Yahoo Finance

Yahoo Finance If History Repeats

No one can tell what’s going to happen in the market, not you, not I, and indeed not Wall Street; hence it’s essential to listen to the messages the market tells you daily.

The market is so finely tuned that, in a matter of 5 trading days, its self-correcting mechanism takes hold without the need for central bank policy. One of the more undervalued market mechanisms is how quickly financial conditions loosen. From Friday a week past highs to peak fear last Friday, the bond markets shaved off a whopping 30 basis points on ten-year US yields, which sent the dollar reeling, and it provides looser financial conditions in the US market.

Also, we know the Fed is a reactionary committee, and history reminds us of the disinflationary shock from SARS that pushed the Fed into a final insurance cut in 2003. And with the Fed struggling to ignite the inflation fires, a rate cut this spring or summer is becoming the base case in quick order.

Monday Open

The markets continue to view the Wuhan virus through the lens of the SARS epidemic of 2002-03. Still, given the importance of China in the global supply chain 2020 vs. 2003, the risk might be that the market might not be alarmist enough. And by the looks of Friday’s New York session price action, where traders unanimously voted with their feet preferring to hold long volatility positions ahead of the Monday’s China post-Lunar New Year market open. The thinking is that there’s a chance Chinese “dà mà” traders hit the panic button out of the gates before the expected PBoC policy measures or the markets mean reversion algorithms kick in.

As far as China risk, it’s hard to predict if the catch-up trade trap door gap lower at the open will extend Monday, typically it does during big meltdowns. Still, history reminds us that we should be reasonably confident the Financial Stability and Development Commission, part of the People’s Bank of China, will offer support. Their new light-touch attitude, when it comes to the market’s intervention, will probably give way to the old guard heavy-handed approach, as well they will possibly instruct the so-called “national team “to hold the line of support on equity markets to ensure an orderly open.

At the time of writing, the PBoC has preannounced $170 billion in added liquidity for the Monday open. This is well beyond the band-aid fix, and if this deluge doesn’t hold risk-off at bay, we are in for a colossal beat down. In addition, the PBoC will likely intervene on the currency market, so I would expect them to layer the soothing market tiger balm on thick and heavy.

The Chinese government established the so-called “national team” of financial institutions to buy stocks with public funds directly. It also started a campaign to hunt down “financial crocodiles,” whose trading practices were blamed for numerous mainland market crashes.

So, try to ignore initial headlines around price fall at the open in China since the markets have been closed for a week as the drop is only reflecting a catching up with the broader proxy moves from last week. It’s not the earthquake at the open but rather the aftershocks that will drive risk sentiment on Monday.

But and this is a big but.

It doesn’t seem like there is much rational thinking going on given the mortality rate remains low, while comparisons and extrapolations to SARS seem questionable. However, this is a market that appears to be reasonably fragile when it comes to confidence. And without the usual stock market rally to help paper over the cracks, I suspect investors will take few chances when it comes to running risk on Monday. And they’re probably only a step away from moving into sell first ask question later mode.

SARS vs. WARS

The biggest threat to the global economy is not just because the disease spreads quickly across countries through networks related to global travel. But also, because any economic shock to China’s colossal industrial and consumption engines will spread rapidly to other countries through the increased trade and financial linkages associated with globalization.

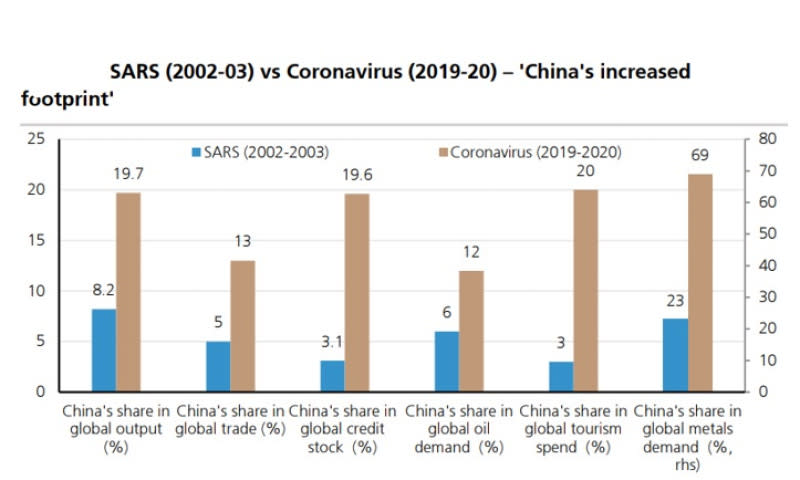

However, two reasons the coronavirus outbreak may hit the financial market harder than SARS did in 2003 are 1) consumption is now a more substantial part of China’s GDP and 2) China’s overall growth trajectory. In 2002, retail sales for 34% of nominal GDP; this share is now over 40%

While comparisons between the SARS and coronavirus are beyond tricky, for those looking to play the big rebound play, keep in mind that in 2003 the entire backdrop was completely different as most risky assets were already at the lows, not highs, after the tech bubble blow up and US recession. So, looking at the stream of rebound comparison is invalid on so many levels.

