Yahoo Finance

Yahoo Finance HEXO (TSE:HEXO) May Not Be Profitable But It Seems To Be Managing Its Debt Just Fine, Anyway

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies HEXO Corp. (TSE:HEXO) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for HEXO

What Is HEXO's Debt?

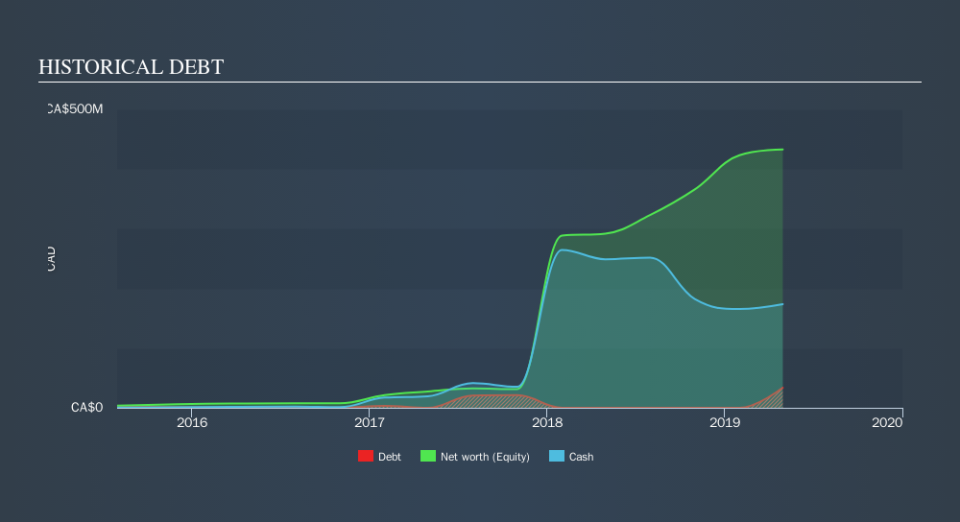

The image below, which you can click on for greater detail, shows that at April 2019 HEXO had debt of CA$33.7m, up from none in one year. However, its balance sheet shows it holds CA$173.6m in cash, so it actually has CA$139.9m net cash.

How Healthy Is HEXO's Balance Sheet?

The latest balance sheet data shows that HEXO had liabilities of CA$47.4m due within a year, and liabilities of CA$30.4m falling due after that. Offsetting these obligations, it had cash of CA$173.6m as well as receivables valued at CA$18.1m due within 12 months. So it actually has CA$114.0m more liquid assets than total liabilities.

This short term liquidity is a sign that HEXO could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, HEXO boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine HEXO's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, HEXO reported revenue of CA$34m, which is a gain of 665%, although it did not report any earnings before interest and tax. That's virtually the hole-in-one of revenue growth!

So How Risky Is HEXO?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that HEXO had negative earnings before interest and tax (EBIT), over the last year. And over the same period it saw negative free cash outflow of CA$182m and booked a CA$35m accounting loss. With only CA$139.9m on the balance sheet, it would appear that its going to need to raise capital again soon. Importantly, HEXO's revenue growth is hot to trot. High growth pre-profit companies may well be risky, but they can also offer great rewards. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting HEXO insider transactions.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.