Yahoo Finance

Yahoo Finance Key Factors to Impact Essex Property's (ESS) Q1 Earnings

Essex Property Trust, Inc. ESS is scheduled to report first-quarter 2020 earnings on May 6, after market close. The company’s performance will likely display year-over-year growth in funds from operations (FFO) per share and revenues.

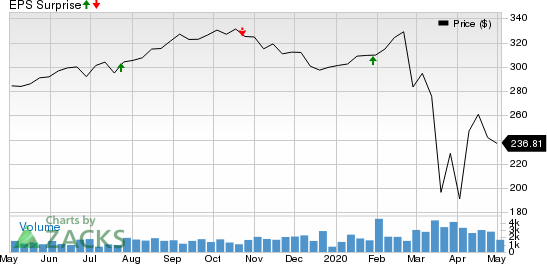

In the last reported quarter, this San Mateo, CA-based residential real estate investment trust (REIT) reported a positive surprise of 0.88% in terms of FFO per share. Results reflected solid net operating income from its communities on high occupancy level.

Over the trailing four quarters, the company beat the Zacks Consensus Estimate on three occasions and missed in the other, the average beat being 1.00%. This is depicted in the graph below:

Essex Property Trust, Inc. Price and EPS Surprise

Essex Property Trust, Inc. price-eps-surprise | Essex Property Trust, Inc. Quote

Let’s see how things have shaped up for this announcement.

Factors at Play

The first quarter had commenced on a positive note with resilient economy and decent job-market strength, though the second half of the period was jeopardized by the coronavirus pandemic.

Usually, demand for apartments slows down during the colder months as renters usually prefer less to move in winters. However, per a report from real estate technology and analytics firm RealPage, the U.S. apartment rental market’s performance in February was steady, with national apartment occupancy in the month remaining at 95.5%, in line with January’s and up 30 basis points (bps) from the year-ago tally. Rent growth of 2.9% was also in line with the three-year average.

With a solid balance sheet, Essex Property is likely to leverage on favorable demographic trends and household formation in its markets. Substantial exposure to the West Coast market, which is home to several innovation and technology companies, is anticipated to have provided ample scope to bolster its top-line growth in the quarter under review.

The region has been witnessing higher median household incomes and increased percentage of renters than owners. Further, transition from renter to homeowner is difficult in its markets due to high cost of homeownership. These are likely to have favorably impacted rental-housing demand during the period under consideration.

As such, the Zacks Consensus Estimate of $383.2 million for first-quarter revenues indicates a 7.6% improvement, year on year. In addition, the company had earlier estimated core FFO per share of $3.36-$3.46 for the quarter. The Zacks Consensus Estimate for the same is currently pinned at $3.42. It reflects 5.9% growth from the prior-year quarter’s reported tally.

Moreover, Essex Property maintains a solid balance sheet and enjoys financial flexibility. As of Jan 27, 2020, the company had $725 million in undrawn capacity on its unsecured credit facilities. This healthy financial position is likely to have helped the company strengthen and expand its business.

The company is also focused on providing its residents with convenience and customer service through paperless leasing, mobile maintenance accessibility, and smart-home technologies, and has been implementing several platform investments in the first quarter that are aimed at maximizing efficiency and growth and enhance sustainability.

However, new supply of apartment properties was elevated in the first quarter in a number of the company’s markets. This high supply is a concern because it curtails landlords’ ability to command more rent, results in lesser absorption and leads to increased concession activities. Additionally, in this seasonally-slower demand period, occupancy and rent growth are likely to have been limited.

In addition to the above, Essex Property’s activities during the January-March period were inadequate to gain analyst confidence. The Zacks Consensus Estimate for the quarterly FFO per share for remained unchanged in the past month.

Here is what our quantitative model predicts:

Our proven model does not conclusively predict a positive surprise in terms of FFO per share for Essex Property this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of a FFO beat. But that’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Essex Property currently carries a Zacks Rank #3 and has an Earnings ESP of -0.48%.

Stocks That Warrant a Look

Here are a few stocks in the REIT sector that you may want to consider, as our model shows that these have the right combination of elements to report a positive surprise this quarter:

SBA Communications Corporation SBAC, set to report quarterly numbers on May 5, has an Earnings ESP of +0.67% and carries a Zacks Rank of 3 currently. You can see the complete list of today’s Zacks #1 Rank stocks here.

Extra Space Storage Inc. EXR, slated to release first-quarter earnings on May 6, has an Earnings ESP of +0.21% and carries a Zacks Rank of 3 at present.

Americold Realty Trust COLD, scheduled to announce earnings results on May 7, has an Earnings ESP of +9.74% and currently holds a Zacks Rank #3.

Note: Anything related to earnings presented in this write-up represent funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Looking for Stocks with Skyrocketing Upside?

Zacks has just released a Special Report on the booming investment opportunities of legal marijuana.

Ignited by new referendums and legislation, this industry is expected to blast from an already robust $6.7 billion to $20.2 billion in 2021. Early investors stand to make a killing, but you have to be ready to act and know just where to look.

See the pot trades we're targeting>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Essex Property Trust, Inc. (ESS) : Free Stock Analysis Report

SBA Communications Corporation (SBAC) : Free Stock Analysis Report

Extra Space Storage Inc (EXR) : Free Stock Analysis Report

Americold Realty Trust (COLD) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research