Yahoo Finance

Yahoo Finance Can LiCo Energy Metals (CVE:LIC) Afford To Invest In Growth?

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

So, the natural question for LiCo Energy Metals (CVE:LIC) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

Check out our latest analysis for LiCo Energy Metals

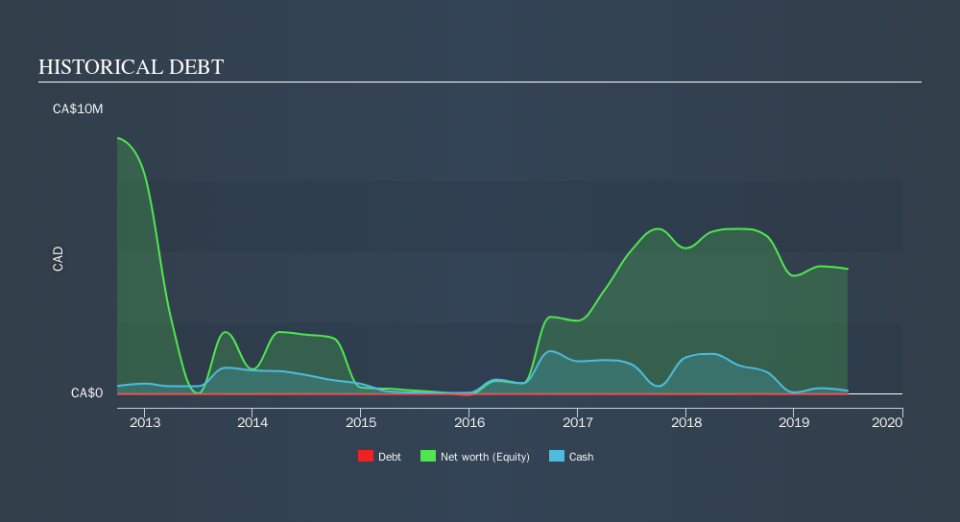

When Might LiCo Energy Metals Run Out Of Money?

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. In June 2019, LiCo Energy Metals had CA$108k in cash, and was debt-free. Importantly, its cash burn was CA$1.4m over the trailing twelve months. Therefore, from June 2019 it seems to us it had less than two months of cash runway. It's extremely surprising to us that the company has allowed its cash runway to get that short! Depicted below, you can see how its cash holdings have changed over time.

How Is LiCo Energy Metals's Cash Burn Changing Over Time?

Because LiCo Energy Metals isn't currently generating revenue, we consider it an early-stage business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. The 67% reduction in its cash burn over the last twelve months could be interpreted as a sign that management are worried about running out of cash. LiCo Energy Metals makes us a little nervous due to its lack of substantial operating revenue. So we'd generally prefer stocks from this list of stocks that have analysts forecasting growth.

How Hard Would It Be For LiCo Energy Metals To Raise More Cash For Growth?

There's no doubt LiCo Energy Metals's rapidly reducing cash burn brings comfort, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund further growth. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

LiCo Energy Metals has a market capitalisation of CA$963k and burnt through CA$1.4m last year, which is 144% of the company's market value. Given just how high that expenditure is, relative to the company's market value, we think there's an elevated risk of funding distress, and we would be very nervous about holding the stock.

Is LiCo Energy Metals's Cash Burn A Worry?

As you can probably tell by now, we're rather concerned about LiCo Energy Metals's cash burn. In particular, we think its cash runway suggests it isn't in a good position to keep funding growth. But the silver lining was its cash burn reduction, which was encouraging. Looking at the metrics in this article all together, we consider its cash burn situation to be rather dangerous, and likely to cost shareholders one way or the other. When you don't have traditional metrics like earnings per share and free cash flow to value a company, many are extra motivated to consider qualitative factors such as whether insiders are buying or selling shares. Please Note: LiCo Energy Metals insiders have been trading shares, according to our data. Click here to check whether insiders have been buying or selling.

Of course LiCo Energy Metals may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.