Wuhan Virus Toolbox

It’s injudicious for anyone in the market to offer any strong views on how this virus will play out. But instead, you need to come up with a reactive game plan, which I’ve tried to simplify below to get you thinking in the correct direction.

Remain focused on the daily flow of confirmed cases and when they peak

2019-nCoV Global Cases by Johns Hopkins CSEE

In the unfortunate event that the virus’s spread is not contained, the impact on the global economy will likely be much more severe than it was during the time of SARS. China’s share in the global economy and in global trade is colossally more significant by multiples than what it was 17 years ago.

Bloomberg

The ‘starting points’ on global GDP and trade growth are much weaker. Although China has policy room to accommodate a short term shock, its ability to do so is limited by structural deficiencies that prevent policy markers getting the money into the hands of those that need it the most and are probably more limited now than at the time of the previous health scares, such as SARS.

Bloomberg

Market positioning could be a concern, but I don’t want to be the alarmist. Still, according to most metrics, up until last week’s equity futures long positioning had continued to rise to new records, call volumes have surged to the highest since October 2018, and sentiment indicators are at the top of their historical band. Over the last three months, equity funds have also seen inflows of $75bn, the strongest since early 2018, with cyclical sectors being big beneficiaries, especially Tech, Financials, and Industrials. Indeed, the market’s fear factor has given way to greed, which could leave current positions precariously perched. Pullbacks of 3-5% in the S&P 500 have been typical every 2 to 3 months historically, but now we’ve stretched to about 3.5 months since October market knockdown. If a significant “Wu-Flu “risk wobble occurs, we could see more profound positioning unwinds as a pandemic panic ensues. That situation has become a real possibility.

IMM Data

There is nowhere that China’s economic influence is more on display than in Asia. The key driver of ASEAN’s steady growth over the past decade has been the rapid growth in bilateral trade with China. China has been ASEAN’s largest trading partner in the past ten years, with two-way trade reaching $292 billion in the first half of 2019. And thus, makes the rest of Asia extremely vulnerable to a China economic slowdown.

At some point this week, the market may begin to focus on a few rebound trades; however, ASEAN traders will also look at risk from two different perspectives. Economies that are tourist and service providing to China and that will not recoup lost spending – i.e., Thailand and Singapore. Both could continue to struggle for months ahead l. Whereas manufacturing and commodity exporters that could see pent-up demand rebound later in the year will probably see much of the initial rebound flow if virus fears deescalate and the transitory trade sets in.

Currency Markets

The greenback was under pressure across G10 into month-end rebalancing. USDJPY got hit the hardest, and it struggled to get back above 108.50 even on the short squeeze mini bounce into the weekend. Rebalancing isn’t solely to blame for this move – it’s a bit of a catch-up move with USTs and risk in general. Downside levels are at 107.90/107.65.

The weakest ASEAN links in the basket are the most obvious (THB and SGD), so despite paring back USD longs vs G-10 on Friday, interbank traders were flocking to those paths of least resistance. ( buying USD vs THB and SGD)

If history repeats itself as was the case in 2003, Singapore MAS could let the doves fly while the Bank of Thailand will most certainly bring forward a rate cut to ward off the damaging effects on the tourism sector. Both of which could significantly weaken those two currencies.

