Yahoo Finance

Yahoo Finance How Hispanic homeownership became a 'driving force' shaping the housing market's future

After three years of house hunting, Noemi Hoskins couldn’t bear the idea of taking her teenage daughters to see one more property.

“There was so much disappointment when I would end up not qualifying for the house that we loved,” she says. “Especially my youngest. She’d say, ‘We'll never get a house.'”

The thing that kept Hoskins, an immigrant from the Dominican Republic, in the game was the trust she had built with her real estate agent, who not only spoke her native Spanish but understood the challenges Hoskins faced in financing a home.

This year, Hoskins, 43, closed on a $425,000 single-family home in Methuen, a Boston suburb.

“It's awesome just to see my girls being at home and feeling at home,” she told USA TODAY.

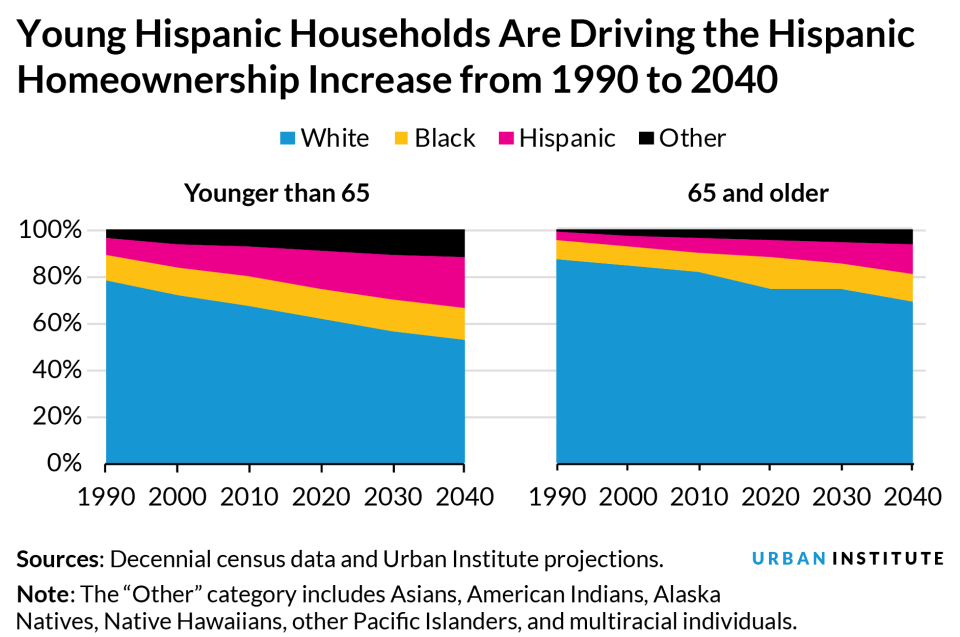

Hoskins is among a growing number of homeowners who, despite affordability challenges exacerbated by the pandemic housing market, are helping fuel the rise in Hispanic homeownership rates, the only demographic to see eight years of steady homeownership growth, according to census data.

