Yahoo Finance

Yahoo Finance Itau Unibanco (ITUB) Rides on Strategic Buyouts Amid High Costs

Itaú Unibanco Holding S.A. ITUB is well-poised for growth, backed by strength in the asset management and investment banking units. The company is focused on expanding its footprint globally through strategic acquisitions. However, a rise in expenses and weak credit quality remain near-term concerns.

The bank has recorded revenue growth over the years, driven by increased commissions and fees as well as strong performance in insurance operations. The rise was primarily due to an increase in asset management, credit operations and guarantees provided, as well as credit and debit cards. Given the company's dominant position in the asset management and investment banking sectors in Latin America, along with growth opportunities in the insurance market, the bank is well-positioned to sustain and enhance its revenue growth in the coming periods.

The bank has been focused on growing inorganically in Brazil and abroad. In 2022, the company acquired an 11.4% equity stake in XP Inc. for R$8 billion. Further, it acquired Ideal Holding to bolster its investment ecosystem and completed the first phase of the deal on Mar 31, 2023. The transaction is set to be carried out in two phases over five years. In March 2024, Itaú Unibanco completed the acquisition of ZUP IT. This strategic move will bolster the bank's efforts in digital transformation, enabling the development of advanced digital projects and the delivery of new functionalities and digital products to its customers. Thus, such inorganic efforts to diversify its product mix are expected to support its top line in the upcoming quarters.

Itau Unibanco has maintained a strong total credit portfolio. It witnessed a CAGR of 13% over the last four years (2019-2023), with the uptrend continuing in the first quarter of 2024. The company is actively trying to reduce its loan portfolio exposure in higher volatile segments. Such efforts are likely to further strengthen its credit portfolio in the future.

As of Mar 31, 2024, the bank’s deposit is R$965.35 billion, which showcases its strong funding base. Its times' interest ratio of 1.5 in the first quarter of 2024 increased on a year-over-year basis. Hence, ITUB is less likely to default on interest and debt repayments if the economic situation worsens. A robust funding position helps it maintain a healthy credit portfolio (including financial guarantees provided and corporate securities).

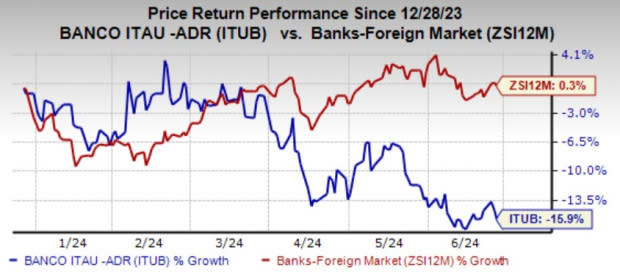

Shares of the company have plunged 15.9% on the NYSE over the past six months against the industry’s growth of 0.3%.

Image Source: Zacks Investment Research

ITUB currently carries a Zacks Rank #3 (Hold).

However, an escalating expense base remains a concern for the ITUB. The company’s ongoing investment in digital transformation and client centricity will likely keep the expenses elevated and may hinder the bottom-line growth in the near term. Management projects non-interest expenses to grow 4-7% in 2024.

Itau Unibanco has exhibited deterioration in its credit quality in the recent past. Its non-performing loan ratio and the cost of credit charges have remained elevated over the last few years. The metric is expected to remain elevated in the near term, owing to the worsening economic outlook and recessionary fears, which are likely to affect credit quality in the near term.

Stocks to Consider

Some better-ranked bank stocks are Banco Macro S.A. BMA and KBC Group NV KBCSY.

Banco Macro’s earnings estimates for 2024 have been revised 29.6% upward in the past 60 days. The company’s shares have surged 94.3% over the past six months. At present, BMA sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

KBC Group NV’s 2024 earnings estimates have revised 50.8% upward in the past 60 days. The stock has gained 8.7% over the past six months. Currently, KBCSY sports a Zacks Rank #1.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Itau Unibanco Holding S.A. (ITUB) : Free Stock Analysis Report

Macro Bank Inc. (BMA) : Free Stock Analysis Report

KBC Group SA (KBCSY) : Free Stock Analysis Report