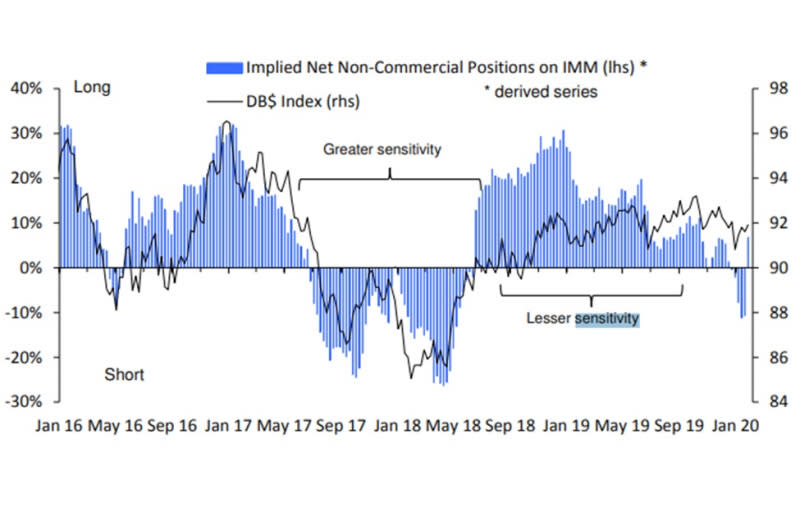

On the IMM data, and after a short five weeks being short the US Dollar, the tape indicated investors flipping aggressively back into dollar longs, as a safe-haven hedge. At the same time, total open interest declined to a 2-1/2 year low. Investors increased EUR and AUD shorts while also reducing GBP, CAD, and MXN length.

USD long position shift on the IMM

Oil markets

The Oil market has caught more than a case of the sniffles. China’s larger oil market footprint (5.7 MMB/d in 2003 vs. 13.9 MMB/d today) raises the potential for enormous demand devastation given Chinas current oil demand profile in comparison to the SARS epidemic era.

According to Deutsche Bank, “Early estimates of the impact on oil demand growth are around 100 kb/d, raising this year’s oversupply to 1 MMB/d. This assumes the disruption is limited to the first quarter and suggests Brent prices may remain USD 60/bbl. below.”

Although oil bulls are hoping on a wing and a prayer that an early OPEC meeting (February instead of 5 March) raises the prospect of greater supply discipline, but this is by no means certain given OPEC’s current low level of output and the general consensus among OPEC ministers who believe the market impact will be smaller than the current level of market fear priced into the equation.

Regardless of the outcome of the 2019-nCoV epidemic, oil prices may have further to fall and will generally remain under downside pressure due to the toxic combination of extreme demand destruction and excess non-OPEC supply.

Gold markets

Gold gains on massive demand as a hedge against coronavirus concerns; in a position build-up that is now expected to challenge USD1,600/oz near term. Gold continues to benefit from the need for risk-off positioning as investor sentiment tanks and the economic devastation reality check sets in as equity market traders have pivoted from buying the dip to selling the fact.

Gold propped up as US equities weakened, and yields fell, with the yield on the US 10-year Treasury easing to 1.502%. But just as significant of short term traders, as was the case for the disinflationary shock from SARS, that pushed the Fed to a final “insurance” cut in 2003, with the Fed struggling to ignite the inflationary flame, a rate cut this spring is quickly becoming the market base case and extremely bullish for gold.

For now, the weaker US dollar is factoring positively into the equation as the market brings forward a Fed interest rate cut, which should weaken the US dollar and provide a positive knock-on fillip for gold prices.

Gold has clearly benefited from the turmoil emanating from the coronavirus and the Iran conflict earlier in the month. However, if both tails fade gold positioning could be a bit of a problem, and with physical demand remaining weak, traders will need to be extremely alert to plateaus in virus headcount or mortality rates on a daily basis.

Gold positioning in ounce terms (ETF, Net Managed Money, Tocom non-commercial)

The week ahead

The other risk here is that all the bandwidth is being taken up by the virus, while there are plenty of other issues to consider.

A new NBC/WSJ poll puts Bernie Sanders in the lead, the first time he has been at the top of a national survey (even if statistically tied). Sanders leads on 27%, Joe Biden is on 26%, Elizabeth Warren is on 15%, and Michael Bloomberg has crept up into the fourth spot with 9%. This should be a significant risk for both the USD and US equities if this trend continues and Trump’s popularity wanes in the head to head polls with Sanders.

Buckle up for a US economic data deluge

This week’s economic docket includes the granddaddy of data releases, the January employment report (Friday), which will take on a heightened level of importance given the at the markets are now in the process of pricing in Fed rates cuts sooner than later. As well, we have the January manufacturing ISM (49.8 vs. 47.8) along with Wednesday’s non-manufacturing ISM (55.5 vs. 54.9) and ADP employment survey (150k vs. 201k) will set the tone going into Friday’s employment report.

