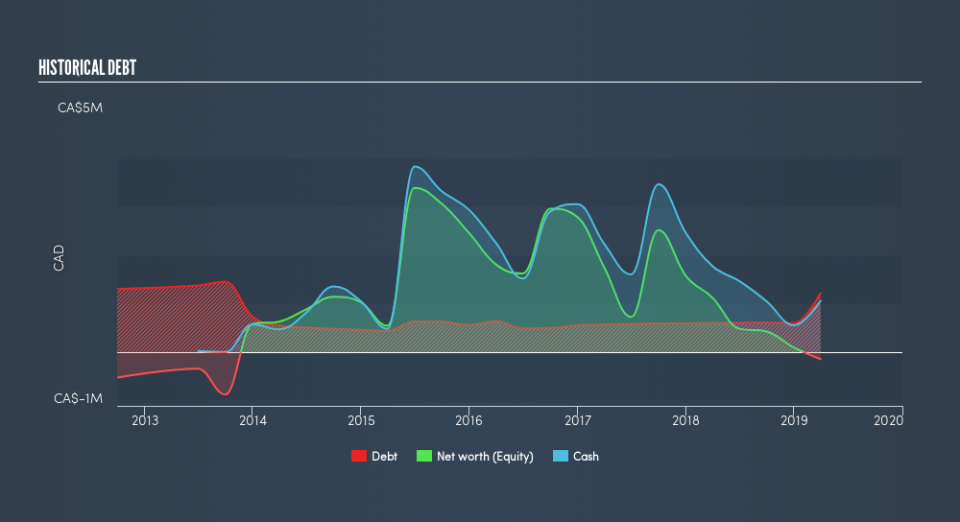

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Memex had CA$1.22m of debt, an increase on CA$600.5k, over one year. On the flip side, it has CA$1.06m in cash leading to net debt of about CA$156.7k.

A Look At Memex's Liabilities

Zooming in on the latest balance sheet data, we can see that Memex had liabilities of CA$1.69m due within 12 months and liabilities of CA$1.22m due beyond that. On the other hand, it had cash of CA$1.06m and CA$1.10m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CA$750.1k.

Given Memex has a market capitalization of CA$4.02m, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Memex will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Memex managed to grow its revenue by 37%, to CA$3.1m. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

Even though Memex managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. Indeed, it lost a very considerable CA$1.4m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn't help that it burned through CA$1.3m of cash over the last year. So in short it's a really risky stock. For riskier companies like Memex I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.