Yahoo Finance

Yahoo Finance How To Manage All the Extra Debt You Piled Up in 2020

If you’ve piled on debt this year, you’re not alone. A recent survey conducted by Clever found that the average American has taken on an additional $7,512 in debt since this time last year, and 54% have missed or deferred at least one payment in 2020.

“Having debt is not some kind of moral failing,” said debt expert Jackie Beck. “You are still a worthwhile person. Do what you can right now to get through things.”

When you’re in debt it can definitely feel overwhelming, but with a plan in place, you can begin to pay it down over time. I spoke to financial experts to get their best advice on how to pay down any extra debt you took on this year. Here’s how to tackle your debt and start 2021 on better financial footing.

Last updated: Nov. 18, 2020

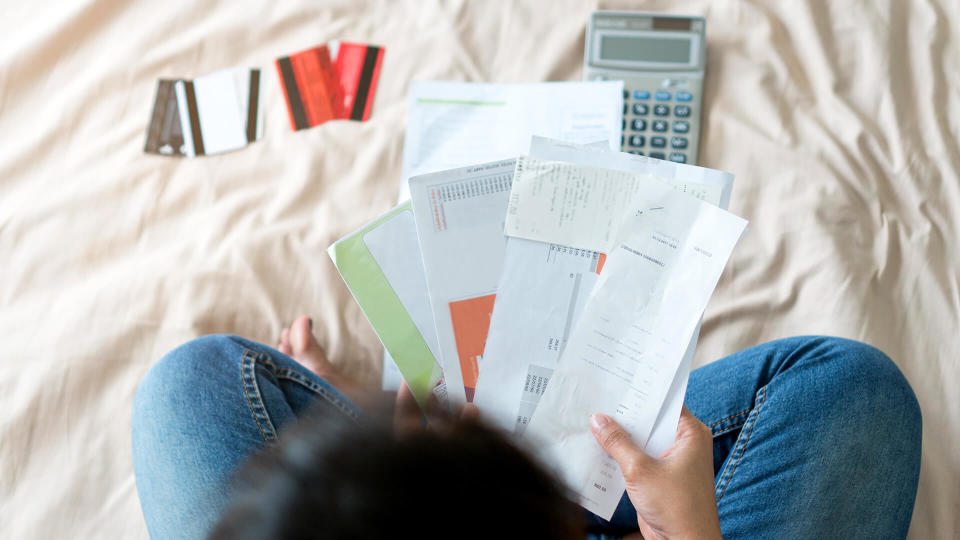

Create a List of All Your Debt

It’s important to have a clear picture of exactly how much debt you have.

“The first thing you need to do is create a budgeting spreadsheet,” said Drew Cheneler, founder of the personal finance blog SimpleMoneyLyfe.com. “Find out who you owe debt to and how much. Separate it by categories: credit cards, student loans, [other] loans, etc.”

You should also include due dates so you don’t miss any payment deadlines, added Patrina Dixon of It’s My Money.

Research Financial Assistance Programs That May Be Available

You may be able to have some of your debt forgiven.

“It’s a good idea to start to look at what financial assistance is available to forgive some of that debt, especially if it relates to some of the government programs offered this year,” said Chalmers Brown, CTO at Due.

Reach Out to Your Lenders

If it seems like you have more debt than you can manage, ask for help.

“Due to the extraordinary situation that the pandemic has caused, many lenders are more flexible than they might have been in the past,” said Marc Andre, personal finance blogger at VitalDollar.com. “They may have a hardship program or a way to accommodate people who are in difficult situations, but you probably won’t know about this unless you ask. Call the lender to explain your situation and ask if there is anything they can do to help. They might be willing to delay payments or adjust the terms in some way that makes it possible for you to pay.”

“It’s important that you’re proactive about this and reach out to the lender as soon as possible,” he added. “You’ll be more likely to get help if you reach out before you’ve already fallen behind on the payment.”

Consider Consolidating or Refinancing Your Debt

Interest rates are low, which means you may be able to benefit from refinancing any loans you have.

“See if you can consolidate or refinance your debt to make sure your repayment terms are as favorable as possible from the start,” said Anna Barker, personal finance expert and founder of LogicalDollar. “In particular, reducing the interest rate — including taking advantage of any interest-free periods — could save you thousands of dollars over the life of your loan.”

If you are a homeowner, refinancing your home could help you get out of the hole.

“Refinance and take some equity out to consolidate all the debt at a much lower rate,” serial entrepreneur John Rampton said. “Now that home values are on the rise and interest rates are at near historic lows, this could be a good way to save money on interest charges and accelerate pay-down.”

Consider a Balance Transfer Credit Card

Opening a balance transfer credit card is another option to reduce your payments, especially if you’re specifically dealing with credit card debt. However, make sure you understand repayment terms.

