Yahoo Finance

Yahoo Finance Here's Why We're Not Too Worried About Cypress Development's (CVE:CYP) Cash Burn Situation

There's no doubt that money can be made by owning shares of unprofitable businesses. Indeed, Cypress Development (CVE:CYP) stock is up 640% in the last year, providing strong gains for shareholders. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

In light of its strong share price run, we think now is a good time to investigate how risky Cypress Development's cash burn is. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business' cash, relative to its cash burn.

See our latest analysis for Cypress Development

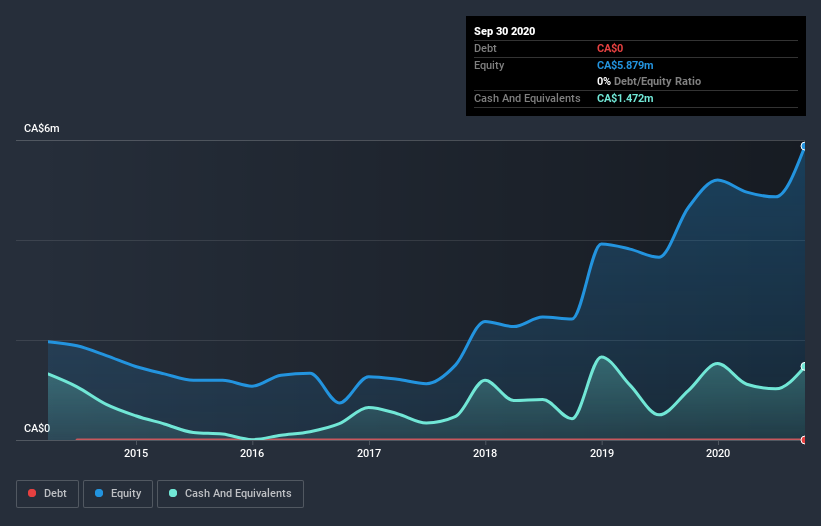

How Long Is Cypress Development's Cash Runway?

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. As at September 2020, Cypress Development had cash of CA$1.5m and no debt. In the last year, its cash burn was CA$1.7m. So it had a cash runway of approximately 10 months from September 2020. That's quite a short cash runway, indicating the company must either reduce its annual cash burn or replenish its cash. Depicted below, you can see how its cash holdings have changed over time.

How Is Cypress Development's Cash Burn Changing Over Time?

Because Cypress Development isn't currently generating revenue, we consider it an early-stage business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. Given the length of the cash runway, we'd interpret the 43% reduction in cash burn, in twelve months, as prudent if not necessary for capital preservation. Admittedly, we're a bit cautious of Cypress Development due to its lack of significant operating revenues. We prefer most of the stocks on this list of stocks that analysts expect to grow.

Can Cypress Development Raise More Cash Easily?

While Cypress Development is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of CA$152m, Cypress Development's CA$1.7m in cash burn equates to about 1.1% of its market value. So it could almost certainly just borrow a little to fund another year's growth, or else easily raise the cash by issuing a few shares.

So, Should We Worry About Cypress Development's Cash Burn?

Even though its cash runway makes us a little nervous, we are compelled to mention that we thought Cypress Development's cash burn relative to its market cap was relatively promising. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Cypress Development's situation. On another note, Cypress Development has 4 warning signs (and 2 which can't be ignored) we think you should know about.

Of course Cypress Development may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.