Yahoo Finance

Yahoo Finance The Huifu Payment (HKG:1806) Share Price Is Down 14% So Some Shareholders Are Getting Worried

Passive investing in an index fund is a good way to ensure your own returns roughly match the overall market. When you buy individual stocks, you can make higher profits, but you also face the risk of under-performance. Investors in Huifu Payment Limited (HKG:1806) have tasted that bitter downside in the last year, as the share price dropped 14%. That's disappointing when you consider the market returned 3.4%. Because Huifu Payment hasn't been listed for many years, the market is still learning about how the business performs. On top of that, the share price has dropped a further 9.3% in a month. We do note, however, that the broader market is down 3.8% in that period, and this may have weighed on the share price.

See our latest analysis for Huifu Payment

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

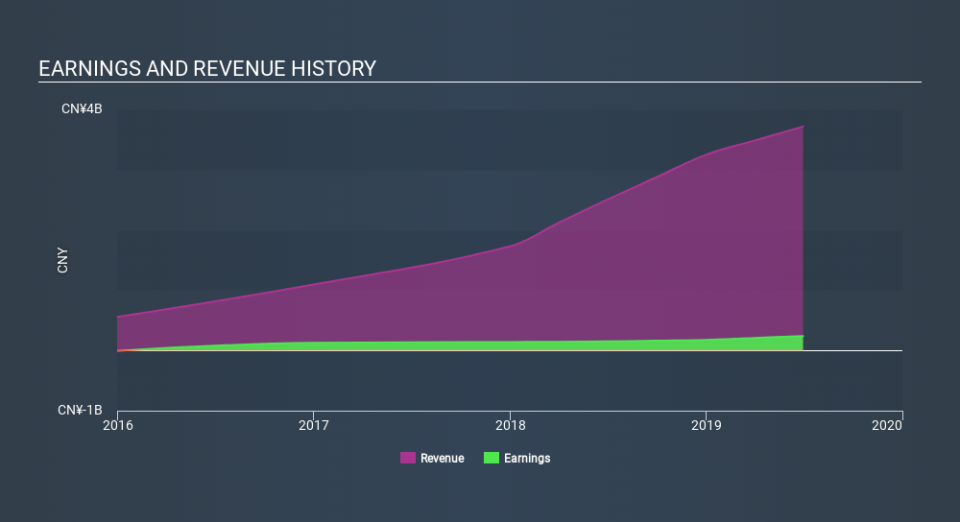

During the unfortunate twelve months during which the Huifu Payment share price fell, it actually saw its earnings per share (EPS) improve by 13%. It could be that the share price was previously over-hyped.

It's fair to say that the share price does not seem to be reflecting the EPS growth. So it's easy to justify a look at some other metrics.

Huifu Payment's revenue is actually up 49% over the last year. Since the fundamental metrics don't readily explain the share price drop, there might be an opportunity if the market has overreacted.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We know that Huifu Payment has improved its bottom line lately, but what does the future have in store? So it makes a lot of sense to check out what analysts think Huifu Payment will earn in the future (free profit forecasts).

A Different Perspective

While Huifu Payment shareholders are down 14% for the year, the market itself is up 3.4%. While the aim is to do better than that, it's worth recalling that even great long-term investments sometimes underperform for a year or more. With the stock down 8.4% over the last three months, the market doesn't seem to believe that the company has solved all its problems. Given the relatively short history of this stock, we'd remain pretty wary until we see some strong business performance. Before forming an opinion on Huifu Payment you might want to consider these 3 valuation metrics.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on HK exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.