Yahoo Finance

Yahoo Finance Here's Why Sandstorm Gold (TSE:SSL) Can Manage Its Debt Responsibly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Sandstorm Gold Ltd. (TSE:SSL) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Sandstorm Gold

What Is Sandstorm Gold's Debt?

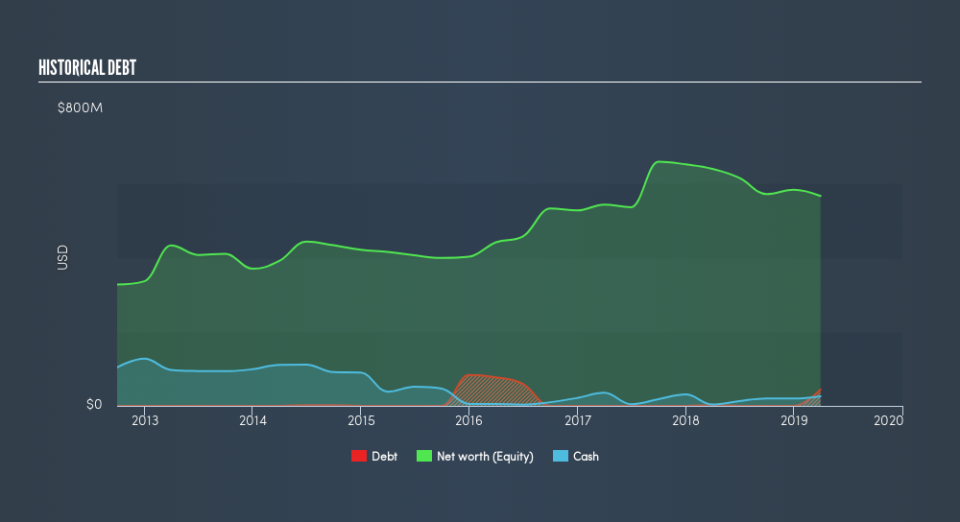

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Sandstorm Gold had US$44.0m of debt, an increase on US$2.00m, over one year. However, because it has a cash reserve of US$26.0m, its net debt is less, at about US$18.0m.

A Look At Sandstorm Gold's Liabilities

According to the last reported balance sheet, Sandstorm Gold had liabilities of US$6.42m due within 12 months, and liabilities of US$47.3m due beyond 12 months. Offsetting these obligations, it had cash of US$26.0m as well as receivables valued at US$5.26m due within 12 months. So it has liabilities totalling US$22.5m more than its cash and near-term receivables, combined.

Of course, Sandstorm Gold has a market capitalization of US$1.10b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Sandstorm Gold has net debt of just 0.39 times EBITDA, indicating that it is certainly not a reckless borrower. And this view is supported by the solid interest coverage, with EBIT coming in at 9.4 times the interest expense over the last year. It was also good to see that despite losing money on the EBIT line last year, Sandstorm Gold turned things around in the last 12 months, delivering and EBIT of US$16m. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Sandstorm Gold's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, Sandstorm Gold generated free cash flow amounting to a very robust 94% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that Sandstorm Gold's demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its interest cover also supports that impression! Looking at the bigger picture, we think Sandstorm Gold's use of debt seems quite reasonable and we're not concerned about it. After all, sensible leverage can boost returns on equity. We'd be motivated to research the stock further if we found out that Sandstorm Gold insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.