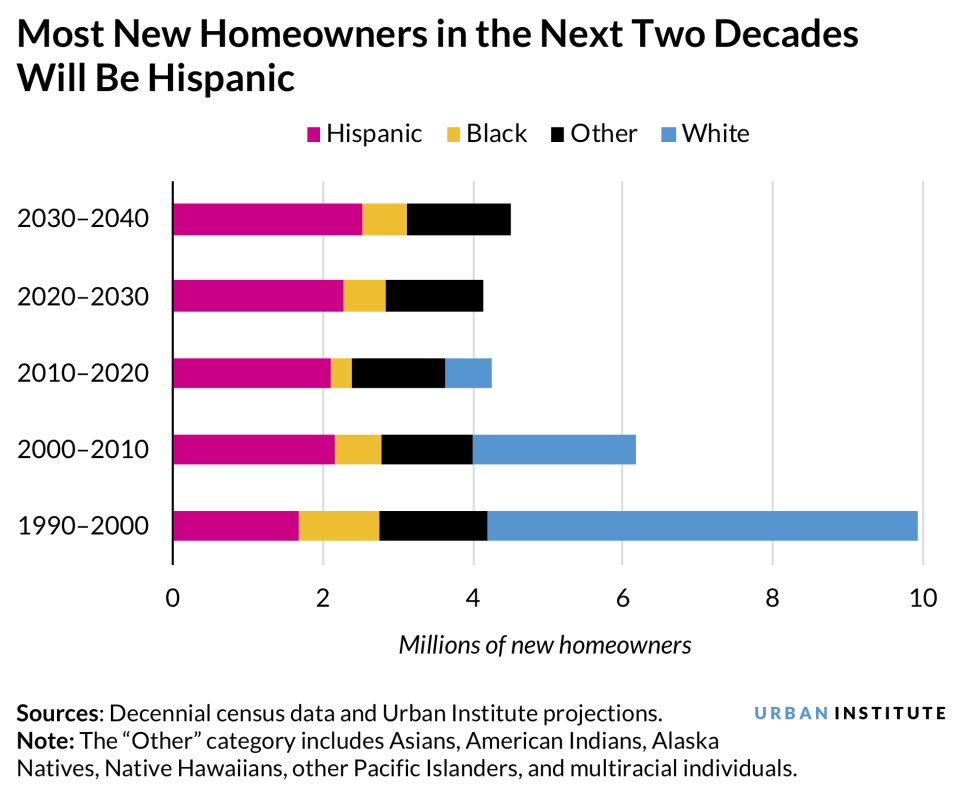

Between 2020 and 2040, 70% of net new homeowners will be Hispanic, according to the Urban Institute. That is because about one-third, or 17.9 million, of the nation’s Hispanic population is younger than 18 compared with 22% of the overall population and will be aging into the prime years for household formation in the coming years.

Credit scores: Exclusive: Fannie Mae to announce plan to bolster renters' credit scores

Housing: It's tough to buy a starter home these days. Three Americans tell their stories.

Mortgage rates: Housing market is 'overly sensitive' to Fed rate hikes. Experts weigh in on what's next.

That presents housing industry professionals with the unique opportunity to break down barriers and meet the needs of Hispanic homebuyers and help them build generational wealth, experts say.

“Hispanics are going be a huge driving force in terms of homeownership over the next couple of decades because the number of white homeowners is actually going to decline as the boomers die off,” says Laurie Goodman, founder of the Housing Finance Policy Center at the Urban Institute.

In 2022, homeownership rates stood at 74% for white Americans, 46% for Black Americans and 49% for Hispanic Americans, according to U.S. census data.

Between 2020 and 2040, there will be 6.9 million net new homeowners, a 9% increase, of which 4.8 million more will be Hispanic homeowners, 2.7 million more Asian and other homeowners and 1.2 million more Black homeowners, while white homeownership will dwindle by 1.8 million, the Urban Institute projects.

So it also makes business sense for the housing industry to pay attention to the needs and characteristics of this growing demographic, which tends to live with multiple generations and are more likely to be self-employed, experts say.

Latinos are 1.7 times more likely to start a business than any other racial group, according to a 2019 Bain & Company report.

Banks typically use W-2 tax forms – which shows the income a person has earned from their employer – as proof of income. With entrepreneurs, whose incomes tend to fluctuate, the underwriting standards tend to be stricter to avoid the risk of loan defaults and could lead to higher interest rates and requirements for higher down payments.

“So, it basically means that it would be good to change the way we do underwriting, for example, by counting more heavily the incomes of family members who contribute to the mortgage but who are not on the mortgage,” Goodman says.

Gary Acosta, co-founder and CEO of the National Association of Hispanic Real Estate Professionals, says the well-being of the housing industry may depend on it.

“My message to the big companies that service the housing industry is that the Latino market isn't for everybody. Just companies that want to stay in business in the next five years,” Acosta says with a laugh.

'Focus' and 'save money'

When Fredy Barerra came to the U.S. from El Salvador in 2008, he says, he was laser-focused on saving money. He rented a small apartment with several of his friends in Houston, trying to keep is living expenses to a bare minimum. When he was married a few years later, he moved in with his mother-in-law for four years to save up.

“I always had a dream of buying a house,” says Barerra, a manager at Smart Meal, a meal prep company. “I saw people renting for 10 years, but after 10 years they had nothing.”

In 2016, he bought his first home for $120,000 with an FHA loan that allowed him to put a 3.5% down payment, smaller than what most conventional loans would have required. Last year, he sold it for $220,000, netting a tidy profit as the pandemic housing market soared in Texas.

Barerra then bought his second home, a more spacious single-family home with a two-car garage for $285,000 in Tomball, a Houston suburb. This time, he had $80,000 for a down payment and qualified for a conventional loan.

“People who come from my country ask me ‘How did you do it?,’” he says. “I say, ‘You need only focus and you need to save money’.”

Having a Hispanic real estate agent and a mortgage broker who speak Spanish made the process that much simpler, says Barerra, who is not fluent in English.

