Yahoo Finance

Yahoo Finance How Should Investors Feel About Actual Experience plc's (LON:ACT) CEO Pay?

Dave Page is the CEO of Actual Experience plc (LON:ACT). This analysis aims first to contrast CEO compensation with other companies that have similar market capitalization. Then we'll look at a snap shot of the business growth. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. This method should give us information to assess how appropriately the company pays the CEO.

Check out our latest analysis for Actual Experience

How Does Dave Page's Compensation Compare With Similar Sized Companies?

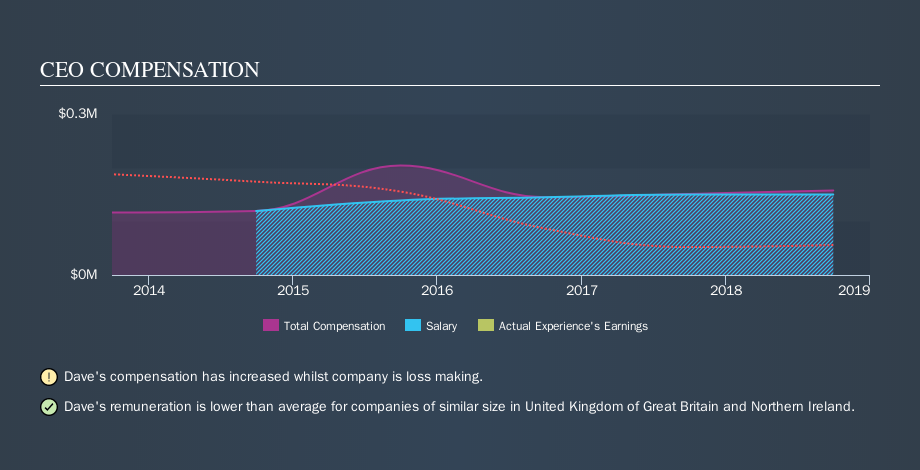

According to our data, Actual Experience plc has a market capitalization of UK£53m, and pays its CEO total annual compensation worth UK£158k. (This number is for the twelve months until September 2018). It is worth noting that the CEO compensation consists almost entirely of the salary, worth UK£150k. We looked at a group of companies with market capitalizations under UK£160m, and the median CEO total compensation was UK£255k.

A first glance this seems like a real positive for shareholders, since Dave Page is paid less than the average total compensation paid by similar sized companies. While this is a good thing, you'll need to understand the business better before you can form an opinion.

You can see, below, how CEO compensation at Actual Experience has changed over time.

Is Actual Experience plc Growing?

On average over the last three years, Actual Experience plc has shrunk earnings per share by 5.8% each year (measured with a line of best fit). In the last year, its revenue is up 305%.

Investors should note that, over three years, earnings per share are down. On the other hand, the strong revenue growth suggests the business is growing. These two metric are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. We don't have analyst forecasts, but you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Actual Experience plc Been A Good Investment?

With a three year total loss of 57%, Actual Experience plc would certainly have some dissatisfied shareholders. So shareholders would probably think the company shouldn't be too generous with CEO compensation.

In Summary...

It appears that Actual Experience plc remunerates its CEO below most similar sized companies.

It's well worth noting that while Dave Page is paid less than most company leaders (at similar sized companies), performance has been somewhat uninspiring, and total returns have been lacking. I am not concerned by the CEO compensation, but it would be good to see improved performance before pay increases. Whatever your view on compensation, you might want to check if insiders are buying or selling Actual Experience shares (free trial).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.