Yahoo Finance

Yahoo Finance Markets think the midterms could be as big as the presidential election

The midterm elections are less than three weeks away.

And traders are prepping for some stock market volatility.

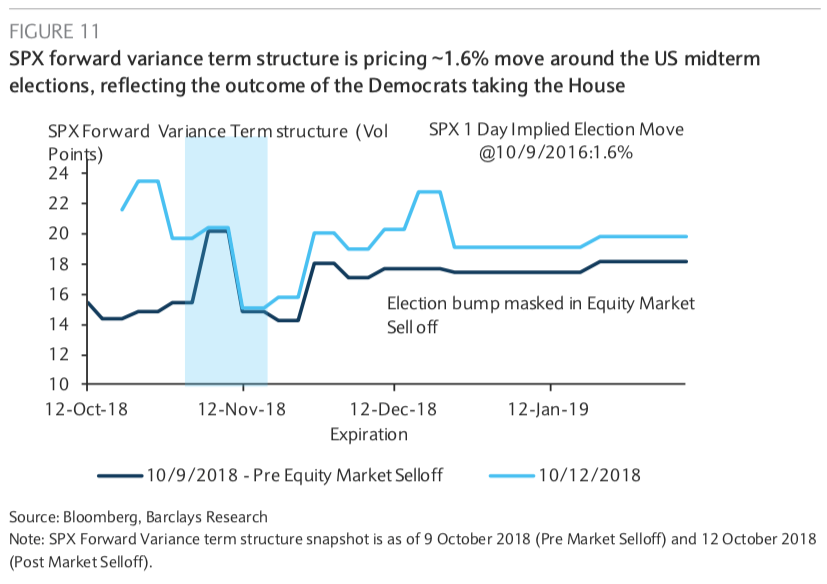

According to strategists at Barclays, the options market is pricing in a 1.6% swing on election night, a modest swing given the recent volatility we’ve seen in the stock market.

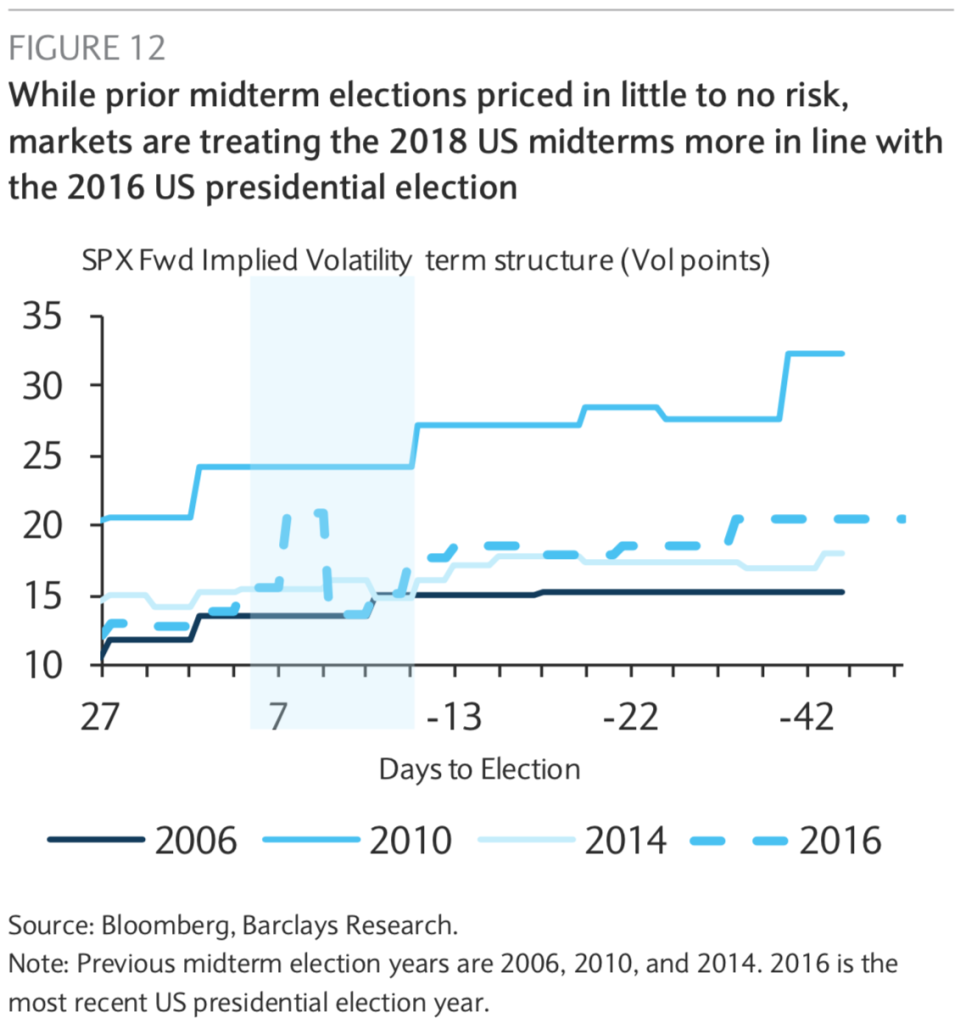

But this market positioning is notable considering investors usually price in little meaningful volatility around midterm elections.

Those who recall the wild market swings we saw around the 2016 presidential election — U.S. stock futures went limit down on election night before staging a huge rally that continued unabated through the early months of Trump’s presidency — will perhaps be relieved to see markets pricing in more muted action around the midterms.

Markets pricing in this kind of swing for a midterm election reflects the more heightened political climate in the U.S., and indicates investors are loath to forget the election night surprises seen in 2016 when both the Brexit vote and Trump’s win shook markets.

“Historically, we haven’t seen excess moves priced in by the equity volatility market around midterm elections,” Barclays said in its note published Thursday. “The reason for the muted risk pricing in the past was that the magnitude of the realized SPX move on midterm election days has been lower than the magnitude of moves on U.S. presidential election days.”

And as the following chart shows, the last three midterm elections — including the 2010 midterm when the House was completely flipped while the economy still struggled following the financial crisis — were seen ahead of time as relative non-events by markets. But that is not how investors see the world today.

Barclays adds that, “The midterm elections are often seen as a referendum on the president, and this year due to the heightened political polarization in the United States, the SPX variance term structure is behaving in a similar manner to the 2016 presidential election.

“The similarity to the variance term structure in the run up to 2016 presidential election highlights investors are perhaps pricing risks arising from the other two, less likely, scenarios: Blue Tsunami (Democrats taking both House and Senate) and Red Wall (Republicans keeping both House and Senate).”

In other words, the options market might be implying a 1.6% swing on election night, but traders aren’t ruling anything out.

“A few weeks ago there was a clear ‘bump’ in the term structure, indicating the event volatility being priced by the market,” Barclays said in a note published Thursday.

“If we assume that the entire increase in forward volatility is concentrated on the Election Day, this would correspond to a move of 1.6%, which is fairly muted. However, at present, given the current elevated levels of volatility, the event volatility is hard to discern.”

Last week each of the major averages lost more than 3% as the S&P 500 logged its third day this year of a drop greater than 2%. In 2016 and 2017, the benchmark index experienced no days of a drop this large.

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland