Yahoo Finance

Yahoo Finance Home prices, sales slide in June as rising rates put more buyers on sidelines

Toronto real-estate agent Harry Sarvaiya was ready for higher interest rates, but not like this.

“I think the intention was shock,” Sarvaiya said a couple of days after the Bank of Canada raised the benchmark a full percentage point, the biggest increase since 1998. “In real estate, people didn’t expect it.”

Housing is probably the industry most sensitive to interest rates. That’s helpful when the economy is in trouble. The central bank can stoke demand quickly by dropping interest rates in the knowledge the Canadians will rush to buy houses — and then renovate them and fill them with big-ticket items such as appliances and furniture. Service providers such as banks, brokers, contractors, and movers all benefit.

If prices keep rising, the broader economy benefits, because households feel richer, something economists call the “wealth effect.”

Canada’s economic growth over the past dozen years has depended to a great degree on such wealth effects. But the central bank’s job isn’t goosing the housing market; its mission is to control inflation, which accelerated to nearly eight per cent in May.

Bank of Canada Governor Tiff Macklem has now raised borrowing costs more in the past four months than his predecessors did during the decade between the end of the Great Recession and the start of the pandemic. The effect on the housing market has been just as immediate as when borrowing costs were dropped to nearly zero, but nowhere near as pleasant for the real-estate industry and aspiring buyers and sellers.

“We’ve had everything happen to us in the past couple weeks,” said Joe Baglieri, broker at Re/Max Realtron Property Shop in Markham, Ont. “We’ve had deals fall through, we’ve had renegotiations happen.”

Baglieri said that real estate is more of a long-term game and anyone involved in it has to expect cooler periods. The problem is, borrowing costs have been so low for so long, many households have forgotten what it’s like when interest rates bite. Geoff Morgan, a brand marketer from Toronto, said his bank raised his variable mortgage rate within hours of the Bank of Canada’s shock policy announcement on July 13, while his variable-rate savings account barely budged.

“I’ve asked my bank for an explanation,” Morgan said. “They tell me they offer competitive rates.”

The impact goes beyond the strain for current home owners. Home sales and prices continue to slide across the country, as rising mortgage costs ripple throughout the market, putting more homebuyers on the sidelines. Sarvaiya said he lost a sale on a $400,000 condo in Toronto because the buyer failed to qualify for the mortgage.

“He had the 20-per-cent down payment, but after that it’s ratios,” said Sarvaiya. “He has to qualify for prime plus two, which he would have two months back easily, and now it’s difficult to qualify.”

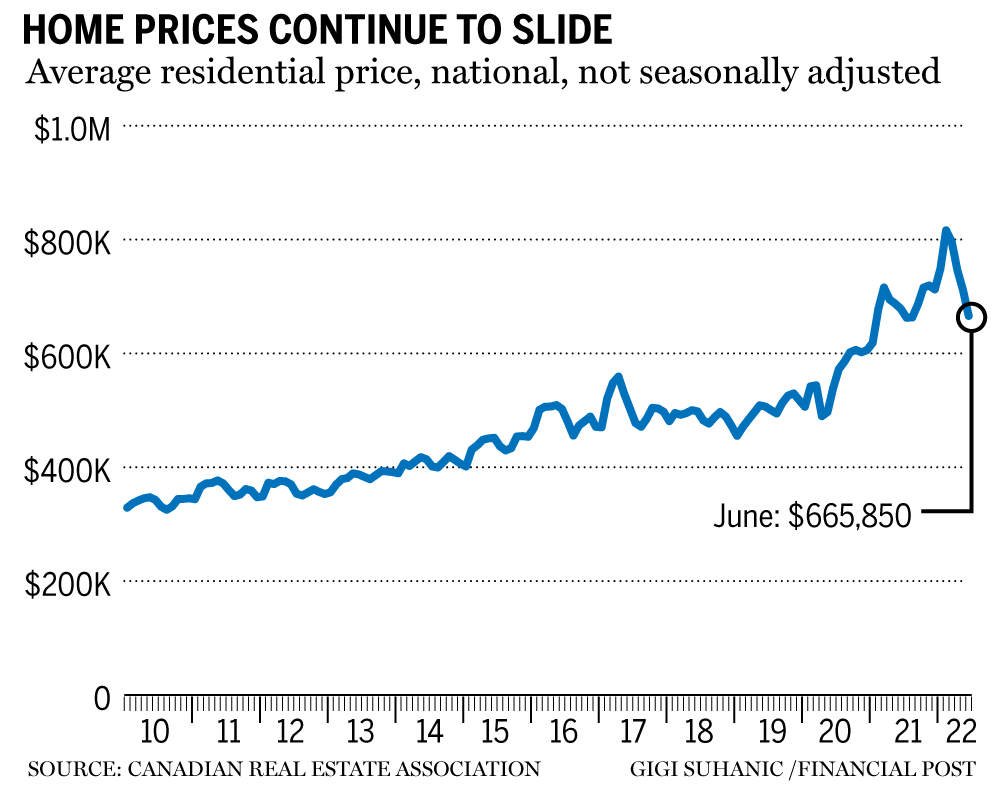

The Canadian Real Estate Association reported on July 15 that the nationwide actual, non-seasonally adjusted average price stood at $665,850 in June, slipping nearly two per cent from a year earlier and sliding six per cent from May.

