Yahoo Finance

Yahoo Finance How to invest for the next recession

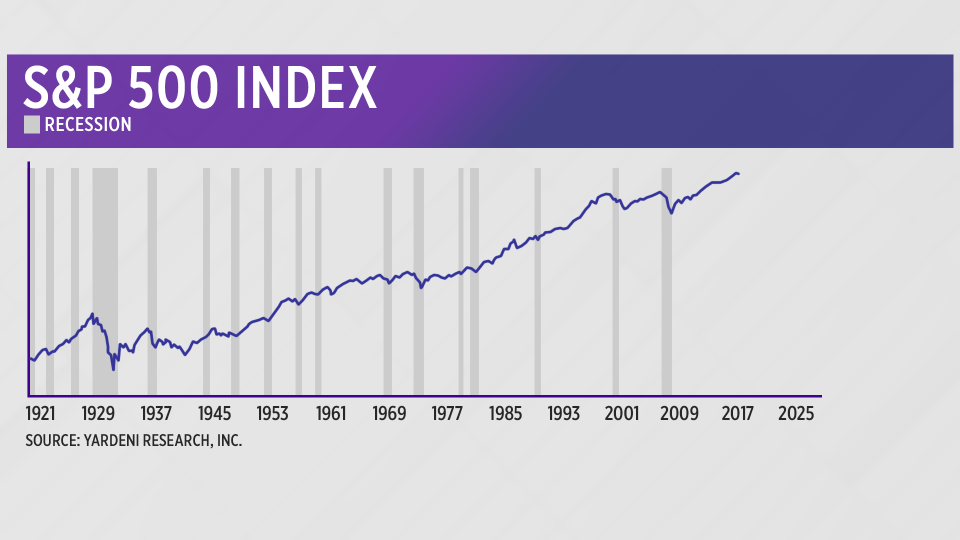

The last nine years have been great for stock investors, with the S&P 500 up 300% since early 2009.

Expect the next nine years to be more turbulent.

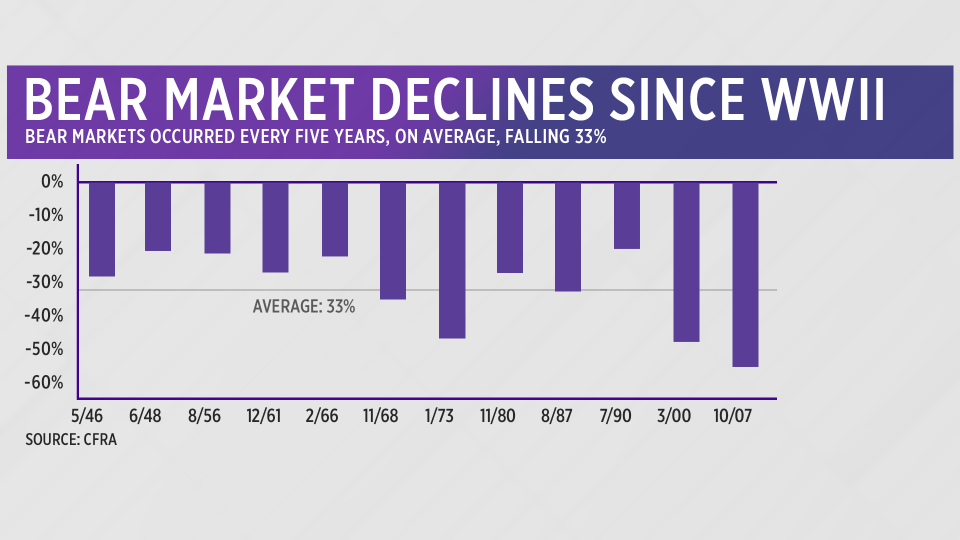

Economists don’t think a recession is imminent, but some think the economy could enter a downturn by late 2019 or 2020. And recessions usually trigger a sharp drop in stock values. Recessions since 1945 have lasted 11 months on average, while the average bear market in stocks has lasted 14 months, according to investing firm CFRA. The average price drop in the S&P 500 during a bear market is 33%.

Some investors are starting to anticipate the inevitable bear market. A recent poll of economists by investing giant PIMCO found that “a US recession over the next three to five years has now become consensus—even though markets do not seem to be pricing in this risk.” PIMCO thinks the next recession will be “shallower and longer” than normal, with steep losses in some asset classes and surprising resilience in others.

To help Americans survive the next recession, Yahoo Finance is publishing a series of stories on how to take advantage of good times now to prepare for leaner times coming. No, we’re not rooting for economic hardship, as comeuppance for President Trump, as some of his backers may believe. We’re simply forecasting the obvious: The current economic expansion just entered its 10th year, which is twice the average length since 1945. We’re due for a recession.

