Yahoo Finance

Yahoo Finance Introducing Eagle Graphite (CVE:EGA), The Stock That Tanked 70%

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

It's not possible to invest over long periods without making some bad investments. But you have a problem if you face massive losses more than once in a while. So take a moment to sympathize with the long term shareholders of Eagle Graphite Incorporated (CVE:EGA), who have seen the share price tank a massive 70% over a three year period. That'd be enough to cause even the strongest minds some disquiet. And the ride hasn't got any smoother in recent times over the last year, with the price 70% lower in that time. Unfortunately the share price momentum is still quite negative, with prices down 16% in thirty days.

See our latest analysis for Eagle Graphite

Eagle Graphite hasn't yet reported any revenue yet, so it's as much a business idea as an actual business. This state of affairs suggests that venture capitalists won't provide funds on attractive terms. So it seems shareholders are too busy dreaming about the progress to come than dwelling on the current (lack of) revenue. It seems likely some shareholders believe that Eagle Graphite will find or develop a valuable new mine before too long.

We think companies that have neither significant revenues nor profits are pretty high risk. There is almost always a chance they will need to raise more capital, and their progress - and share price - will dictate how dilutive that is to current holders. While some such companies go on to make revenue, profits, and generate value, others get hyped up by hopeful naifs before eventually going bankrupt. It certainly is a dangerous place to invest, as Eagle Graphite investors might realise.

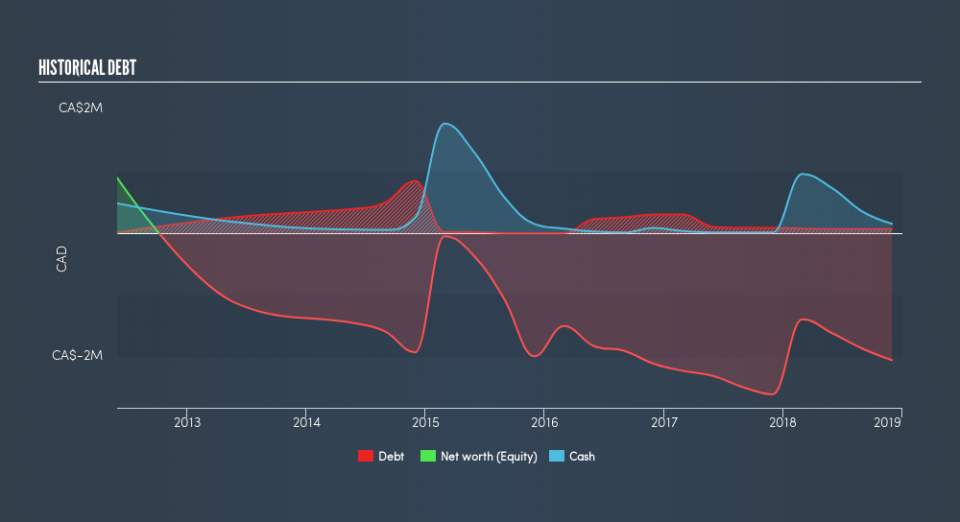

Our data indicates that Eagle Graphite had net debt of CA$2,535,025 when it last reported in November 2018. That puts it in the highest risk category, according to our analysis. But since the share price has dived -33% per year, over 3 years, it looks like some investors think it's time to abandon ship, so to speak. You can click on the image below to see (in greater detail) how Eagle Graphite's cash levels have changed over time.

It can be extremely risky to invest in a company that doesn't even have revenue. There's no way to know its value easily. Given that situation, would you be concerned if it turned out insiders were relentlessly selling stock? I would feel more nervous about the company if that were so. It only takes a moment for you to check whether we have identified any insider sales recently.

A Different Perspective

The last twelve months weren't great for Eagle Graphite shares, which cost holders 70%, while the market was up about 6.3%. Of course the long term matters more than the short term, and even great stocks will sometimes have a poor year. The three-year loss of 33% per year isn't as bad as the last twelve months, suggesting that the company has not been able to convince the market it has solved its problems. We would be wary of buying into a company with unsolved problems, although some investors will buy into struggling stocks if they believe the price is sufficiently attractive. Shareholders might want to examine this detailed historical graph of past earnings, revenue and cash flow.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on CA exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.