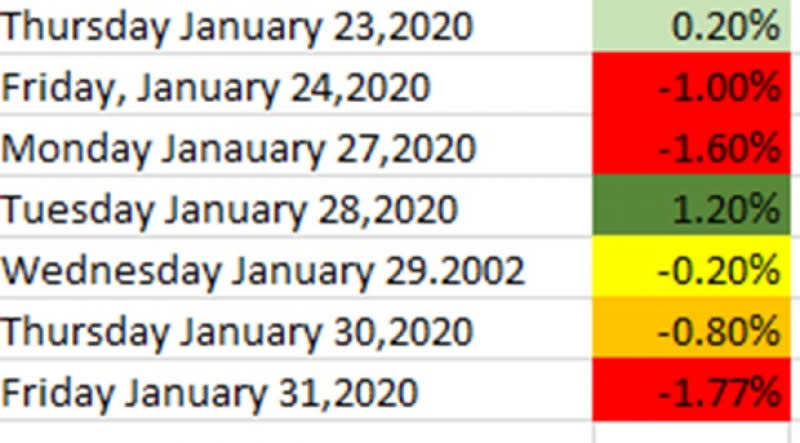

The anatomy of market sell-off through the lens of a trader

S&P 500 daily return, past 7 days, which is a very typical risk-off progression but nothing too crazy on the downside yet.

Friday 3:30 AM SGT (Yes real traders wake up at 3 AM when things look gnarly) Hmm WHO put there stamp of approval on China containment efforts. Traders quickly move to reduce over hedged USDCNH and Gold longs and buy back a chunk of those Oil shorts as WHO opposes restrictions on travel to China or trade with it. Everyone seems to agree, although they know things are going to get worse before better. It’s the herd mentality that also influences trading momentum when uncertainty is rampant.

Friday 9:20 AM SGT Social media goes frantic when close to 10,000 total confirmed cases of the virus were reported, which means its spreading at a faster pace than during SARS. (however, during SARS, the data was arguably underreported, partly as it coincided with the war in Iraq.) The market pared risk, but the WHO decree was too fresh in trader minds to trigger a more prominent sell-off.

Friday Asia Noon SGT: Now traders think its time to square the books and add some defensives hedges against a possible Monday market meltdown. Still, no significant market moves as big Asia traders are mostly hedged via proxy or in cash now looking for the transitory reversion play this week.

Friday London opens Asia is hedged but probably not over hedged, which begets a more prominent tail risk on Monday, none the less the London market continues to de-risk and gingerly buys more bonds underscoring the bid for gold. However, the big guns in London were somewhat complacent to the downside, which could contribute to a more significant Monday open tail risk.

Friday New York: Proprietary and discretionary traders get into the office early after following the proceedings in Asia the night before. And are now thinking that they need some defensive hedge as the markets are looking a bit ugly.

Friday New York Opening Bell: Splat!! Cross asset traders unanimously move in to buy more US bonds and to sell the Spooz. On the currency market, FX traders cover USD longs as rates markets are starting to price in a summer Fed rate cut and opt for the path of least resistance and buy USD vs. (SGD, THB, and CNH) to hedge weekend risk and probably add a bit of over hedge for a punt against the China Monday open

Friday New York 2:00 PM: Now traders think they are too short as the market has only sold off <2 %, so they now think it’s wise to cover some of that over hedged risk and the usual 2 PM to 4 PM EST short squeeze ensues.

Saturday: Everyone reads the Armageddon prophecies, the worst-case scenarios, and just how bad Fridays beat down was. But more importantly, the fear factor sets in due to a deluge of insane amounts of negative coverage.

A New Week Dawns

Monday Open: Market gap lower as expected selling initially builds, and then it would usually cascade into Europe and then New York. This is what typically happens but not sure how much of a force the “national team ” will be and how effective the PBoC massive liquidity injection remains the question mark. But its a lot of cash and could keep the market on an even keel.

Monday New York: Normally the lows would hit around 1- 4 PM EST, and then markets start to revert

Tuesday Asia: Yup another Turnaround Tuesday and the shorts get painfully squeezed

Wednesday: The teeter tooter battle of the bulls and the bears

Thursday: Unless there a slow down in the virus spread, traders get nervous again and put on the hedges they took off the day before.

Friday: Rinse and Repeat

Twitter Follow

Finally, after 8 years, I’m starting to get more active on Twitter, where I’m sharing interbank views from an assortment of Top tier global banks I’m in contact with , so follow me and I will be sure to follow you back.

Also, I will provide a weekly follow recommendation. This week it’s a heads up to Kevin Muir, who runs his own fund out of Toronto Canada . Also, in a former life and like me, he cut his trading chops on Bay Street Toronto Canada, where he was an equity derivates trader for Royal Banks of Canada. Kevin offeres up excellent market insights and great retweets.

This article was originally posted on FX Empire