Largest Hispanic-owned, private mortgage company

That’s something Patty Arvielo, a daughter of a Mexican immigrant and CEO and co-founder of New American Funding, the largest privately owned and Latina-owned mortgage company in the nation, understands well.

“In 1964, my dad went to go rent an apartment by himself, and then when he showed up with my mother, the landlord told him: ‘We don't rent to Mexicans. You didn't tell us your wife was Mexican’,” she says.

For many immigrants from Latin American countries, home ownership is often unattainable in their native countries, where financing a home purchase is often very difficult, she says.

“So whether you're from Guatemala, El Salvador, Mexico, Columbia, we all come here knowing that the dream of home ownership is very accessible,” she says.

In 2022, almost 70% of the Latino home purchase originations were through an independent mortgage lender, according to data from the Home Mortgage Disclosure Act – a fact that underscores the importance of understanding the nuances of their needs and limitations.

At New American Funding, 33% of all purchase loans in 2021 went to minority borrowers, compared with 28% for all other lenders combined. Purchase loans to Black borrowers in 2021 was 60% higher than the industry average, while purchase loans to Hispanic borrowers was 30% higher than the industry average.

The reason the company has been successful in minority lending is because it has a large minority (42%) workforce, she says.

Arvielo, who has more than 40 years of experience in the mortgage business, founded California-based New American Funding with her husband, Rick, 20 years ago.

The company is now one of the top 20 mortgage companies in the U.S., with more than 3,400 employees and a servicing portfolio of more than 243,700 loans for $64.3 billion.

Getting educated about homeownership

Francisco Davila, a first-generation Hispanic American, who works as an HR manager for the City of Long Beach, says he never would have considered buying a home if it had not been for a friend who started working at New American Funding.

Davila, 38, became a first-time homebuyer in September 2020 when he purchased a condominium within walking distance of his office.

“I had been renting for 10 years, and when my roommate moved out, I was thrown into the situation,” he says. “My friend was like, why don't we run your numbers and just see whether you're eligible?'"

Davila, who had been promoted recently, says he was surprised to find out he was eligible for some affordable places.

“I didn't think I was going to find anything at that range here in the city, because growing up, I always lived in a single-family home with a backyard, and that's what my expectations were,” he says. “In Long Beach, there was no way I could afford that. I hadn't even considered the idea of owning a condo.”

After six months of looking, Davila found a one-bedroom condo listed for $269,000. He offered $275,000 in a competitive market and went with a conventional mortgage.

He says financing was not a problem, because he had a good credit score and had paid down his debts.

"I had been living with a poverty mentality. I didn’t spend on designer clothes. I saved as much as I could,” he says.

His friend also sent him to a first-time homebuyers seminar so he could familiarize himself with all the steps.

Looking back, Davila says, he’s glad he took the plunge to go from a $1,400 rental to becoming a condo owner.

“The property values have shot up, and I've been looking around and the rents are crazy for downtown Long Beach right now," he says. "There's a new building that just went up for one bedroom. They're going for $4,000 a month for rent.”

When Hoskins, the recent homebuyer from suburban Boston, moved to the U.S. on a work visa to work as a hotel room attendant in 2005, homeownership was not even a distant dream.

But watching her sister build a life for herself and become a homeowner motivated her, she says.

“I had to get my finances in order, get educated about becoming a homeowner and understand the local market,” she says.

Getting promoted last year to deputy director of housekeeping helped, she says.

When she first started looking for homes, her daughters were attending public schools in North Andover, a “rich town” where most of their classmates lived in big homes.

She always wished she could do better for them.

"I felt like I could be doing so much better for them than living in an apartment, but that is all I could afford at that moment."

Hoskins kept her home purchase from her daughters until the last minute for fear it could fall through.

"They cried because the whole process was a surprise," she says. "I never said anything to them until the closing."

Policymakers and homebuilders should pay attention to the needs of the population that will be drive future demand, says Janneke Ratcliffe, who leads the Housing Finance Policy Center at the Urban Institute.

The Latino median household income has grown by 50% to $60,566 over the past 10 years, outpacing the overall income growth of 36% during that same period. But the median household income among white households is $75,412, 24.5% more than Latino households.

“They're going to need starter homes and there is a lack of supply of affordable housing," she says. "If there's no stock for them to buy, that is going to really stifle the future of home ownership."

Swapna Venugopal Ramaswamy is a housing and economy correspondent for USA TODAY. You can follow her on Twitter @SwapnaVenugopal and sign up for our Daily Money newsletter here.

This article originally appeared on USA TODAY: By 2040, 70% of net new homeowners will be Hispanic. What that means.