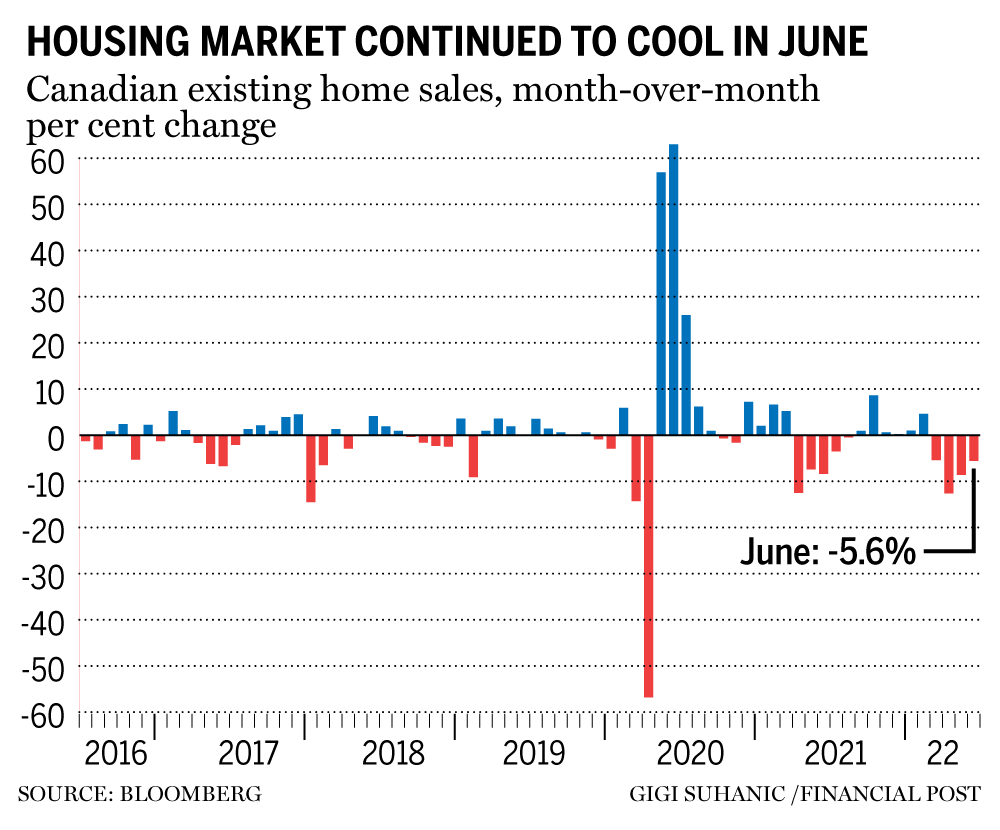

The number of homes changing hands fell 5.6 per cent month-over-month in June and fell approximately 24 per cent from the June record set in 2021. The association noted that the declines were not as large as the drops seen in April and May.

“Sales activity continues to slow in the face of rising interest rates and uncertainty,” Jill Oudil, chair of CREA, in a press release accompanying the data. “The cost of borrowing has overtaken supply as the dominant factor affecting housing markets at the moment, but the supply issue has not gone away.”

Lauren Haw, chief executive officer at Zoocasa Realty Inc., told Financial Post’s Larysa Harapyn in a July 12 interview that more Canadians are holding off on their purchases and seeing what the Bank of Canada would do next.

“As people are saying right now, just let the dust settle before they make that big decision,” Haw said. “So that means there’s a lot of dislocation and people are just sitting on the sidelines.”

Haw added that prospective homebuyers are waiting for an indication that prices have hit the bottom before they re-enter the market.

The Bank of Canada observed in its latest quarterly report that a “sharp slowdown” in housing is “underway.” Robert Kavcic, an economist at Bank of Montreal, called the latest data the “early days of correction” in a note to clients.

“Sales have now fallen back into pre-COVID ranges and below the 10-year average for the first time since the pandemic broke out,” Kavcic wrote in a note to clients. “The period of extreme excess demand is essentially over, and we are on track for a very weak year ahead for resale volumes and prices.”

What the Bank of Canada’s full percentage point hike means for the housing market and your mortgage

'I am distraught': Jumbo rate hike adds more financial pain for some Canadians

Royal LePage cuts home price outlook ‘significantly’ on aggressive Bank of Canada rate hikes

Canadians flocked to variable-rate mortgages ahead of Bank of Canada rate hikes, CMHC says

Some are already warning that Canada is headed for a housing bust. At the same time, some of those people have been saying that for more than a decade. Christopher Alexander, president at Re/Max Canada, argued that the exuberant average price growth during the pandemic had been unsustainable and that higher interest rates will leave the market healthier.

“This is good news for buyers and sellers who need to move within the market, and ultimately, good for the real-estate professionals who serve them,” said Alexander. “A healthy market that’s appreciating in the mid- to high-single digits will allow more Canadians to engage in the market. The real challenge for consumers and the real estate industry will be the supply shortage.”

Kelsey Smith, who is looking to purchase her first home in Calgary, said house hunting and mortgage shopping has become a lot more difficult. The recent MBA graduate said she plans to avoid locking into a five-year fixed rate mortgage, even though she doesn’t relish the idea of “riding the rollercoaster” of variable rates.

“I chose to bring my price range down by $50,000 because of the current interest rates,” she said. “On the mortgage front, I’ve been having to look at changing the amortization period from 25 years to 15 years — I’ve actively been trying to MacGyver myself a way into a better deal. It’s kind of been crappy.”

Back in Toronto, Sarvaiya was bracing for a new reality. The “madness” of bids $100,000 over asking is over, he said. “There are all these houses for sale right now and nobody’s buying, even if they reduced the price because the buyer lost confidence, thinking it will be a downward spiral,” he said.

Additional reporting by Marisa Coulton, Denise Paglinawan, and Meghan Potkins.

• Email: shughes@postmedia.com | Twitter: StephHughes95