[Check out our Next-Recession Survival Guide.]

This installment, on investing, will outline how various asset classes typically perform during a downturn, along with strategies for minimizing the pain and capitalizing on bargains. Sound investing is highly personalized and depends on age, life circumstances, risk tolerance and many other factors. So this guide does not constitute professional investing advice. But anticipating market reaction to a downturn can help investors figure out how to protect their assets based on their own personal needs. Younger investors with a long time horizon may choose to do nothing at all, while those closer to retirement age may want to make sure their principal doesn’t take a hit.

The first thing to know about the next recession is that it won’t be quite like the last one, which involved a huge housing bust and a terrifying financial crash. While some analysts think stocks are overvalued today, there are few signs now of the type of giant imbalances that toppled Lehman Brothers and other financial institutions in 2008. Safeguards put in place after the 2008 crash also put limits on excessive debt and other factors that can cause a crash.

There are still risks, however. Corporate debt is at record levels, and while default rates are low now, they could spike amid a confluence of adverse factors, such as rising interest rates, slowing consumer spending and tightening lending standards among banks. “The liquidity faucet gets turned off pretty quickly in a recession,” says finance professor Edward Altman of New York University’s Stern School of Business, an expert on corporate bankruptcy. “The default rate is going to go up, and go up a lot. It could get very ugly.” The most vulnerable industries are those with the lowest-quality debt, which include energy, retail and health care.

[See the biggest risks for workers when the next recession hits.]

US banks are much healthier than they were leading up to the last recession, and they can weather a spate of defaults and a modest recession. European banks, however, have not fully recovered from the last meltdown, and remain vulnerable, especially with Britain leaving the European Union and other strains weakening the EU. Banks in China, now the world’s second-biggest economy, also have high levels of bad debt on their books, and that could matter more than it did a decade ago. “China was a non-factor before,” says Altman. “Now they’re a big factor.”

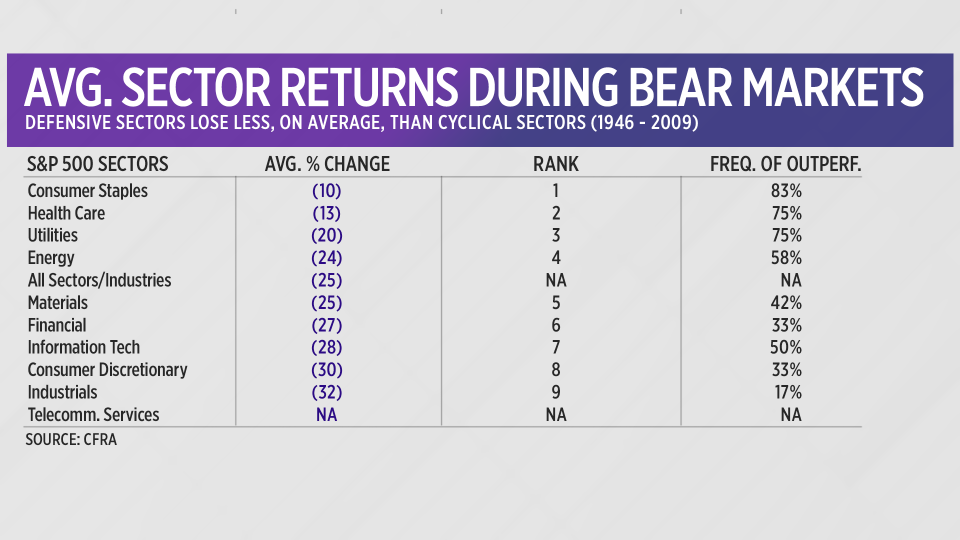

If defaults, layoffs or bad economic data give markets a whiff of recession, stocks could sell off rapidly, with little spared as investors shed risky assets for safer ones. “There are very few places to hide in a bear market,” says Sam Stovall of CFRA. “Once you scream bear market, everything goes red except for bonds, the U.S. dollar and most times, gold.” So-called defensive sectors such as consumer staples and utilities tend to hold up better than most other sectors—but they still drop. Since 1945, bear-market declines have averaged double-digits in every sector, according to CFRA.

[See what’s likely to cause the next recession.]

