Yahoo Finance

Yahoo Finance Mastercard's (MA) Q4 Earnings Beat on Resilient Spending

Mastercard Incorporated MA reported fourth-quarter 2022 adjusted earnings of $2.65 per share, which outpaced the Zacks Consensus Estimate and our estimate of $2.56. The bottom line advanced 13% year over year.

The leading technology company in the global payments industry, Mastercard’s revenues amounted to $5,817 million, which rose 12% year over year in the quarter under review. The top line beat the consensus mark of $5,766 million and our estimate of $5,792.6 million.

Resilient consumer spending, recovery in cross-border travel, cross-border volume growth, higher gross dollar volume ("GDV") and increased switched transactions contributed to the strong quarterly results of Mastercard. Its exposure to Asian economies played a positive role in boosting performance. However, the upside was partly offset by rising operating expenses.

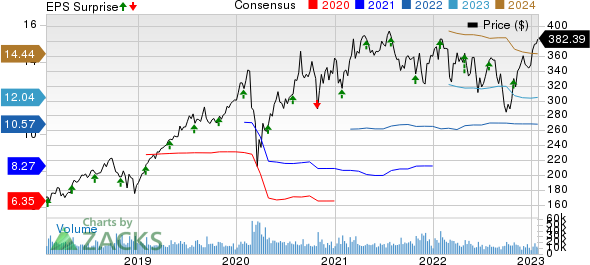

Mastercard Incorporated Price, Consensus and EPS Surprise

Mastercard Incorporated price-consensus-eps-surprise-chart | Mastercard Incorporated Quote

Q4 Operational Performance

In the quarter under review, GDV (representing the aggregated dollar amount of purchases made and cash disbursements obtained from MasterCard-branded cards) improved 8% year over year on a local-currency basis to $2,133 billion. This was lower than our estimate of $2,189 billion.

Cross-border volumes (a key measure that tracks spending on cards beyond the issuing country) improved 31% year over year on a local-currency basis. Switched transactions, which indicate the number of times a company’s products are used to facilitate transactions, came in at 34 billion. The metric rose 8% year over year.

Other revenues advanced 11% year over year to $2,045 million, including a 1% increase from acquisitions. Remaining growth resulted from Cyber & Intelligence and Data & Services solutions. It beat our estimate of $1,910.1 million.

Rebates and incentives climbed 14% year over year in the quarter under review while our estimate for the same suggested 13.1% growth.

MA’s clients issued 3.1 billion Mastercard and Maestro-branded cards as of Dec 31, 2022.

Operating expenses escalated 10% year over year to $2,633 million, primarily due to higher general and administrative expenses. The metric was lower than our estimate of $2,657.9 million.

Operating income of $3,184 million grew from $2,827 million a year-ago and beat our estimate of $3,134.6 million. Operating margin improved 50 basis points year over year to 54.7% and marginally beat our estimate of 54.1%.

Balance Sheet (as of Dec 31, 2022)

Mastercard exited the fourth quarter with cash and cash equivalents of $7,008 million, down from the 2021-end level of $7,421 million. The figure is way higher than the current portion of long-term debt ($274 million).

Total assets of $38.7 billion increased from the $37.7 billion figure at 2021 end.

Long-term debt amounted to $13.7 billion, which increased from the $13.1 billion figure as of Dec 31, 2021.

Total equity of $6.4 billion dropped from the 2021-end level of $7.4 billion.

Cash Flows

In 2022, net cash provided by operating activities climbed 18.3% from the prior-year comparable period’s level to $11.2 billion.

Share Repurchase and Dividend Payout

Mastercard bought back 7.4 million shares for $2.4 billion in the fourth quarter. It had $11.6 billion left under its authorized share buyback program as of Jan 23, 2022.

Moreover, MA paid out dividends worth $473 million in the quarter under review.

1Q23 Outlook

For the first quarter of 2023, management anticipates net revenues to register the high-end of high-single digit growth from the year-ago quarter’s reported figure. Operating expenses are expected to witness mid-single-digit growth year over year.

2023 Outlook

Management projected net revenues to witness low-teens growth from the 2022 figure of $22,237 million. Operating expenses were estimated to see mid-single-digit growth from the 2022 figure of $9,973 million.

Adjusted earnings of $10.65 per share increased 27% year over year in 2022. The Zacks Consensus Estimate for the metric for 2023 is currently pegged at $12.04 per share.

Zacks Rank & Key Picks

Mastercard currently has a Zacks Rank #3 (Hold). Some better-ranked stocks in the broader Business Services space are Green Dot Corporation GDOT, FirstCash Holdings, Inc FCFS and EVERTEC, Inc. EVTC, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Based in Austin, TX, Green Dot is a pro-consumer bank holding company and personal banking provider. The Zacks Consensus Estimate for GDOT’s 2022 earnings indicates an 11.3% year-over-year jump.

Headquartered in Fort Worth, TX, FirstCash is a retail pawn stores operator. The Zacks Consensus Estimate for FCFS’ 2022 earnings indicates 29.7% year-over-year growth.

San Juan, Puerto Rico-based EVERTEC has a major transaction processing business. The Zacks Consensus Estimate for EVTC’s 2022 bottom line is pegged at $2.41 per share, which remained stable over the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Mastercard Incorporated (MA) : Free Stock Analysis Report

FirstCash Holdings, Inc. (FCFS) : Free Stock Analysis Report

Green Dot Corporation (GDOT) : Free Stock Analysis Report

Evertec, Inc. (EVTC) : Free Stock Analysis Report