“For someone who has one or more credit card accounts carrying high interest rates, transferring the balance(s) to a card with a low- or zero-interest rate can help get that debt paid off,” said Sean Fox, president of Freedom Debt Relief. “They are generally available only to people with good credit, fees can be high and the promotional rates that make them work will expire. Someone in financial hardship must be sure that they can pay off the balance before then.”

Delay Any Government-Backed Loans If You Need To

“Keep in mind that the CARES Act allows borrowers with government-backed loans to delay payments for up to one year,” personal finance blogger Cara Palmer said.

While you will have to pay these debts back eventually, delaying repayment can help you focus on paying down more pressing debts.

Find Out: From $300,000 in Debt to Zero — How Real People Repaid Their Debts Fast

Track Your Spending

If paying off your debt is a priority, you should be mindful of how you’re using every dollar.

“Closely track your spending so that you know exactly where each dollar is going,” Barker said. “Following this strategy makes sure that you’re not accidentally wasting any money that should be funneled towards paying off your debt. Your budget should have the aim of allowing you to make more than your minimum debt repayments, which will likely involve you having to strictly control your spending.”

“Look at what you spent and where so you can determine which categories you can immediately lower spending in to allocate more to debt repayment,” added Yenn Lei, head of engineering at Calendar.

You may have to cut out some unnecessary costs during this debt repayment period.

“Try eliminating any monthly subscriptions that aren’t necessary and cook from home instead of getting takeout,” said Sam Hawrylack, co-owner of the personal finance blog How To FIRE. “Be very careful to actually understand wants versus needs.”

“Cutting out cable or not going out to eat as often might not be fun, but short-term sacrifice for long-term financial freedom can be well worth it,” added Misty Larkins, president of Relevance.

You may also try to renegotiate some of your monthly bills that fit into the “needs” category.

“Will your utility companies defer or discount your monthly payment for a few months?” said Jason Hennessey, founder of Hennessey Digital. “Many people can probably save between $250 to $500 per month just by making a few phone calls and asking for some flexibility or removing services that are more of a luxury.”

Use a Budgeting App To Get a Clear Picture of Your Finances

“Consider downloading a mobile budgeting app that will help you track your finances and debt,” Cheneler said. “Sometimes a holistic view is all you need to kickstart paying off debt.”

Utilize Community Programs To Cut Down on Expenses

“Take advantage of free community services, whether it’s grocery giveaways, community meals, or goods and services being offered through your network,” said Julie Rains, founder of Investing to Thrive. “For example, some folks are reaching out via the NextDoor app to both get and give help. When you’re able, you can give back.”

Every dollar saved is another dollar you can put toward debt repayment, so don’t feel shy about accepting help right now.

Remove Saved Credit Card Data From Apps and Websites

Keeping your credit card information saved on shopping websites and apps “makes it too easy to spend,” said Lawrence Gonzalez, founder of The Neighborhood Finance Guy. Those dollars you are mindlessly spending are better off going toward debt repayment.

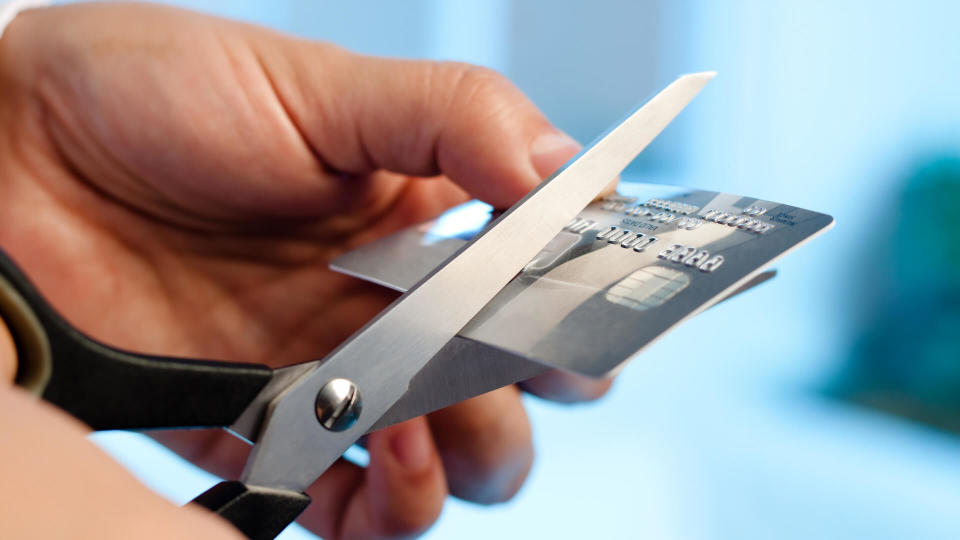

Ditch Your Credit Card Altogether

“As you pay debt off, do everything in your power not to create new debt in the process,” said Stephen Dalby, founder and CEO of Gabb Wireless.