The riskiest and safest investments in a recession

PIMCO thinks the riskiest investments during the next recession include companies with high-yield or junk-rated debt, which will be most vulnerable to default as credit tightens. Safer: Short-term bonds such as highly rated corporates or US Treasuries. PIMCO also thinks tougher regulation during the last decade could shield industries that were highly vulnerable the last time around. “Sectors that have seen a significant increase in regulation, including commercial real estate and the financial sector as well as housing, will likely demonstrate resilience,” PIMCO analysts wrote in a recent report.

Cash is perhaps the most obvious place to put your money during a bear market, since it protects your principal and leaves “dry powder” for buying when you feel the bear market may be close to a bottom. But there are risks with cash, too. First, nobody knows when the next recession will start and end, so you could miss out on market gains by liquidating too soon—or get crushed by liquidating too late. And while your money’s in cash, you’re still losing out to inflation.

As for gold, its reputation as a store of value in chaotic times is not quite correct. Gold prices, for instance, fell by about 25% during the first couple months of the financial crash in 2008. Gold recovered faster than the stock market did after that, but it still subjected holders to a nauseating, if brief, nosedive. Exchange-traded funds based on the price of gold, such as SPDR Gold Shares (GLD), performed similarly.

Investing pros typically recommend a blend of assets split among riskier stocks, safer bonds, cash and precious metals, based on your risk profile. In a bear market environment, it’s obviously prudent to shift your mix away from risk in favor of safety. But timing is everything, and the old maxim—don’t try to time the market—applies in both good times and bad.

One way to mitigate timing risk is to move money out of riskier assets into safer ones on a consistent schedule that’s not influenced by market movements, similar to the dollar-cost averaging strategy—but in reverse. “Every month, take out a portion of your cyclical investments and place them into more defensive areas like consumer staples, utilities, cash, and gold,” says Stovall.

Boring bonds

Peter Kenny, co-founder of market analytics firm Kenny & Company, suggests harvesting profits from investments that have treated you best. “Take some money off the table, especially in funds or equities that have given you outperformance,” he says. “If you’re up 100%, take 50% off the table. It’s going to feel counterintuitive. That’s why so many people get hung up on this. They’ve made money and they love looking at that symbol. That attachment should never be tolerated.”

Brokerages such as Vanguard, Fidelity, Schwab and Ameritrade offer a variety of mutual and exchange-traded bond funds that provide the type of haven many investors seek during a bear market. A short-term bond fund holding high-quality securities tends to be safest. “Short-term bond funds tend to be safer, because the range of yields in a short-term fund is much smaller,” says Karen Wallace, a senior editor at Morningstar. “They’ll probably yield a little bit more than cash.” Still, keep in mind: bond funds can lose money.

One strategy is to gradually move money into a fund that tracks the Bloomberg Barclays US aggregate bond index, a group of highly rated government and corporate bonds. The Barclays “agg,” as its known, did fall in value for short periods of time during the 2008 financial shock. But overall, it rose 6.8% in 2007, 4.3% in 2008 and 6.4% in 2009. The S&P 500, by comparison, rose 3.5% in 2007, plunged 38.5% in 2008 and recovered 23.4% in 2009. The boring bond fund insured against panic.

So if you do survive the next recession with principal intact, when should you start to bargain-shop? And for what? The answer, again, depends largely on each investor’s ability to tolerate risk. But trading patterns during prior recoveries provide guidance.

“The recovery is the mirror image of the decline,” says Stovall. “Cyclicals tend to do best because they did the worst on the way down.” He also points out that markets tend to recover very quickly once investors think the bottom is near, with everybody trying to grab bargains. “In the first 40 days of a new bull market, we tend to recover 25% of what we lost in the entire bear market.”

It’s hard to overstate the difficulty of timing the market, and guessing when the recession is likely to end. Investors thought they were out of the woods when a short recession and bear market ended in the middle of 1980, for instance – but a new recession started a year later, with stocks falling further, for longer, during the second downturn. So shifting from safer assets to riskier ones, if that’s the way you choose to go, is best done incrementally on a consistent schedule.

There may be bargains other than stocks as the next recession comes and goes. Home values have been rising steadily since 2012, and are now at new record highs, leaving many buyers priced out. But home values often fall during a recession—which could be just the break home buyers are looking for. “It may be an opportunity for a younger generation that has been completely unable to access the housing market,” says Peter Kenny. We’ll have more on that in a future installment of this series. Until then, protect your principal.

Confidential tip line: rickjnewman@yahoo.com. Click here to get Rick’s stories by email.

Read more:

Rick Newman is the author of four books, including “Rebounders: How Winners Pivot from Setback to Success.” Follow him on Twitter: @rickjnewman

Follow Yahoo Finance on Facebook, Twitter, Instagram, and LinkedIn