Yahoo Finance

Yahoo Finance Is Lattice Semiconductor's (NASDAQ:LSCC) 228% Share Price Increase Well Justified?

Unfortunately, investing is risky - companies can and do go bankrupt. On the other hand, if you find a high quality business to buy (at the right price) you can more than double your money! For example, the Lattice Semiconductor Corporation (NASDAQ:LSCC) share price has soared 228% in the last year. Most would be very happy with that, especially in just one year! And in the last week the share price has popped 9.4%. This could be related to the recent financial results, released less than a week ago -- you can catch up on the most recent data by reading our company report. Looking back further, the stock price is 209% higher than it was three years ago.

View our latest analysis for Lattice Semiconductor

We don't think that Lattice Semiconductor's modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. Generally speaking, we'd consider a stock like this alongside loss-making companies, simply because the quantum of the profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

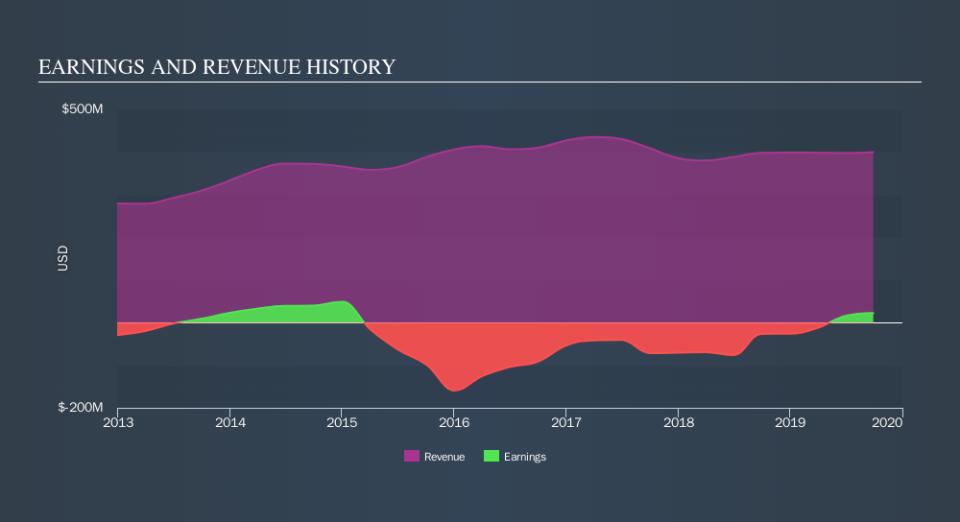

Lattice Semiconductor grew its revenue by 0.5% last year. That's not great considering the company is losing money. In contrast, the share price took off during the year, gaining 228%. The business will need a lot more growth to justify that increase. It's quite likely that the market is considering other factors, not just revenue growth.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We like that insiders have been buying shares in the last twelve months. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. This free report showing analyst forecasts should help you form a view on Lattice Semiconductor

A Different Perspective

We're pleased to report that Lattice Semiconductor shareholders have received a total shareholder return of 228% over one year. That gain is better than the annual TSR over five years, which is 24%. Therefore it seems like sentiment around the company has been positive lately. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. Investors who like to make money usually check up on insider purchases, such as the price paid, and total amount bought. You can find out about the insider purchases of Lattice Semiconductor by clicking this link.

Lattice Semiconductor is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.