Every time you swipe your credit card, you’re potentially piling on more debt.

“Commit to not taking on more debt by using cash instead of credit,” said Ashley Lee, millennial money coach, personal finance enthusiast and host of “The Financial Key” podcast.

Find Ways To Increase Your Income

Making more money will enable you to pay off your debt faster.

“You should look into increasing your income, such as through a side hustle, so that any extra money you’re able to generate can also be used to destroy your debt,” Barker said. “This is a particularly good strategy for paying off debt that’s built up in 2020, as there are so many online-based side hustles at the moment that are very lucrative, especially with a lot of people being at home. Online tutoring, for example, is a great opportunity to make some extra cash, no matter what your area of expertise is.”

Other examples of side hustles you may take on include delivering groceries with Instacart or making yourself available for odd jobs on TaskRabbit, Kate Braun of DollarSanity suggested.

“Getting a second job will help you tremendously,” added Peter Koch, a personal finance expert, also at DollarSanity. “Consider that money as ‘debt money’ so you don’t have to use the money you earn at your full-time job.”

Increase Your Earning Potential

In addition to getting a side hustle, work on acquiring new skills that can help you land a better-paying job.

“Learn high-income producing skills: think sales, marketing and copywriting to name a few,” said Jercori Freeman, founder of Wealthchild.com. “Learn and apply these skills, and you‘ll be able to eliminate your debt.”

Read More: 16 Key Signs That You Will Always Be In Debt

Sell Off Any Unused Items Around Your House

You can also bring in extra money for debt repayment by selling items you are no longer using.

“See if you have items lying around that you can sell on eBay, OfferUp or Facebook Marketplace,” said Anthony Kirlew, financial coach at Fiscally Sound. “Just make sure to use the money to knock out that debt!”

Pay Yourself First

Dedicate a portion of every paycheck to paying down your debt.

“One of the best tips for meeting any financial goal is to always pay yourself first,” Barker said. “This means that you should commit a certain amount of your income to paying off your debt as soon as the money hits your account rather than waiting to see what’s left at the end of the month. Otherwise, there’s a risk that there won’t be enough left over for you to meet your financial goals.”

Start Off by Paying Down High-Interest Debt

There are several debt repayment methods, but Cheneler recommends focusing on paying high-interest debt first.

“This will most likely be credit card debt,” he said.

April Lewis-Parks, director of education and corporate communications at Consolidated Credit, also recommends this debt repayment method.

“Always payoff the highest APR debt first to make the most of your money,” she said.

Or, Start by Paying Down Your Smallest Debt

“List your debts smallest to largest, regardless of the interest rate,” said Rachel Cruze, author, financial expert and host of “The Rachel Cruze Show.” “Throw everything you can at the smallest one and make minimum payments on the rest. Once you pay off your smallest debt, attack the next one. Repeat this process until you’re debt-free. We call this the debt snowball at Ramsey Solutions, and we see people pay off their debt in an average of 18 to 24 months.”

This repayment method is effective for people who have many different debts and want to feel like they’re making a dent in it right away.

“This works because it gives you confidence,” said Deacon Hayes, founder of WellKeptWallet.com. “You are able to pay off a small debt quickly and you feel like you are getting somewhere. This is important because it can help you stay motivated to keep going to tackle all of the rest of your debt.”

Derek Sall, owner of the blog Life And My Finances, also recommends the snowball method of debt repayment, noting that you may be surprised by how quickly you can pay off debts this way: “You can do this!”

Make All of Your Monthly Payments

As you focus on paying off high-interest debt or your smallest debt, be sure to continue making at least the minimum monthly payments on any other debt you have.

“This is key,” Cheneler said. “Missing a payment could cost you your credit score and set you back even more.”

Pay More Than the Minimum Whenever Possible

Although you should absolutely aim to pay the minimum monthly payment, ideally, you’ll be paying more.

“If you only pay the minimum each month, it can feel that it will take forever to get out of debt,” said Ricardo Pina, founder of the personal finance blog The Modest Wallet. “If you pay a bit more — even if it’s $25 or $50 more — it will help you pay your balance faster and it can boost your morale.”

Remember That It's OK To Treat Yourself From Time to Time

Even if you’re serious about paying off debt, that doesn’t mean you need to live off ramen noodles and never leave the house.

“Don’t forget to budget at least a small amount for ‘fun stuff,'” Barker said. “It’s going to take a while to pay off your debt, so letting you use even some of your budget to have a bit of fun makes it far more likely you’ll stick with it.”

More From GOBankingRates

Are You Spending More Than the Average American on 25 Everyday Items?

Guns and 32 Other Things You Definitely Do NOT Need To Buy During the Coronavirus Pandemic

Gabrielle Olya contributed to the reporting for this article.

This article originally appeared on GOBankingRates.com: How To Manage All the Extra Debt You Piled Up in 2020